Tower-ing Over the Competition

Tower Semi thesis

Opinions are my own and do not represent past, present, and/or future employers. All content is based on public information and independent research. This newsletter is not financial advice, and readers should always do their own research before investing in any security. I am invested in the semiconductor industry. As of the date of this publication, I hold a long position in TSEM.

Earlier this week, I made my “career defining bet” on Soitec.

Soros was right about going for the jugular. I sold 3 positions at significantly depressed prices during the Iran crash to fund this. Everything I’ve been taught, as well as my emotions, went against it, but I decided that opportunities like this come rarely.

I am holding this for the LT. Haven’t sold a single share. Parts 2-7 will come after the optics primer because they need to build on top of it. In my part 1, I also forgot to add price/book, which is actually the most compelling valuation metric. Even after the run-up, they are at 1.4x. Those fabs are gonna become real valuable soon.

Citrini and Serenity (on X) both pitched this name shortly after my article’s release. Irrational Analysis also validated the thesis.

Special thanks to Archetype Capital for sharing my research. Check out his publication, he made a very similar bet-the-farm type call on a Japanese company called JCU which has performed very well.

Very happy to be part of this really nice community. Thank you.

There seems to be a lot of interest around Tower recently on X and just general chatter. The GOATs of Substack + FinTwit all put in a good word for this company. So I thought it would be timely for me to do a short piece on them.

I am a Tower OG. My entry price was $67. Been out of the position for quite a while but now I’m back in.

Tower’s thesis is quite simple. A lot of people see them as a CPO play, but in my opinion that is not fully correct. The main thesis is the massive amounts of share SiPho will gain in the 1.6T and beyond transceivers for short reach scale-out. The call option is defending significant share in CPO against TSMC COUPE’s onslaught. But the “why enter now?” is probably the best part.

