Why Anthropic Is a $100T Company

And how you can play it right now (ultra-long-form article)

ANTHROPIC IS THE MOST VALUABLE COMPANY IN THE WORLD, AND IT’S NOT EVEN CLOSE.

I don’t understand why this topic isn’t talked about more. In public equities, we look at every company, calculate their 2-3 year out revenues and earnings using detailed supply chain analysis, evaluate their competitive positioning, analyze their engineering in data sheets, build multi-tab quarter-by-quarter financial models, and apply the fairest valuation that we can.

And yet even then, we can get price charts (which is essentially the change in valuation over time where investors say “we got it wrong”) that look like this.

Thousands of market participants and investors in mid-2025 were wrong about this one company’s valuation by a factor of almost 100 times. Think about that for a moment. These shares were changing hands for almost 1% of what they are worth today. They were wrong. So wrong. Dead wrong.

And they are wrong about Anthropic today.

The 1 trillion-ish valuation is not really questioned too much. But once you start asking questions, you realize that there is completely zero chance it is anywhere close to big enough.

Today, I will justify a $100 trillion valuation for Anthropic as a fun thought exercise to show just how undervalued the model labs are. In reality, it is completely silly to claim that a company already worth nearly a trillion dollars will increase in value over 100-fold and become 20x more valuable than the current most valuable company in the world. The point of this exercise is to show that it is logically plausible. It is within the realm of possibility. If the ceiling is this high, at least we must be thinking in the wrong order of magnitude today.

