CPO Supply Chain 101

InP Substrate, Epitaxy, Laser, Optical Engine. AXTI, LITE, AIXA, COHR, SOI, TSEM

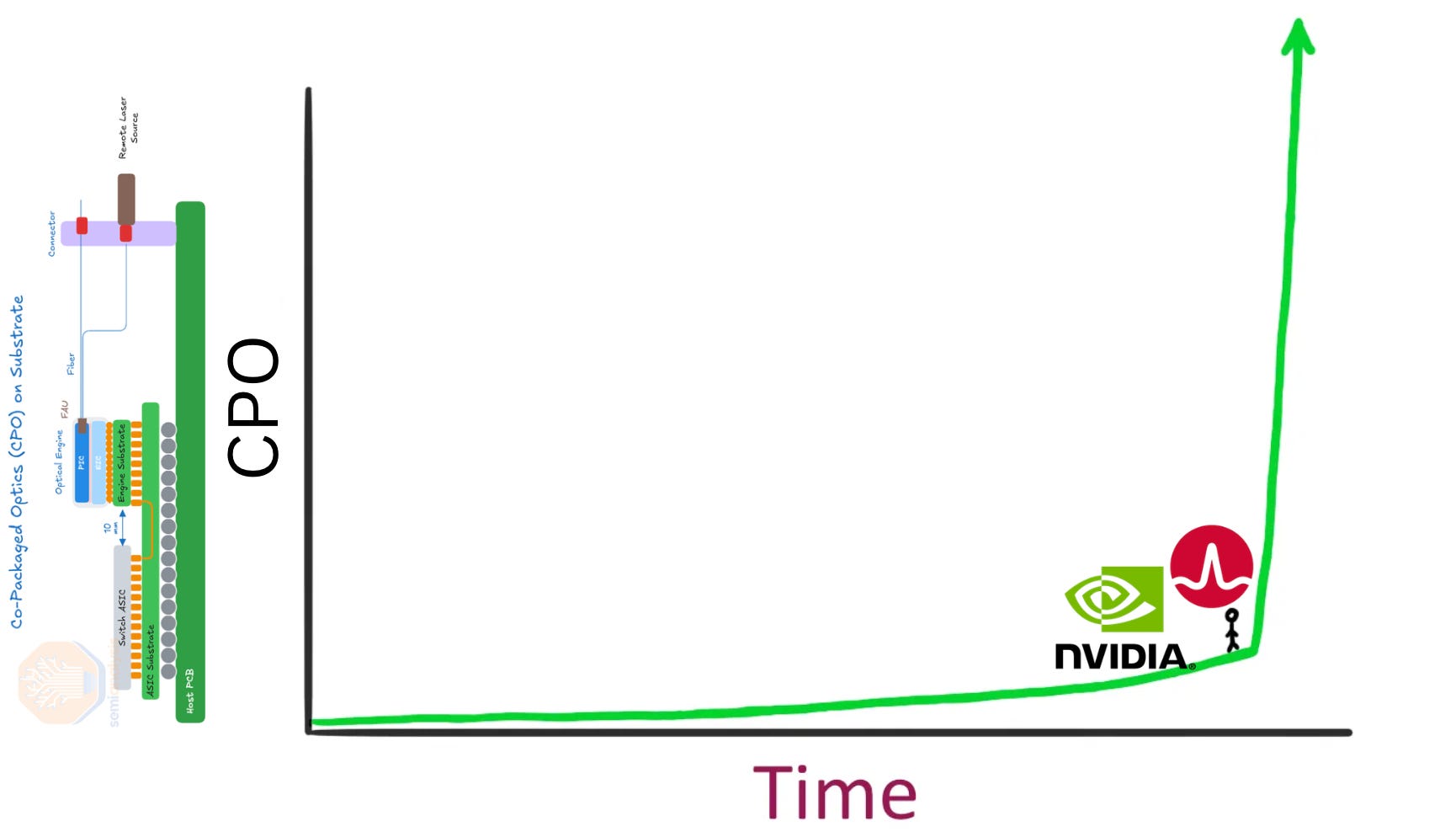

The most important concept to understand when analyzing the CPO supply chain is the power of e x p o n e n t i a l.

Please don’t tell us that we’re going to overbuild because we double the capacity of optical widgets.

There are two layers to this exponential.

First, I think networking will grow as a share of the BOM over compute over the long run. You can see this specific value-add transition in NVIDIA’s earnings, as they missed on compute but massively beat in networking.