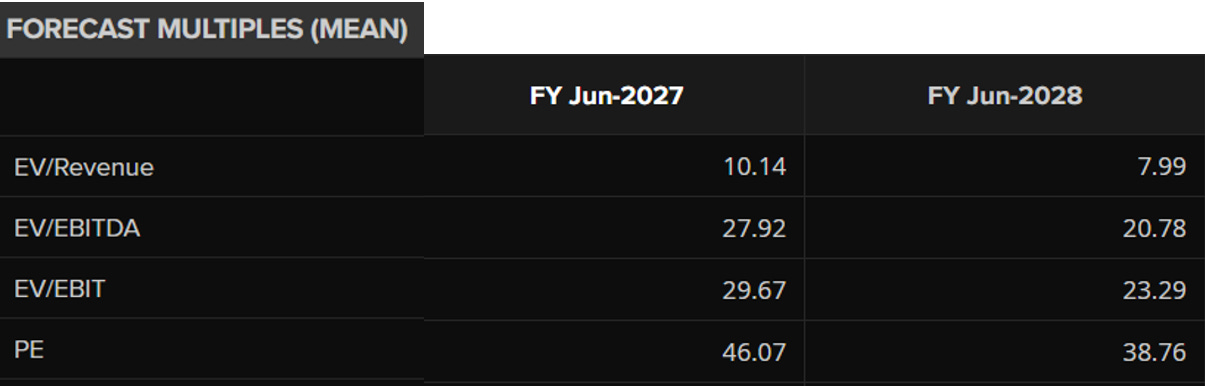

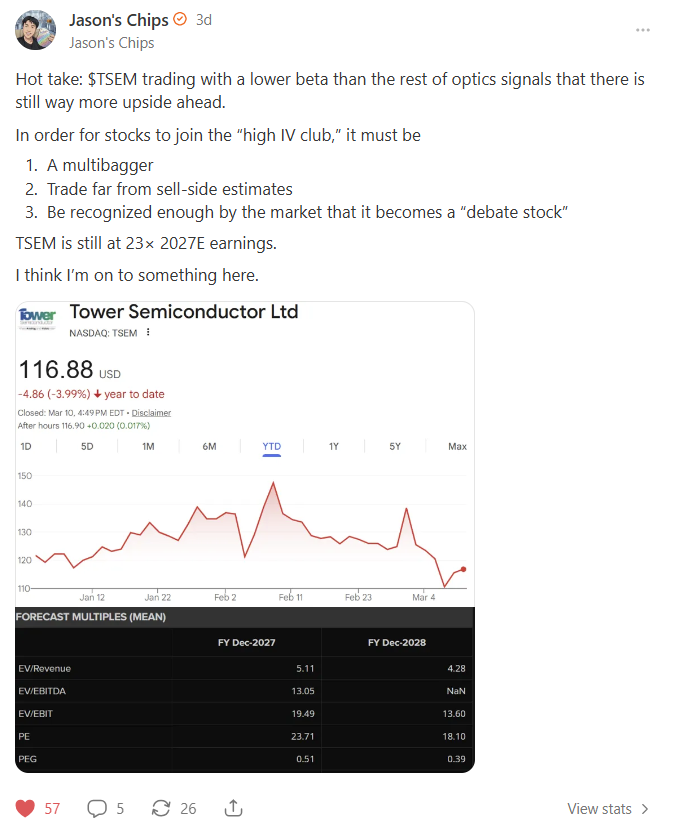

Photonics has been on a tear. And trades significantly above sell-side estimates.

Lumentum as an example (you guys know I love LITE but they are the poster child of this):

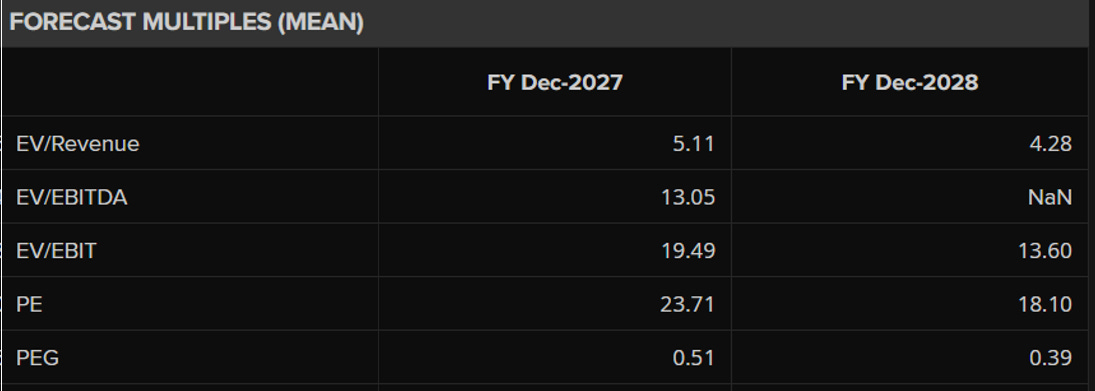

But not TSEM.

At literally ½ of LITE’s sell side multiples.

They are either relatively undiscovered, mis-read by the algos due to legacy mix, or simply misunderstood. They have low IV/beta, and usually names become volatile once they have significantly re-rated and became a “battleground stock.” LITE/AAOI/COHR have done that. TSEM has not done that.

I called this out in a note a few days ago.

Since then they’ve generally outperformed the rest of photonics in a tough macro environment.

Outline

Aura Farming via Capacity Economics

SiPho Transceiver Market Share Conquest

Escaping the COUPE

Full Five-Page Financial Model

Aura Farming via Capacity Economics

Finance people are obsessed with ROIC. Well I have good news, Tower execs would like to have a word with you.

“If we look at what we’re doing with SiPho as far as CapEx, the really nice thing with the SiPho and the CapEx is that it’s truly from the time that you start shipping wafers, you’re dealing with a half year ROI on the CapEx that you put into the tools.”

