Earnings Roundup | Nebius, Tower Semi

Two Massive Beats

I am a shareholder in neither, but congrats to those who were. You made a good decision and probably had a good morning.

Anyways, both of them had massive beats and are looking great. Let’s review the earnings for both today, as we can learn a lot from them in terms of both individual company performance, but more importantly, read throughs to their broader ecosystems (neoclouds for Nebius and optics for Tower).

By accessing this content, you acknowledge and agree to our terms and conditions. This research is not financial advice.

Headlines

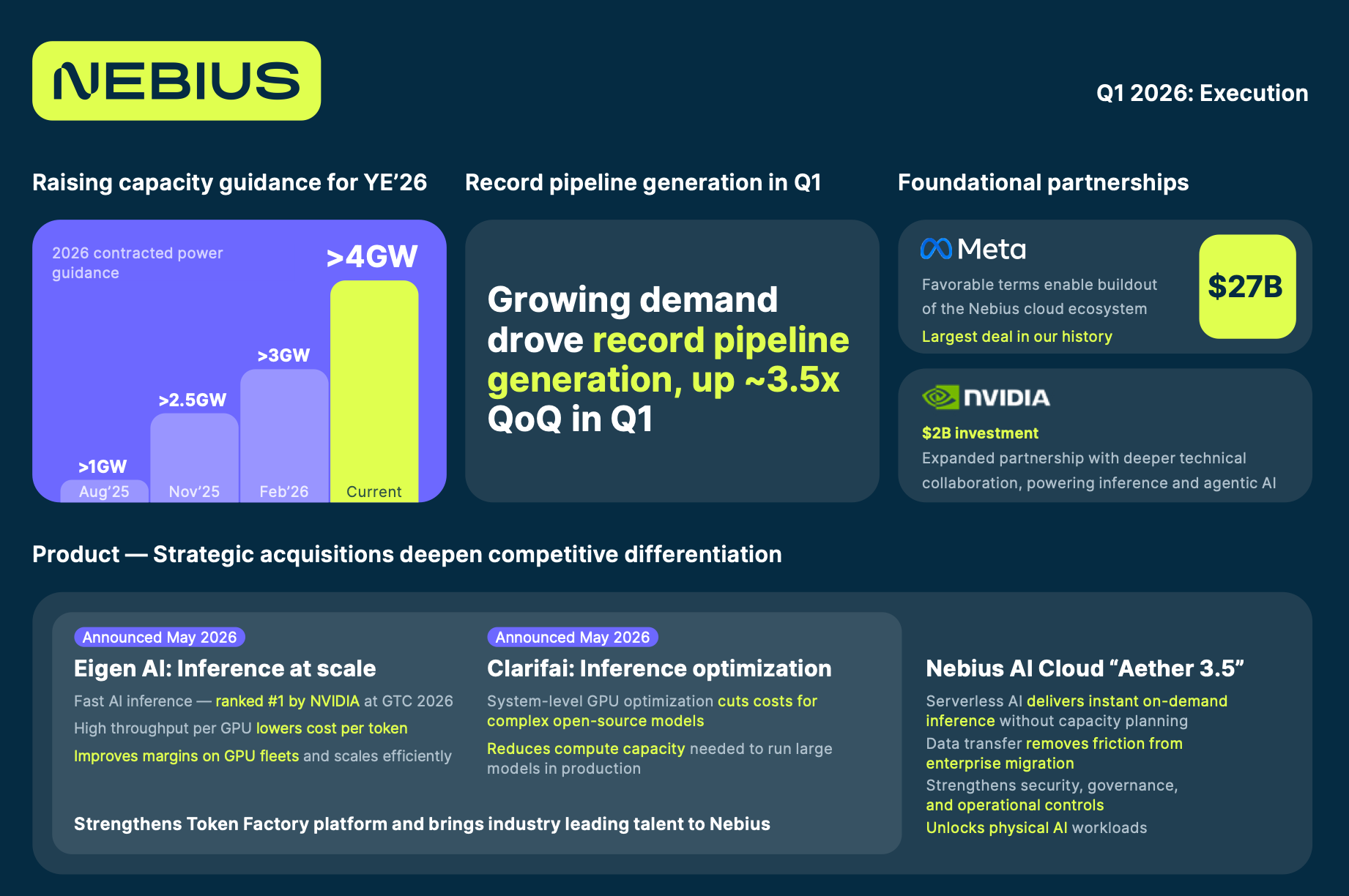

Nebius

Nebius is the smaller (only revenue wise as their market cap flipped CRWV) sibling of CoreWeave and the favorite child of investors.

They are better at serving the long-tail of AI demand instead of only signing big deals and are executing MUCH better on several fronts (and thus have the Super Ultra Premium Valuation). I am biased towards CoreWeave due to my positioning so this is objective. Very rarely do I make a call that contradicts share price momentum.

First, they reiterated their $8b and $3.2b guidance for YE26 ARR and revenue respectively (compared to CoreWeave’s $18.5b and $12.5b). They guided their EBITDA margins to 40% for 2026 (vs 60% for CoreWeave due to scale). They are sold out for 2026 capacity as well.

Now on to how they’re executing really well.