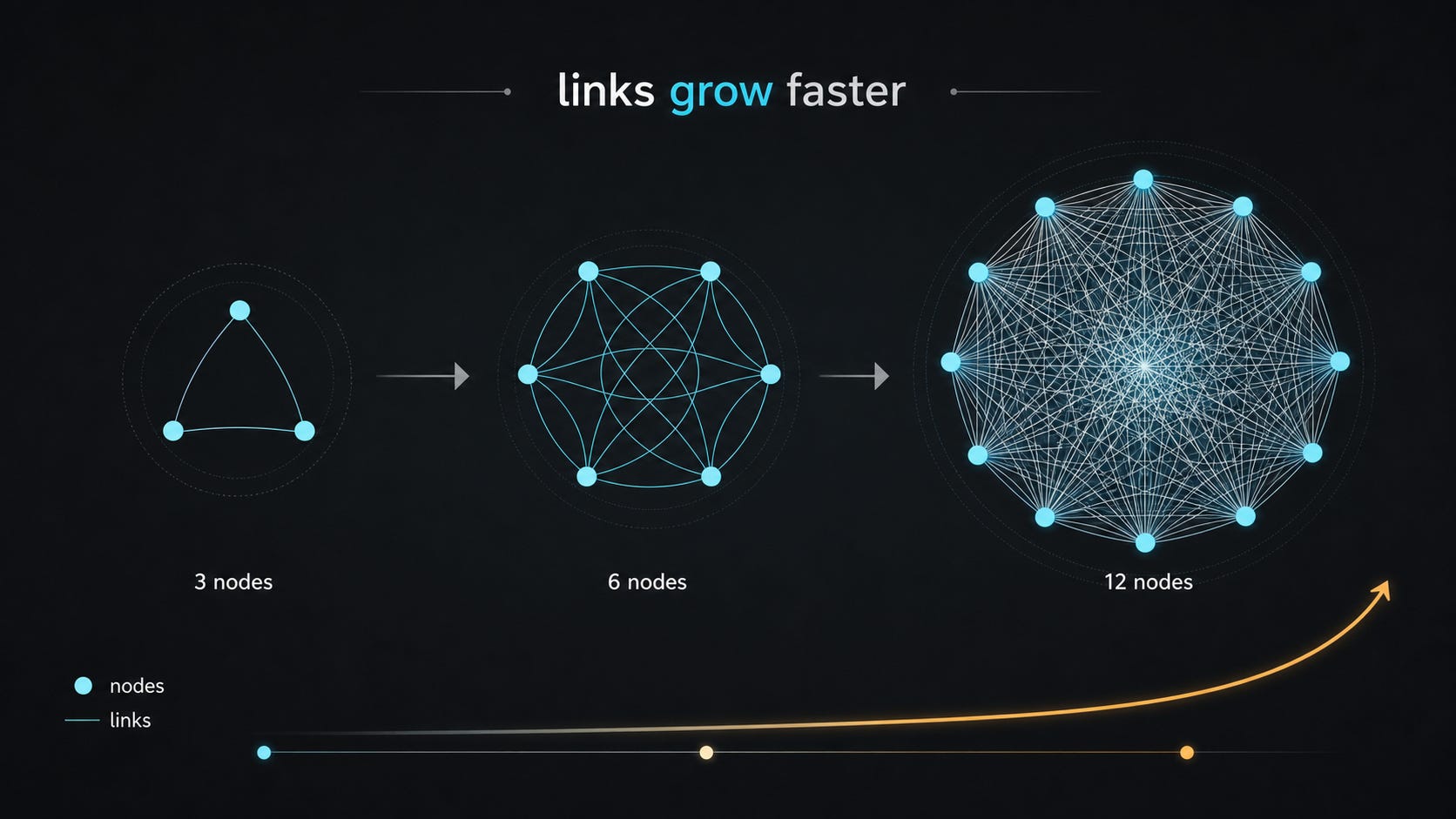

It’s a pretty simple concept, and I’m unsure why this isn’t talked about more in general. If we are hitting the limits of Moore’s Law and traditional dies can only be so big (sorry Cerebras), the only way that we get more powerful compute units is by linking them together. This means that the networking BOM is about proportional links:chips (inside a rack) or links:rack (inside a DC). And according to graph theory, the number of edges will always grow faster than the number of nodes.

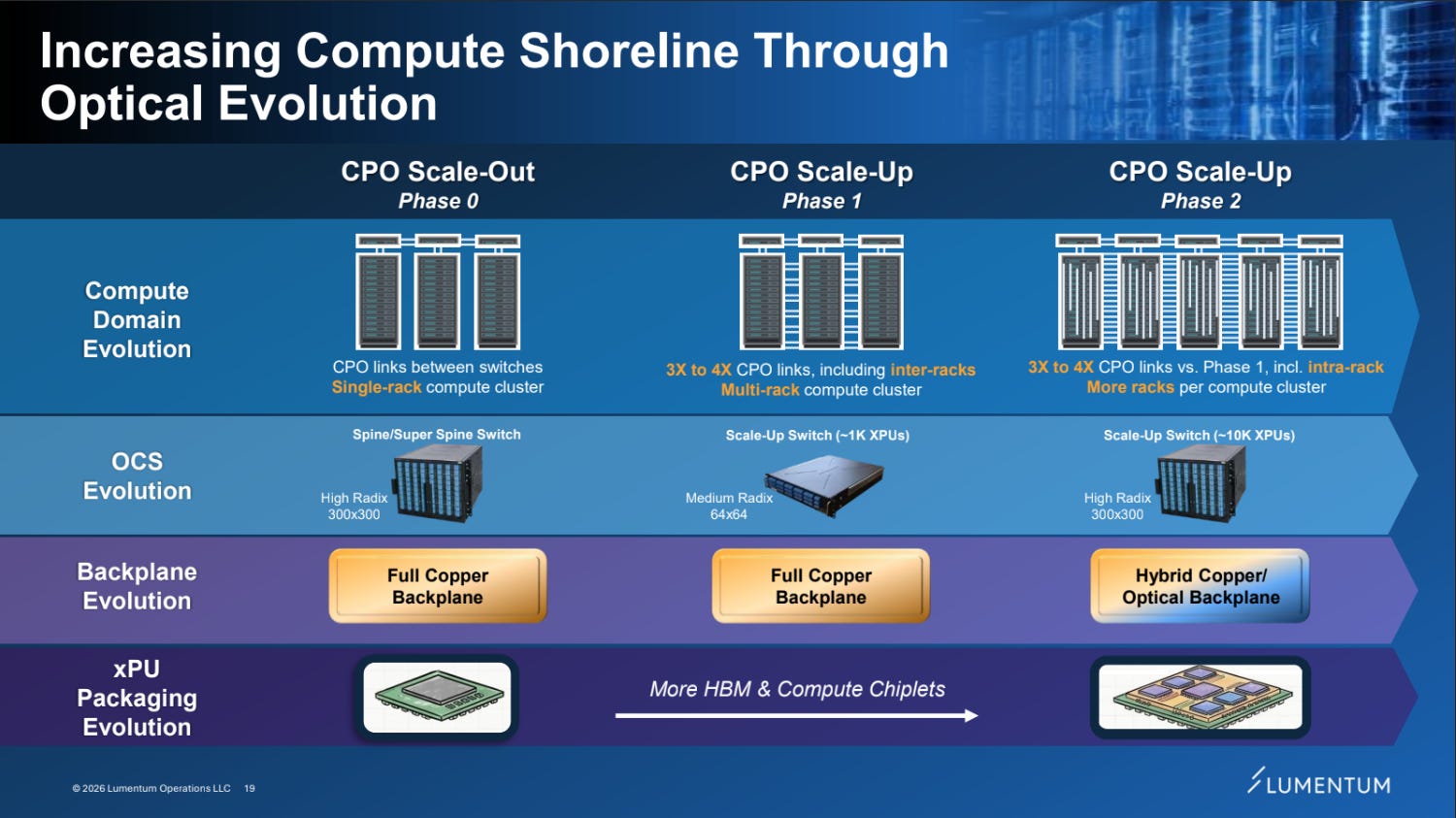

The second layer to the exponential is the CPO copper replacement story itself. Within this layer, there are three more sub-layers. That is, we can split CPO adoption into three phases, each with half an order of magnitude more CPO content than the last.