Abstract

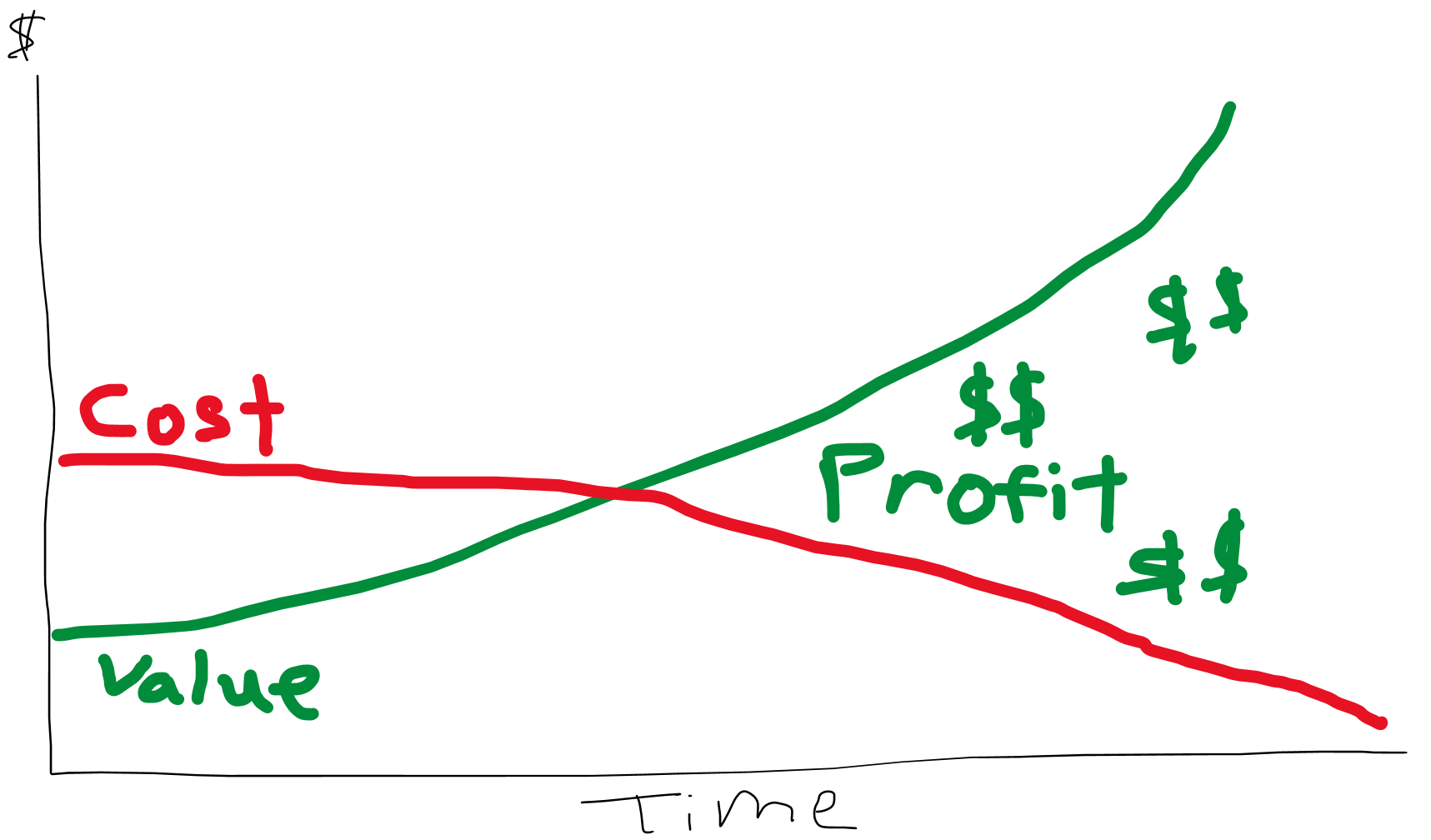

Model Labs are the greatest businesses of all time. Tokens increase in value over time as frontier models become more capable and able to automate longer time-horizon tasks, unlocking new use cases and increasing willingness to pay. Meanwhile, they decline in cost over time due to both hardware efficiency gains and algorithmic improvements in the models themselves. The combined effect of higher value at lower cost increases profit non-linearly, creating a near infinite terminal value. They are able to defend this attractive business because their moat strengthens over time via recursive self-improvement.

Anthropic’s $45b ARR represents growth never before seen in capitalism’s history, and using a Gompertz-style power law curve, we estimate its exit CY26 ARR at $300 billion, its exit CY27 ARR at $1 trillion, and exit CY28 ARR at $1.5 trillion. Yet it is absurdly still valued on trailing and current-year financials. We believe that it is a fallacy to not apply a far out forward multiple to the model labs like we do with high growth high margin public software companies like Palantir and Cloudflare. Doing so, we arrive at our $100 trillion valuation. Despite being optically unreasonable, this valuation is theoretically supported by the idea of the technological singularity, a concept commonly cited by AI theorists but that not yet entered the investment discourse.

However, retail access to this company is heavily gated and the IPO dynamics are incredibly unfavorable to retail investors. This is why I share a trade I have entered providing near 1:1 economic exposure to Anthropic to hedge against the IPO.

Contents

Model Labs = Greatest Businesses of All Time

Increasing Value Over Time

Declining Cost Over Time

Strengthening Moat Over Time

Revenue and Valuation

Estimating CY26 ARR

Public Markets and Forward Numbers

Estimating CY27 and CY28 ARR

Margins

Valuation

The Singularity

The IPO

How Retail Investors Can Play This

This is a longer, higher quality article than usual. Because of the time it takes me, I will only be able to do one or two of these a week. Would you prefer two of these types of higher quality articles or five articles at my usual length and depth? Earnings coverage is not impacted.

SemiAnalysis Giveaway: The first person to subscribe using the paywall on this post will be selected to receive one free month of SemiAnalysis (sent to your email).

By accessing this content, you acknowledge and agree to our terms and conditions. This research is not financial advice.

Model Labs = Greatest Businesses of All Time

The popular media has it backwards. Model Labs are the greatest businesses of all time.

Model labs share a unique combination of characteristics that provide them with a near infinite terminal value:

The value of their product rises over time.

The cost of their input declines over time.

The moat strengthens over time.