- Russell Ellwanger, Tower Semi Q3 2025 earnings call

This is so incredibly underrated and under-discussed. Let’s think about what this means.

It takes SIX MONTHS of wafer sales to match the capex of the capacity. Assuming that refers to revenue, and SiPho contribution margins are 50% (they’re actually higher), the ROIC of the capacity is over 100%.

Tower Semiconductor aura farms via capacity economics.

On capex:

“Now moving into our CapEx investment plan and its impact on our financial model. As we announced today, in order to support the increasing SiPho and SiGe demand, we are allocating an additional $270 million of cash to invest in capacity and capability side for equipment, which would result in a total of $920 million cash investments in CapEx, including the $650 million we already announced during 2025.”

On capacity:

“...it’s the actual capacity that we’re building. So if you look at what we had referred to as the $380 million run rate that we had in Q4, take off of that some small amount of NRE, which we don’t specify, the silicon wafers that we shipped for the fourth quarter, that exact amount of silicon wafers by capacity, we plan to have 5x more of that in the fourth quarter of 2026.”

One billion dollars to 5x capacity at 100% ROIC?

Please. Raise debt. Raise equity. Light cash on fire. I’m begging you. Do more capex.

SiPho Transceiver Market Share Conquest

The optical networking market is complicated. Links can range from centimeters to kilometers. There’s the scale-up, scale-out, and scale-across reach tiers, but there are also sub-tiers within each. Each has a different optimal architecture. I have a very long primer on this coming up soon.

But the short reach scale-out transceiver market is what is most exciting for Tower.

This is the <2km cable length market. Middle of the road. It connects mostly leaf/spine and spine/leaf links inside a data center rack-to-rack, row-to-row, pod-to-pod, and hall-to-hall. Sometimes building-to-building on the same campus. It is the optical network that stitches the AI cluster together after you leave the server/rack internals but before you get to the true metro/DCI.

This is the biggest market in optics, by far. It is the meat of pluggable volume.

I will abstract away the modulator and modulation scheme for now. The most relevant architectural tradeoff for the Tower thesis is the material battle: Silicon Photonics (SiPho) vs monolithic Indium Phosphide (InP).

Silicon is the material used for every chip in the world because it’s cheap and easy to work with. However, it can’t make light.

InP is the material that makes light but is very expensive, brittle, and has lots of defects when you try to print chips on it.

Silicon photonics is the process of putting the modulator (thing that encodes data into light) and waveguides (little paths for the light to travel through) on a silicon chip. The laser light source must still be InP.

Pro: Cheap and mass produceable.

Con: Alignment hell. You need to align the laser with the entrance of the waveguide in the SiPho chip. Then, you need to align the exit of the waveguide with the fiber cable.

Monolithic InP means putting the supporting functions like the modulator on the same InP chip as the laser.

Pro: Everything is on one chip so there is no need for alignment. A very elegant solution.

Con: Big InP chip is very expensive and yields mathematically get worse as chip size increases.

The alpha here isn’t that one solution is strictly better than the other. Instead, we must observe which engineering tradeoff becomes more attractive over time as data speeds increase.

When we migrate from 800G to 1.6T, one of the tradeoffs change while the other is unaffected. The optical structures you must print on InP become bigger, more complex, and more active, while the assembly complexity for SiPho remains the same.

Therefore, as lane speeds rise, the cost of burning scarce InP wafer area on large integrated devices grows faster than the cost of solving difficult alignment in module assembly, causing SiPho becomes more economical and take market share.

If you dig into some earnings calls you can observe the early stages of this share capture become accepted.

“Our capacity growth is fully aligned with and spoken to by our customer demand outlook. Silicon photonics continues to increase market share over EML solutions given its significant cost advantage.

… As such, we anticipate this market share shift to be permanent.”