Phase 0 is scale-out CPO. This actually doesn’t add any new optical content for the total market, but it does add CPO content for the CPO vendors. In Phase 0, transceivers that connect switches in the scale-out network are replaced with CPO. Though it’s a little bit confusing because the ramp happens first but happens the slowest. This does not mean that transceivers will all of a sudden disappear.

Phase one is inter-rack scale-up CPO. This is the art of taking multiple racks, which are usually their own scale-up domain (one coherent piece of compute to the software), and linking them together with optics to make an even larger scale-up domain. This is represented by NVIDIA’s NVL576 Oberon solution for their Vera Rubin platform.

Phase two is intra-rack scale-up CPO. In this final phase, we are ripping out all the copper SerDes and interconnects of a single rack and replacing it all with CPO. As you may imagine, this has by far the most CPO content out of any of the phases, but is also very far away.

Lumentum has this slide at OFC which describes it. They are very excited, as you may imagine.

The timing is also important. CPO is not going to happen as soon as the most optimistic bulls think.

Volume shipments of phase one scale-up CPO will not occur until the Feynman generation. This is despite Rubin Ultra having the NVL576 Oberon 8-rack system, as this will ship in far less volume than regular Kyber NVL144 and Oberon NVL72.

But I’ve, of course, been a very vocal CPO bull. So where do I stand on this?

I think what is underrated about CPO is, instead, its inevitability and sheer VOLUME. People simply do not understand how much CPO will be needed once it actually does ramp.

Anyways, let’s talk about all of the widgets needed for CPO and the different widget makers in the CPO supply chain.

Contents

InP Substrate

Epitaxy

Laser

Optical Engine

Conclusion

AXTI

Aixtron

Lumentum

Coherent

Soitec

Tower Semi

My Ranking (and Positions)

SemiAnalysis Giveaway: The first person to subscribe using the paywall on this post will be selected to receive one free month of SemiAnalysis (sent to your email).

By accessing this content, you acknowledge and agree to our terms and conditions. This research is not financial advice.

InP Substrate

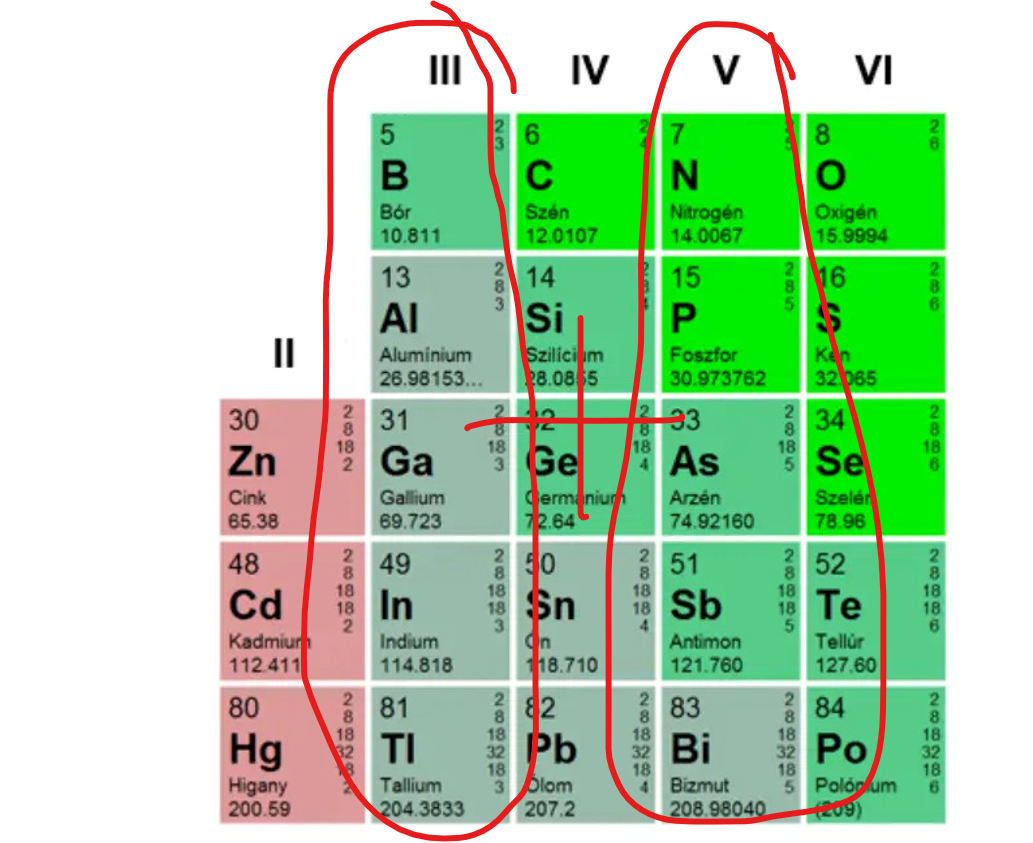

InP is the pure laser raw material. Indium + Phosphide is a III-V (named after periodic table columns) compound which has a direct band gap, meaning that it can emit light, unlike silicon.

This chemical is very hard to make. You must refine high-purity indium (99.99999%) and phosphorus and then grow this compound into an ingot. It’s really hard to grow this stuff. This isn’t memory, where it’s a commodity. You gotta get qualified and develop proprietary processes (like AXT’s VGF).

InP substrates are the bottleneck to end all bottlenecks.