Nebius significantly raised their contracted power guideline to 4 GW. This is an entire gigawatt more than what they gave for their Q4 earnings release. Despite having a smaller (less than 50%) base than CoreWeave today they’ve contracted more power. As a read through of Neoclouds in general, it shows that contracting power is really never the issue anymore, as both public Neoclouds surprised to the upside on their contracted power. Nebius also tends to self-build a lot more, and they have a big 1.2 GW site coming online in Pennsylvania.

Next is their increase in capex from a midpoint of $18 billion to a midpoint of $22.5 billion. Unlike for CoreWeave, this is due to higher projected 2027 revenue rather than cost increases, though they did cite around 3-5% of cost pressure for 2026 from component pricing (memory lol).

For financing, they raised $4b from converts and $2b from equity in the quarter, and are now tapping into debt as they can sign asset-backed loans with their much larger contracts, like the new $27 billion deal with Meta.

Tower Semi

Tower had a pretty sizeable beat on the Q2 guide.

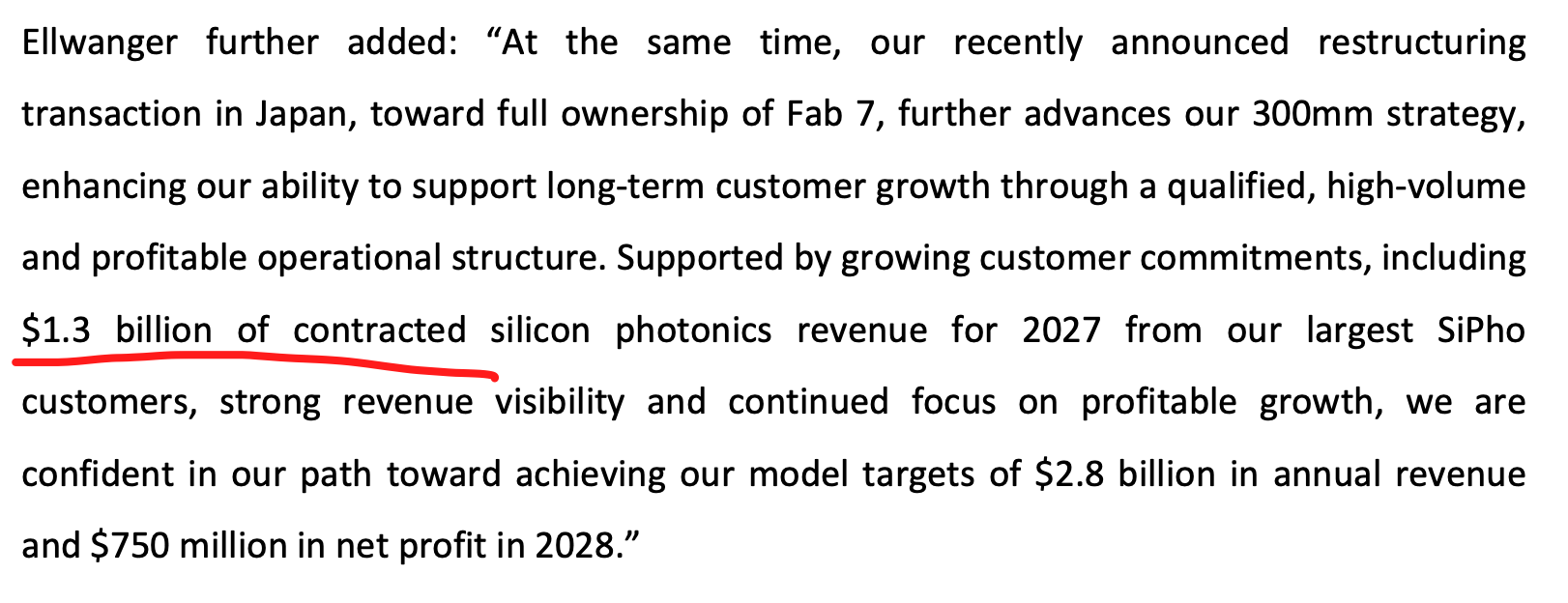

But the real story is that they signed $1.3 billion of Sipho revenue for 2027. This is a massive revision upwards from sell-side and SemiAnalysis projections. It is actually quite close to my own projections from my original long thesis ($1.44b) before I got peer pressured to revise it down lmao.

On the call, they said that they are backed by even more contractual revenue in 2028. Pretty crazy stuff.

They are continuing on their goal to 5x Q4 2025 shipments by year-end 2026 and are on track to execute their $920 million investment plan. Today, their fabs are running mostly clustered around 60 to 80% utilization, which means that they’ll most likely hit capacity limits soon and join Lumentum in the sold-out club.

Call Takeaways & Read-Through

Now on to the meat of our analysis, which is on their Q&A and the read-throughs that we can glean for the rest of their peers.

For Nebius, I talk about the effects of stronger GPU pricing, timing of their capacity additions at their Pennsylvania campus, and the structure of their Meta contract.

We read this through to CoreWeave and Neoclouds in general for what this means for future contract structures (with my own speculation) and whether or not there is a real cap on capacity. I share how this changes my view of and positioning on CoreWeave.

For Tower Semi, we discuss their interesting comments on their content in CPO versus plugables and a little bit of reading of management’s tone, clarify the $1.3 billion commitment with more granular details, unpack their market share comments, discuss pricing power, and talk about their positioning against TSMC COUPE.

We then read this through to the rest of the optics ecosystem and give one lesson I learned that we can take away and apply to how we view our favorite names.