- Russell Ellwanger, Tower Semi Q3 2025 earnings call

“That being said, I still think, you know, consistent with what we’ve said over the past, would expect silicon photonics to be the majority of the transceiver shipments at the 1.6T node. We think the numbers are so large, you know, based on what we’re seeing in terms of the demand from our customers, that our EML shipments, even in the face of a mix shift toward silicon photonics, the absolute number of EMLs will go up for us and rather appreciably.”

- Michael Hurlston, Lumentum Q2 2026 earnings call

Escaping the COUPE

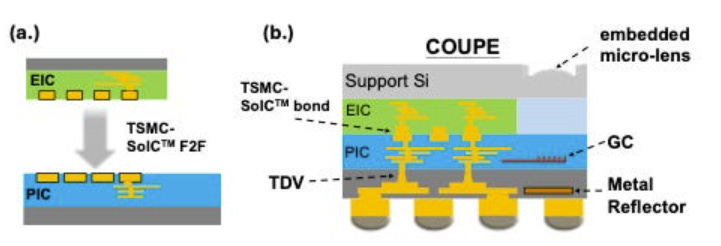

TSMC COUPE is brilliant technology. They bond the electrical IC (EIC) to the photonic IC (PIC) using hybrid bonding. It is very hard to do.

Perhaps more importantly, it is absolutely necessary for CPO. When you think CPO optical engine, think hybrid bonding and think COUPE.

This leads us to an interesting 4d chess move by TSMC. TSMC actually has bad photonics nodes. SiPho does not care about TSMC’s decades of yield learning on leading edge EUV as it is a completely different ball game. The specialists Tower and GloFo beat the generalist TSMC. Tower is the best out of the three.

However, TSMC knows this and they aren’t going down without a fight. So they gave their customers an ultimatum.

If you want to use our legendary COUPE packaging, you must fabricate your chip at TSMC.

So customers lose the choice of fabbing the PIC at Tower. Given TSMC has the best packaging AND the best EIC (where they actually shine!), the battle heavily favors goliath over david.

The risk to Tower is that they won’t capture any market share in CPO.

However, I think the story is more nuanced. There are specific pockets of the CPO markets Tower can still address.

The first is hyperscaler in-house custom optical silicon. Google, Amazon, and Meta all have internal photonics teams designing custom PICs for their own infrastructure. These customers explicitly want foundry independence — they don’t want to be locked into TSMC’s integrated stack for strategic and supply chain reasons. They have the engineering resources to handle packaging outside TSMC’s ecosystem. Tower’s open platform, superior PIC process, and priority capacity access make them the natural foundry partner.

The second is Broadcom’s open CPO ecosystem. Broadcom’s explicit strategy is a merchant CPO platform where third-party optical engines integrate with their switch ASICs via standardized interfaces. They deliberately don’t vertically integrate the PIC, which means every company building optical engines for Broadcom’s platform needs a SiPho foundry. Tower is the natural anchor foundry for this ecosystem given the Cadence co-simulation flow, the PDK depth, and the fact that Broadcom itself has used non-TSMC supply chains for optical components historically.

The third is CPO startups and emerging optical engine companies outside the Nvidia/Broadcom duopoly. Companies like Ranovus, Nubis, Celestial AI, and others building differentiated CPO architectures need a foundry that offers process flexibility, MPW services for early development, and a rich PDK ecosystem for fast iteration. TSMC’s platform is designed around specific customer architectures and is not accessible to smaller players the same way Tower’s open foundry model is.

The conclusion is that CPO is not a headwind for Tower like it is for Innolight/COHR/AAOI, nor is it a tailwind like it is for LITE. They just get a smaller piece of a much bigger pie. And timing wise, it’s not relevant to the thesis since it’s so far out yet very undecided.

Full Five-Page Financial Model

Because we can’t “infinite TAM” or “decades-long growth runway” Tower like we may do for some other optical names, the financials become more important than ever. Below the paywall, I share my revenue build (with capacity, utilization, ASP, and capex for each segment), three-statement model, and DCF.

It’s a big model :)