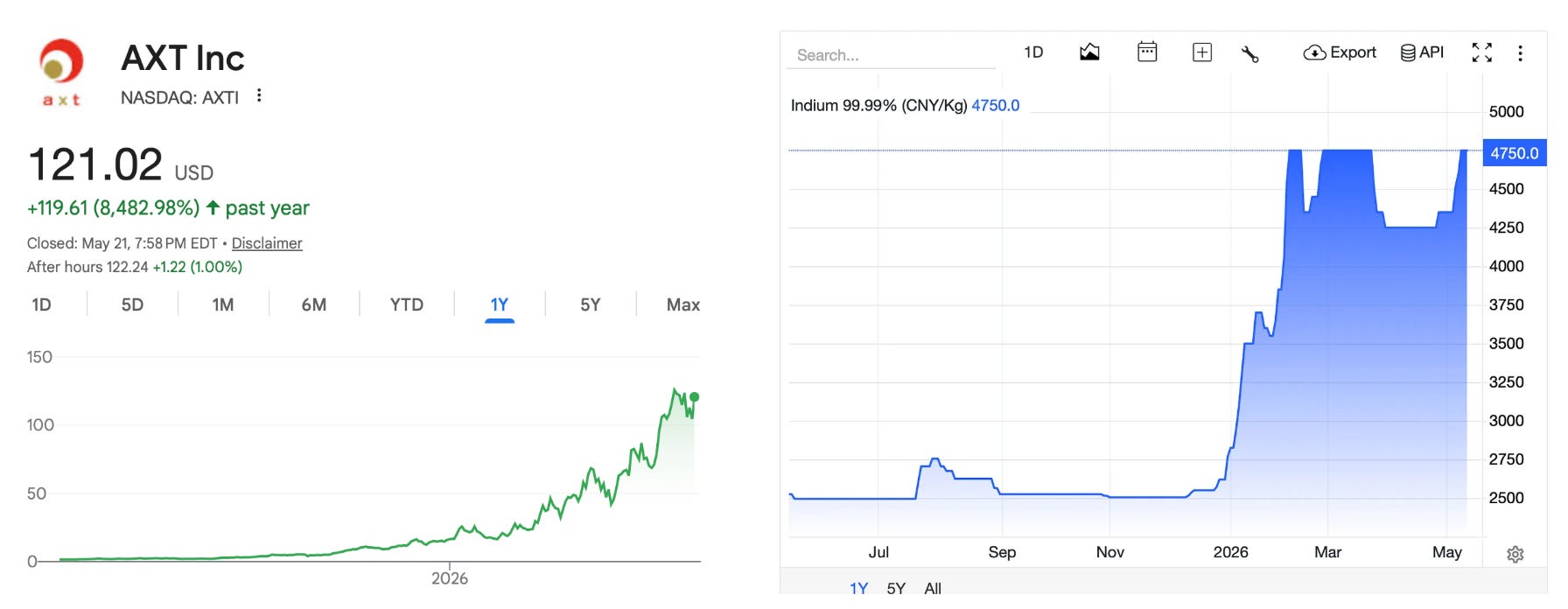

AXTI, the poster child, actually doesn’t have majority market share. They are only the second-place player with roughly 36% share, while Sumitomo Electric holds 42% share. However, I believe AXTI will soon become the largest player here, as they have the most expandable capacity due to their ability to convert gallium arsenide capacity into indium phosphide via brownfield switcheroo.

The relevance for CPO is simple: CPO lasers are high-power CW lasers that require a much larger cavity in order to be so powerful. This means the die area is much larger, and each laser a b s o r b s much more InP substrate. And then you get these lasers to grow exponentially across three phases, each with half an order of magnitude of content increase. Today, despite having no CPO ramping at all, indium phosphide is so constrained that Lumentum is 30% behind demand in just traditional EMLs. See the problem here?

The question for this market is how big the price hikes are going to be. AXT trades at something like 30x exit 2027 ARR, which is ridiculous by any traditional measures. The management team has obviously not announced any crazy memory price hikes, but we all know that eventually they are going to raise the prices. The market is obviously discounting for some level of price hiking, but we just don’t know how much it’s going to be. Bulls will say the ASPs are going to 10x. Bears say it’s only going to 2x.

Epitaxy

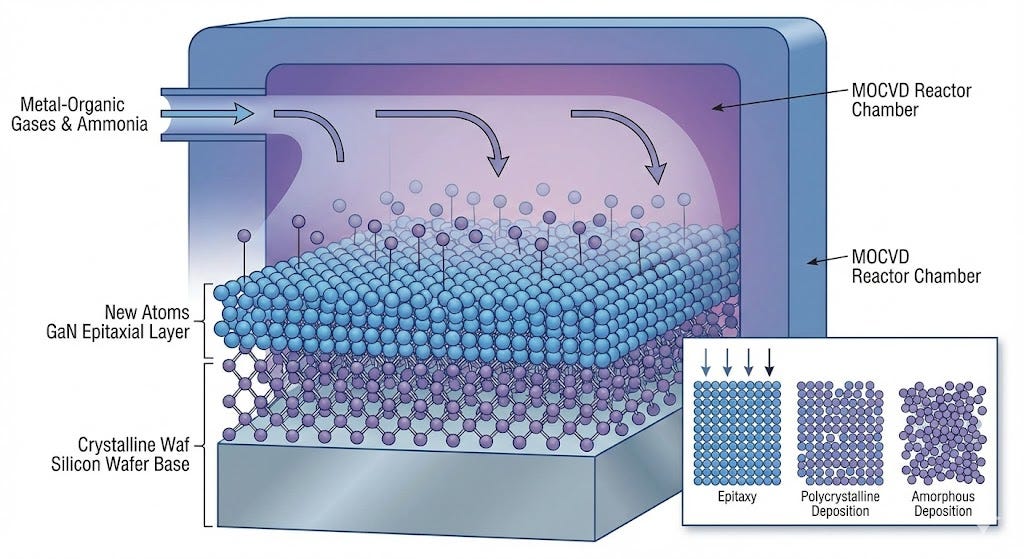

Epitaxy is the next layer. In order for indium phosphide substrates to be turned into real lasers, you have to perform a process of crystal growth called epitaxy to turn them into epiwafers first. It’s an intermediate stage.