As a result, the leading model lab(s) are currently on a fast track towards a monopoly position on all future intellectual and knowledge-based labor, an addressable market comprising most of global GDP.

Increasing Value Over Time

As AI models become more powerful, the value delivered by Model Labs per token rises accordingly. This is intuitive, as smarter models can do more useful things.

As the task set that models can accomplish broadens, people start discovering new ways to use models that have never been discovered before. It is only because of improving model capabilities that the agentic AI phenomenon, widely considered to be as important as the ChatGPT moment, was able to materialize.

Two of the most important examples for how more powerful models have delivered value through agents are Claude Code and OpenClaw.

Claude Code

The term vibe coding was coined by Andrej Kaparthy approximately one year ago.

At that time, when the leading model was Sonnet 3.7, vibe coding was heavily looked down upon and discouraged. I tried to build apps with it too and failed miserably. It will run into bugs and then run around in loops, building up more technical debt and fixing nothing.

Today, with Opus 4.7, Claude code is completely conquering software engineering as it is quickly moving towards 10% of global GitHub commits.

And it hasn’t stopped at just conquering coding. The only difference between an LLM and an agent is its harness: what tools it is given, what software it can access via API.

Now, most knowledge tasks can be automated via these agentic harnesses (which seem to improve just as fast as the models themselves). Agents can perform knowledge work far cheaper than humans, as shown by SemiAnalysis in one of their most recent articles.

Which also led to Doug O’Laughlin’s famous Claude Code psychosis and Anthropic’s ARR compounding at 50% month over month in 2026.

OpenClaw

A similar phenomenon happened with OpenClaw. As the model capabilities enabled longer horizon tasks, an open-source harness that enabled such work inevitably gained immense popularity.

And while OpenClaw hype has died down a bit, usage has not. Funny enough, I am the best example of this. While I talk about OpenClaw way less nowadays, I use my claws more than ever before.

Cron jobs are especially valuable. For example, a common use case in consumer SaaS is to provision a customer service agent, running once per day to respond to requests and modify the account information of real users. Without the significant improvements and model capabilities that occurred over the past year, this would not be a realistic use case, and if it wasn’t realistic, the harness would have never been developed.

Declining Cost Over Time

As the value of a token has risen, the cost to produce it has declined.

NVIDIA’s hardware enables multiple OOMs of efficiency gains in inference every generation.

This is because, with each generation, we get more flops, more memory, better software, lower precision, algorithmic improvements, and a larger scale up domain. Each effect compounds on the other.

But it gets even better. While the hardware becomes more efficient, new models are also getting trained.

This is Leopold’s graph from 2024 because I couldn’t find one more recently that expresses this same idea lol. I can assure you that nothing has changed. The cost of an Opus 3.7 or GPT-5 level model is likely 1% of what it used to be, as DeepSeek V4 Flash is basically free.

Over time, as the value provided rises and the costs drop, profit increases non-linearly.

This is different from ordinary operating leverage, which is just part of the normal course for a business as it matures and has a structural ceiling. This phenomenon for Model Labs is structural and unbounded.

I really need to emphasize this. Every year that passes, the input cost declines while the value provided rises.

There is no other business in which this phenomenon applies. It is this that differentiates the Model Lab from the semiconductor industry. In a way, our revenues are their costs, and we sadly rely on Jevons’ Paradox to drive growth (look at the line). They do not require Jevons’ Paradox at all, as they in fact benefit from technological advancement in both directions.

Strengthening Moat Over Time

The economic argument against this “perfect” business model is, of course, competition. If the profits increase non-linearly, new entrants are also incentivized non-linearly as well, which is why my next argument is that the Frontier Labs also have a moat that strengthens over time.

Over the past two years, there have been several moments where the general consensus declared frontier models a commodity. The most prescient examples are the months following the Deepseek release and the disappointment over GPT-5 back in mid-2025.

The argument is really seductive. Think about it: all it takes is a bunch of compute and a bunch of data to train a frontier model. That means that anyone with tons of capital can do it. It just becomes a very capital-intensive commodity, something like memory.