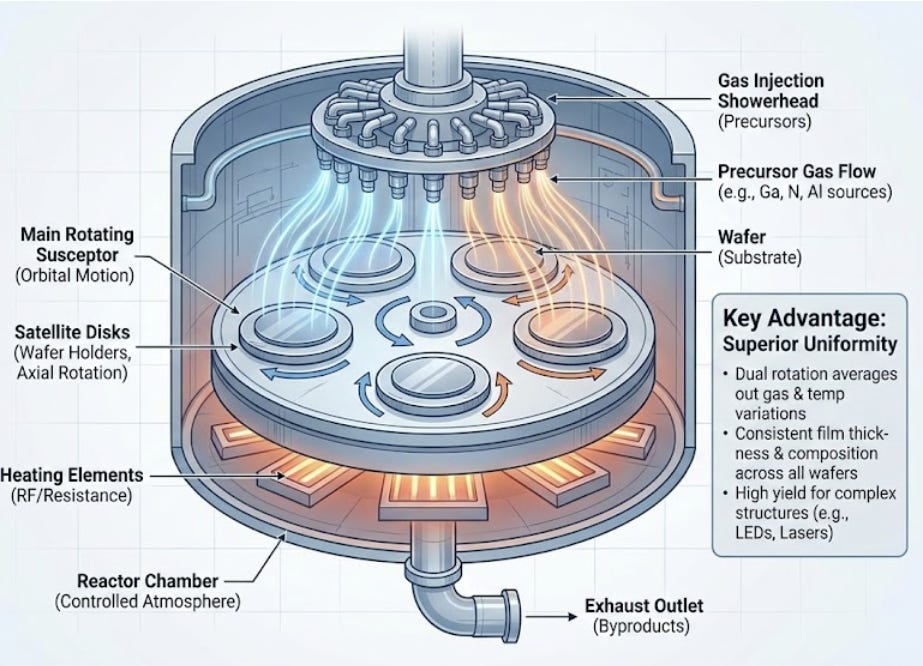

To do this, you use Aixtron’s MOCVD (metal organic chemical vapor deposition) tools. Aixtron has a proprietary process called the planetary reactor, which allows you to batch this activity. Because of this, Aixtron has a literal monopoly on this whole market. They claim “well north of 90% market share,” which is just a kind way of saying this. If you want Veeco tools, you have to throttle your throughput because you won’t have planetary reactor. Aixtron is a monopoly. You have no other choice.

Then there are the buyers of these tools and those who actually do the epitaxy-ing.

Lumentum and Coherent have this process vertically integrated, but for anyone who doesn’t, you can buy from IQE.

They are a pure-play epiwafer maker.

Laser

Once you grow the epiwafer, it goes through a more traditional compound semiconductor fab process with lithography and etch to get turned into the final laser. This is purely the domain of laser manufacturers like Lumentum and Coherent.

Since we’re only looking at the indium phosphide supply chain today, which is the vast, vast majority of CPO anyways, we are only going to consider DFB lasers and not VCSELs.

CPO lasers are high-power continuous wave lasers. This means that they have two important characteristics:

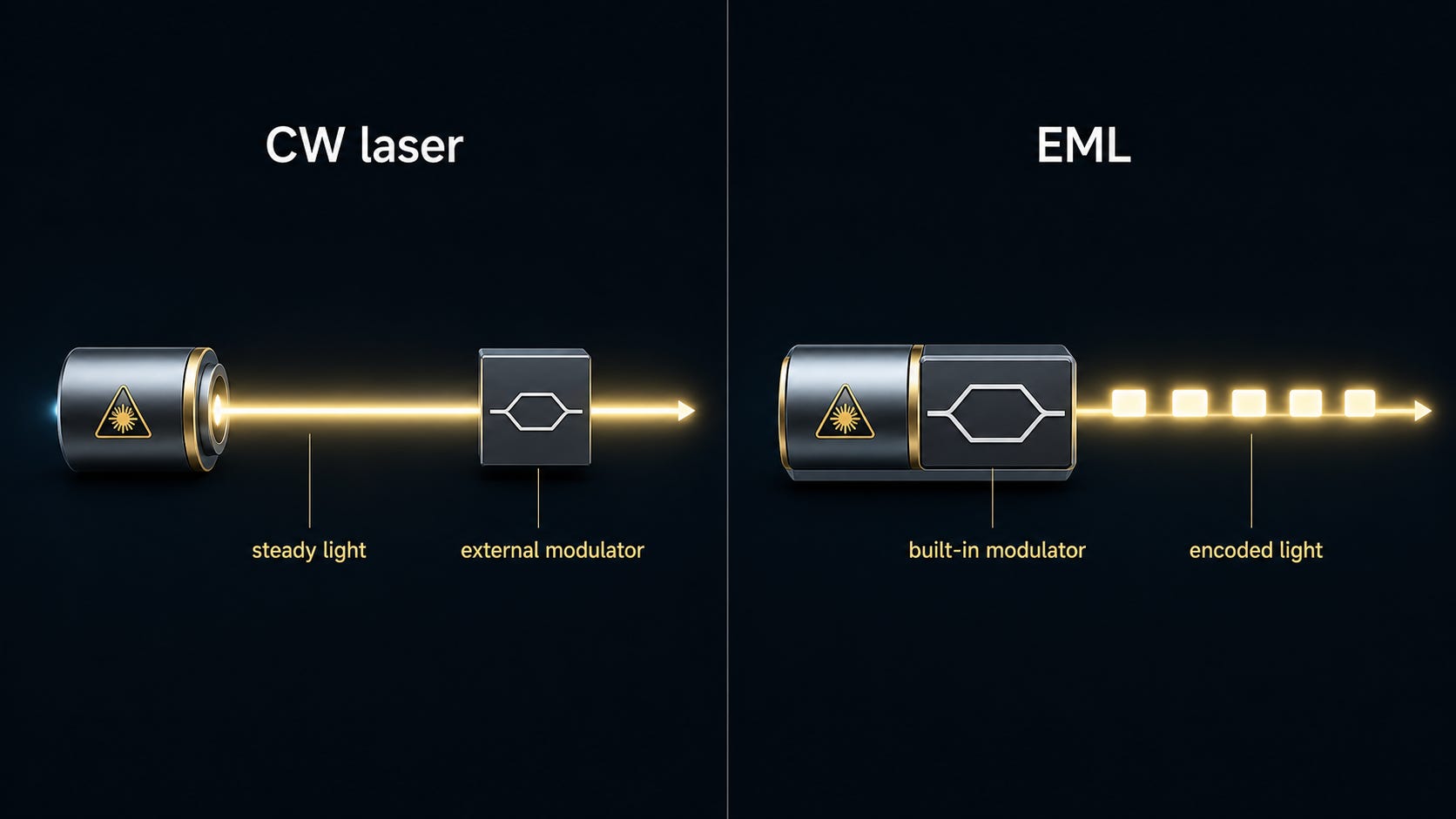

Being continuous wave (rather than EML)

Being high-power (rather than low-power)

CW lasers are lasers that just stay on. It produces a continuous stream of light, like a light bulb or flashlight. A CW laser can provide a steady beam that gets modulated (gets the signal put into it) somewhere else.

EMLs are lasers plus a built-in light switch. EML stands for electro-absorption modulated laser. The laser creates the light, and an attached modulator rapidly changes that light on/off or high/low to encode data.

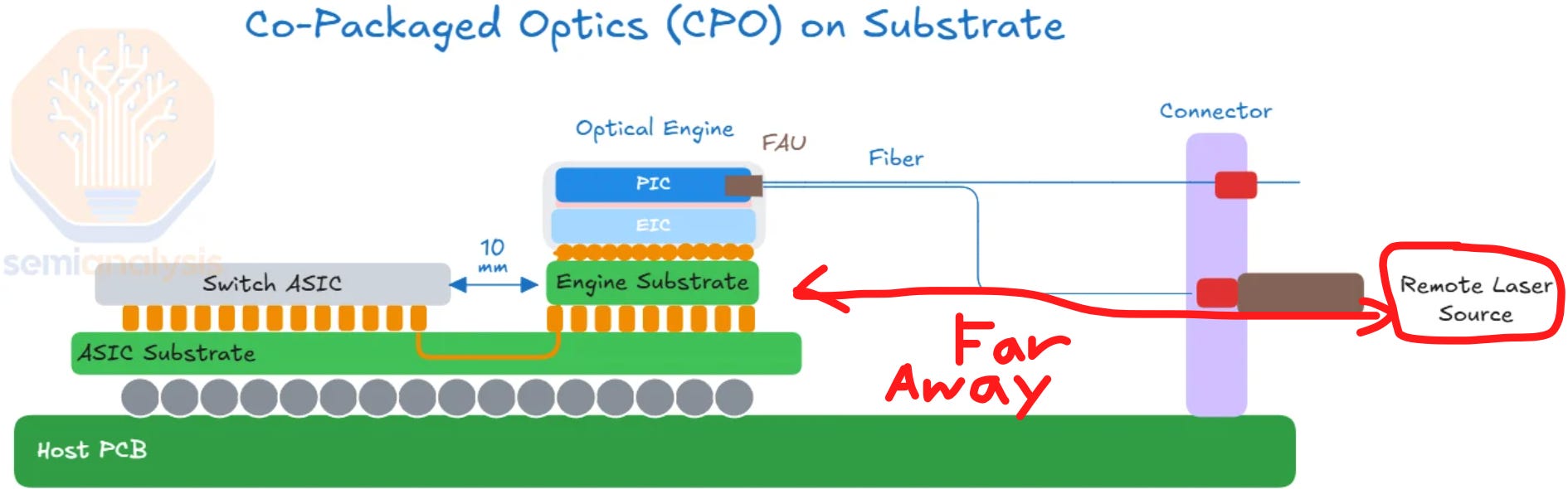

Lasers for CPO must also be placed far away from the optical engine because CPO literally stands for co-packaged optics, which means the optics are co-packaged with the chip and the chip is really hot, so if the laser is right next to the chip, it overheats and breaks and stuff.

Because this laser is so far away, in order for the light to reach the optical engine, it needs to survive a lot of coupling loss. Thus, the starting power of the light must be very high. For CPO, this means generally in the range of 400 mW rather than 30 to 70 mW of traditional CW lasers for SiPho transceivers.

The higher the laser power, the harder it is to make. These lasers must meet critical thresholds on two noise specs: linewidth and RIN. This is essentially the purity of the light. I won’t go into much more detail on noise specs, but if you’re interested, I talk more about them in this article.

High-power CW lasers are currently a market almost completely dominated by Lumentum.

Optical Engine

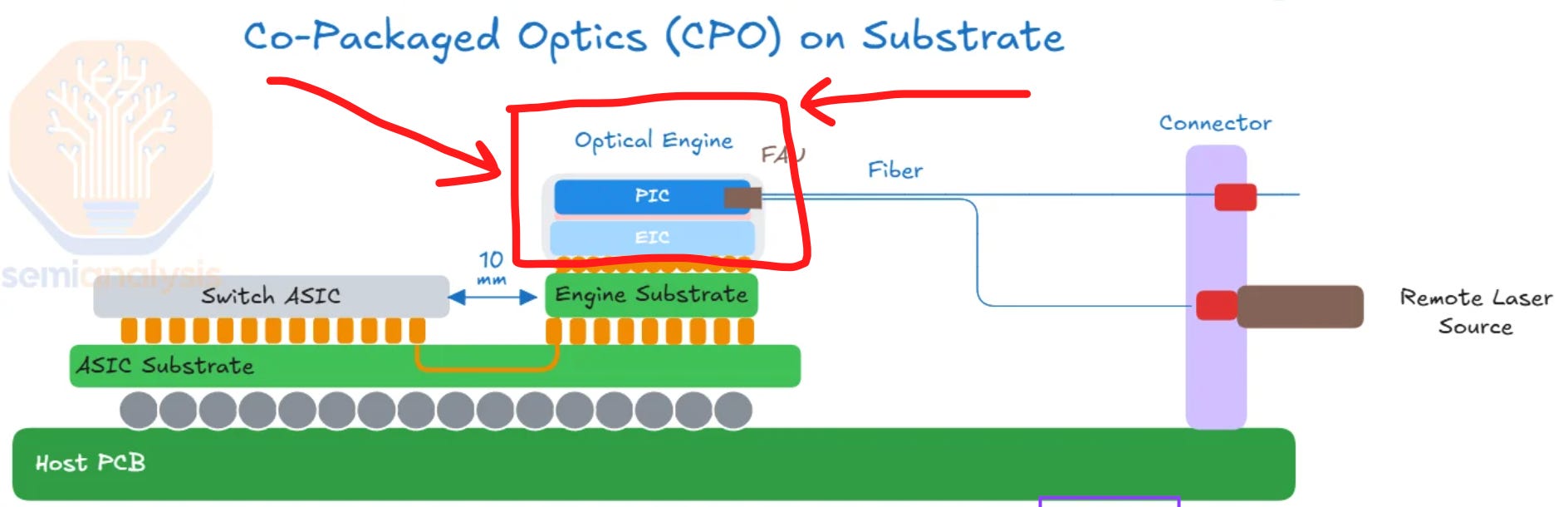

CPO lasers are CW, which means that in order to actually use it to communicate signal and not just be a flashlight, you need external silicon photonics components to do something with the light.