However, over the course of late 2025 and the first half of 2026, this has been proved to be completely untrue. OpenAI and Anthropic have decisively regained the lead in agentic model development, leaving even their relatively more well-capitalized competitors far behind, and are now even widening the gap.

Google Gemini briefly achieved SOTA status in November but has quickly exited the discourse as they did not have a competitive agentic coding offering. xAI and Meta used to be near the frontier in 2025 but are now significantly lagging as well. It is only Anthropic who has grown their ARR 5x in 2026. None of the other labs are even close to having the same level of commercial success. This shows that by providing a superior product, one company is rapidly gaining market share and becoming vastly more difficult to dislodge by the day.

Open Source

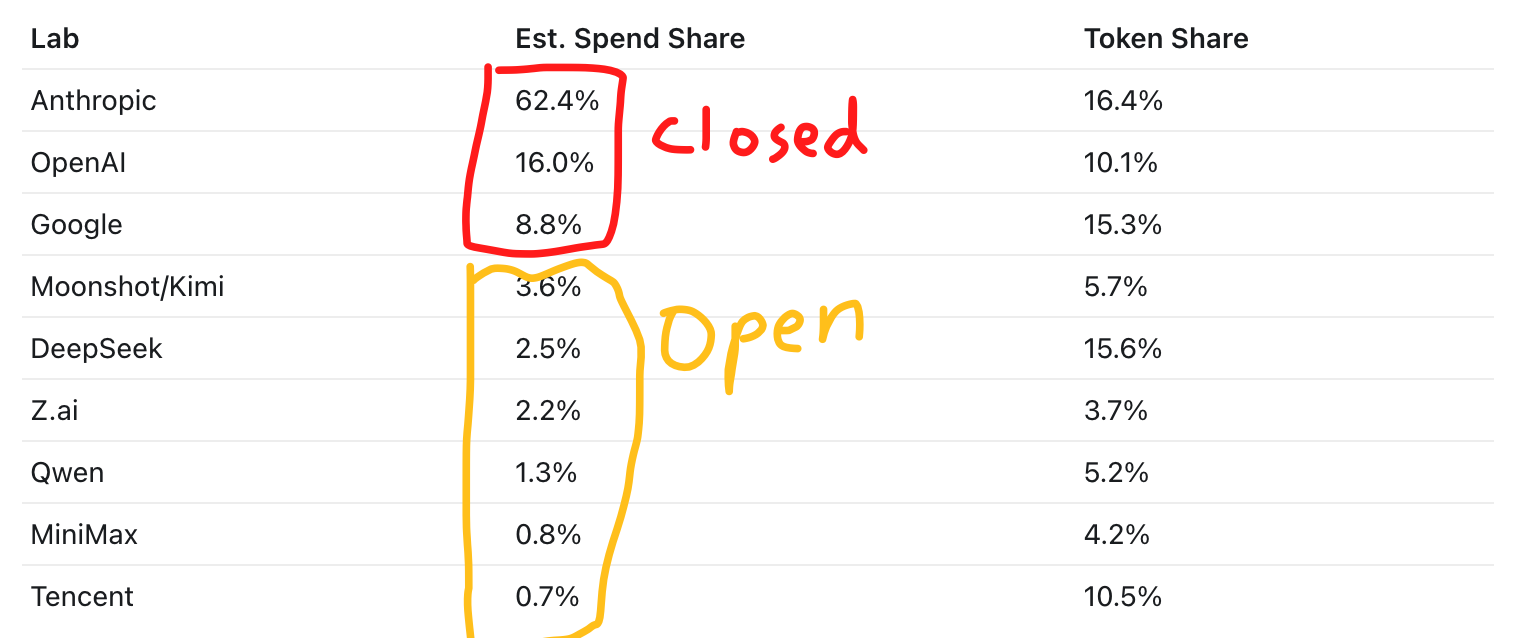

Now I will address the common counterargument that open source models are within striking distance of the frontier on benchmarks while being a fraction of the cost, and instead, show that the gap has been widening over time.