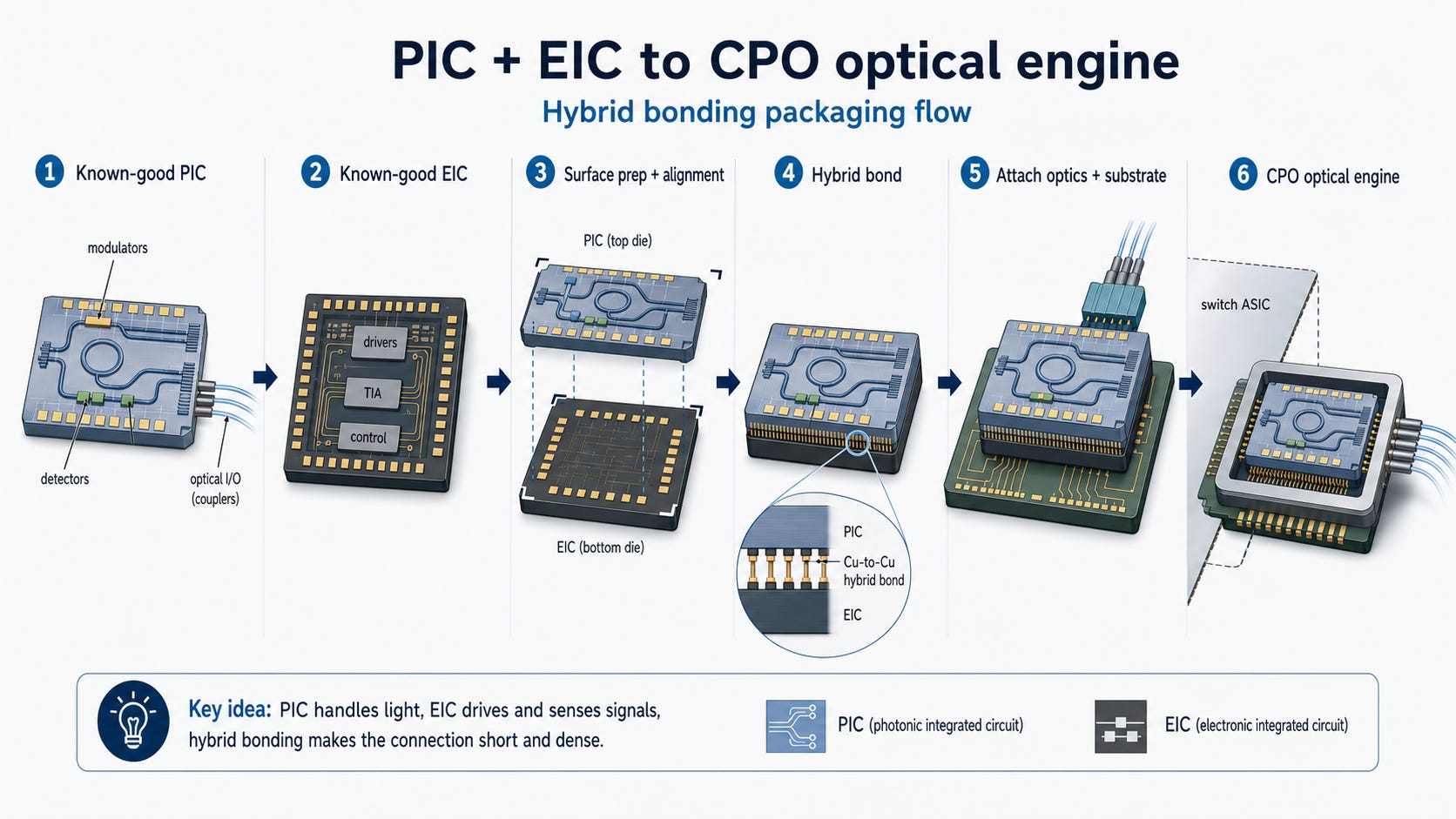

The optical engine is what you can see in the above diagram of the CPO. It is made up of a photonic integrated circuit, or a PIC, and an electrical integrated circuit, or an EIC, hybrid-bonded together (using something like TSMC’s COUPE). The EIC is your standard logic chip. The PIC is a SiPho chip. It is the SiPho PIC which actually modifies and modulates the light, but both of them come in a package whenever we are thinking of CPO. Here is an article if you want to go deeper into SiPho.

There are three layers to making an optical engine:

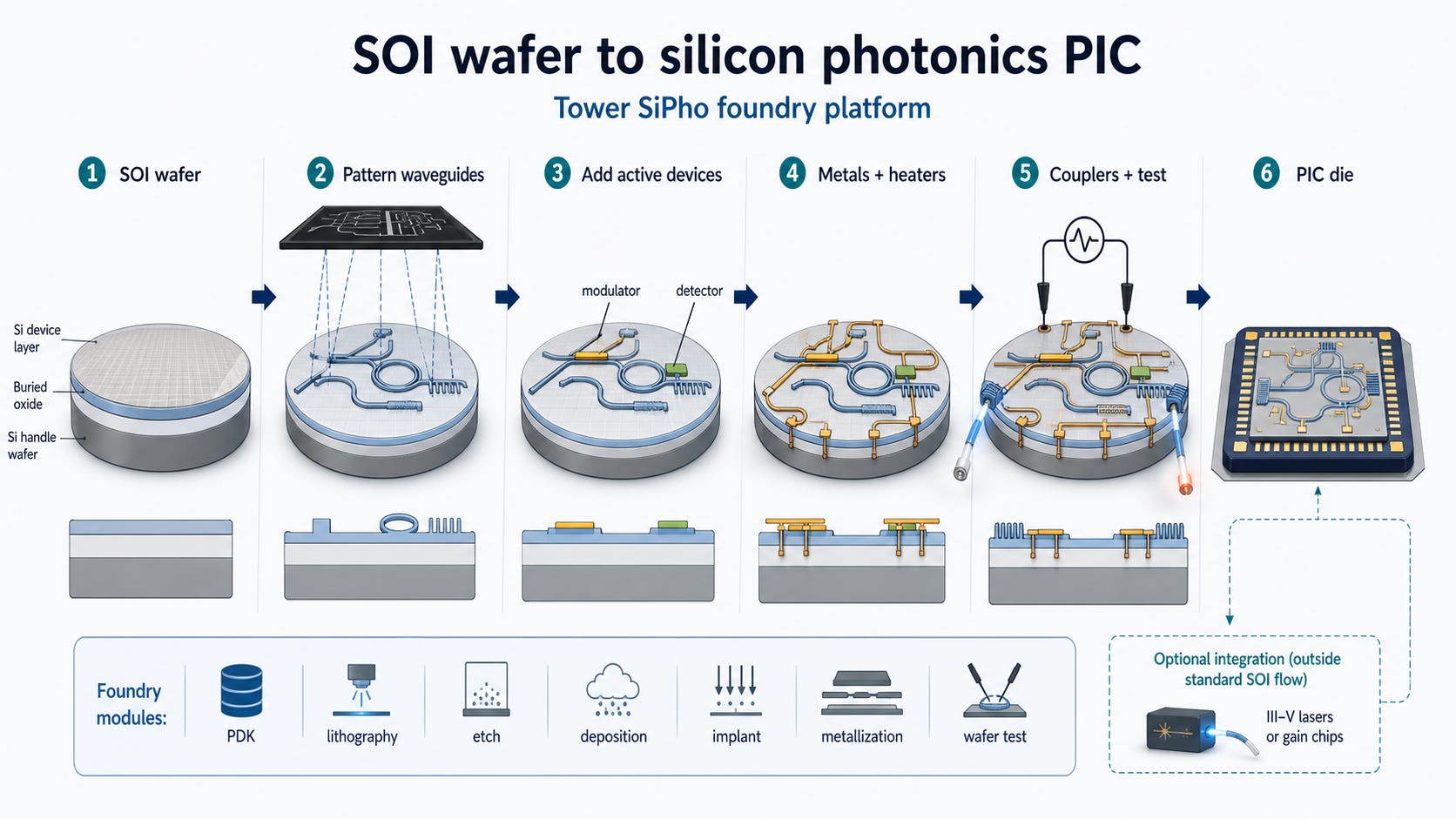

Making the SOI wafer

Fabbing the PIC in a foundry

Hybrid bonding the PIC to an EIC

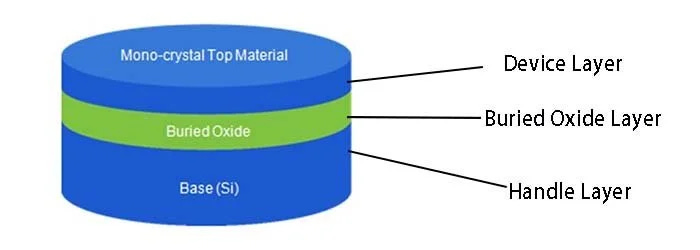

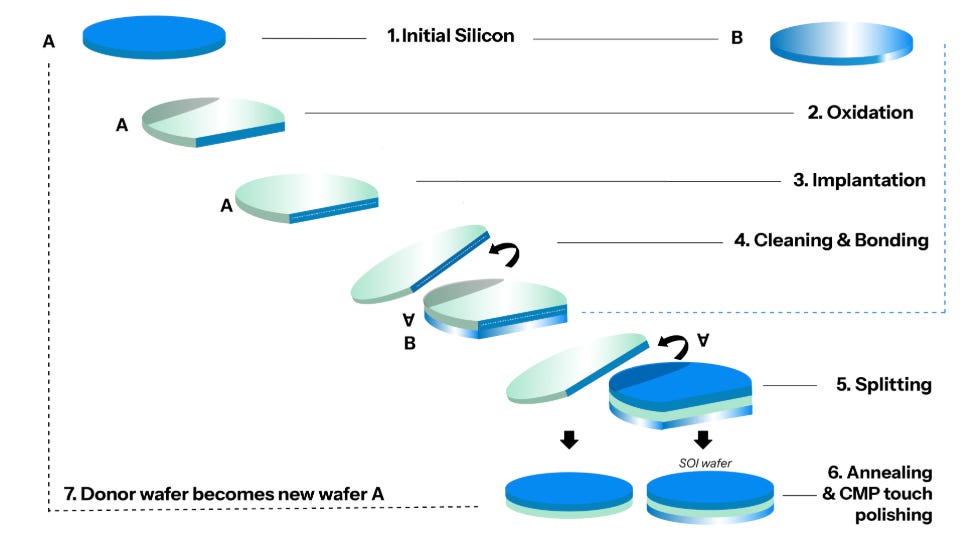

SOI stands for silicon on insulator. It’s basically a silicon sandwich and needed to contain the light waves as they travel through the waveguides.

Soitec is a monopoly here. They control the majority of the IP needed to make these wafers, which they call Smart Cut. Just like with indium phosphide, this is a very difficult process.

I cover this topic a lot more deeply in this article.

Tower Semi is the leading silicon photonics foundry.

Soitec provides the starting wafers that go through Tower Semi’s specialty foundry manufacturing process to become a fully fledged PIC.

They are the best at it. Globalfoundries and TSMC also play in this market, but Tower CEO has specifically flagged and quoted that they have by far the highest market share.

When Krish Sankar of TD Cowen asked Russell about market share, Russell said:

“There’s other people that claim very high market shares. I don’t see how it’s possible at all.”

LOL

Finally, the PIC and the EIC need to be hybrid-bonded to form an optical engine, and the leading platform here is TSMC’s COUPE. TSMC did something really smart here, which is that they require that the PIC is fabricated at TSMC in order to use their COUPE packaging. Now their customers have to choose between the superior PIC manufacturing of Tower Semi and the superior EIC and packaging capabilities of TSMC.

Currently, it is COUPE that has won NVIDIA CPO ramp.

Conclusion

The big takeaway you should have here is that every step in the CPO supply chain (especially the raw materials) is physical and linear. Nothing here is built to handle exponential demand. Everyone has capacity limitations.

However, refining indium phosphide substrates, building MOCVD machines, growing epiwafers, manufacturing lasers, and fabbing PICs all have different capacity dynamics: different speeds of adding shipment volume, different capital intensity, and different substitutability. It is by understanding these dynamics through a lens of perpetual supply constraints and exponential demand, you can identify which companies stand to benefit.

Below I will give my opinions on AXTI, Aixtron, Lumentum, Coherent, Soitec, and Tower Semi, give you revenue builds/EPS estimates for all of them (making the same assumptions about the total industry-wide unit shipments), and share my personal ranking based on my opinion and the positions I have.

Yes, you heard that right. That’s six models!

I also call out why AXTI could still have the most upside, how I modeled the bombshell Aixtron dropped on their last earnings call, why Coherent management speak makes me believe they are uncompetitive, and a very interesting (!!!) component ratio dynamic between Soitec/optical engines and Lumentum/ELS.