There are three reasons why benchmarks are imperfect:

Benchmarks are not representative of real-world tasks. Humanity’s Last Exam and similar benchmarks measure esoteric knowledge in a multiple choice setting not whether or not you can do an economically valuable task, like update an Excel spreadsheet with financial data pulled from a 10-K.

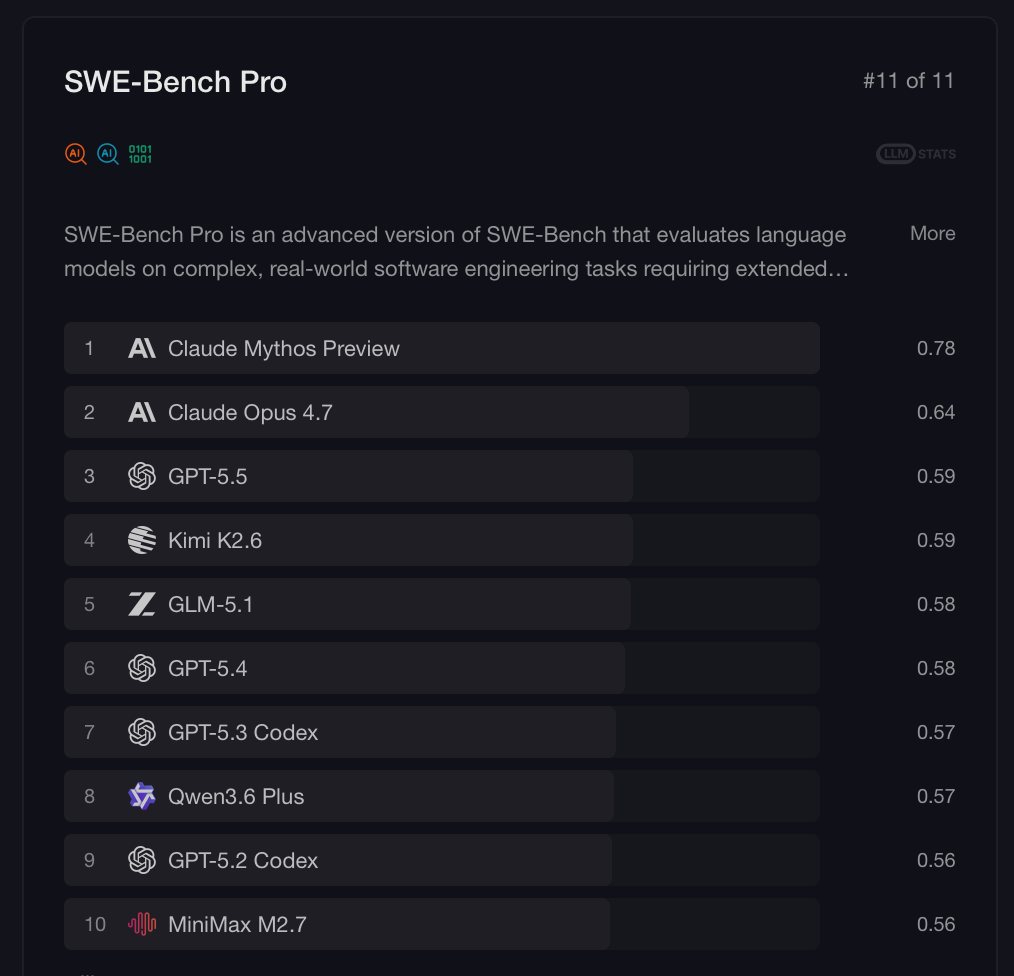

Coding benchmarks, like SWE-bench, have a dual-sided sample problem. Either the coding issues that were scraped from GitHub are not well-defined or are flawed, or the models started memorizing the answers to these benchmarks themselves.

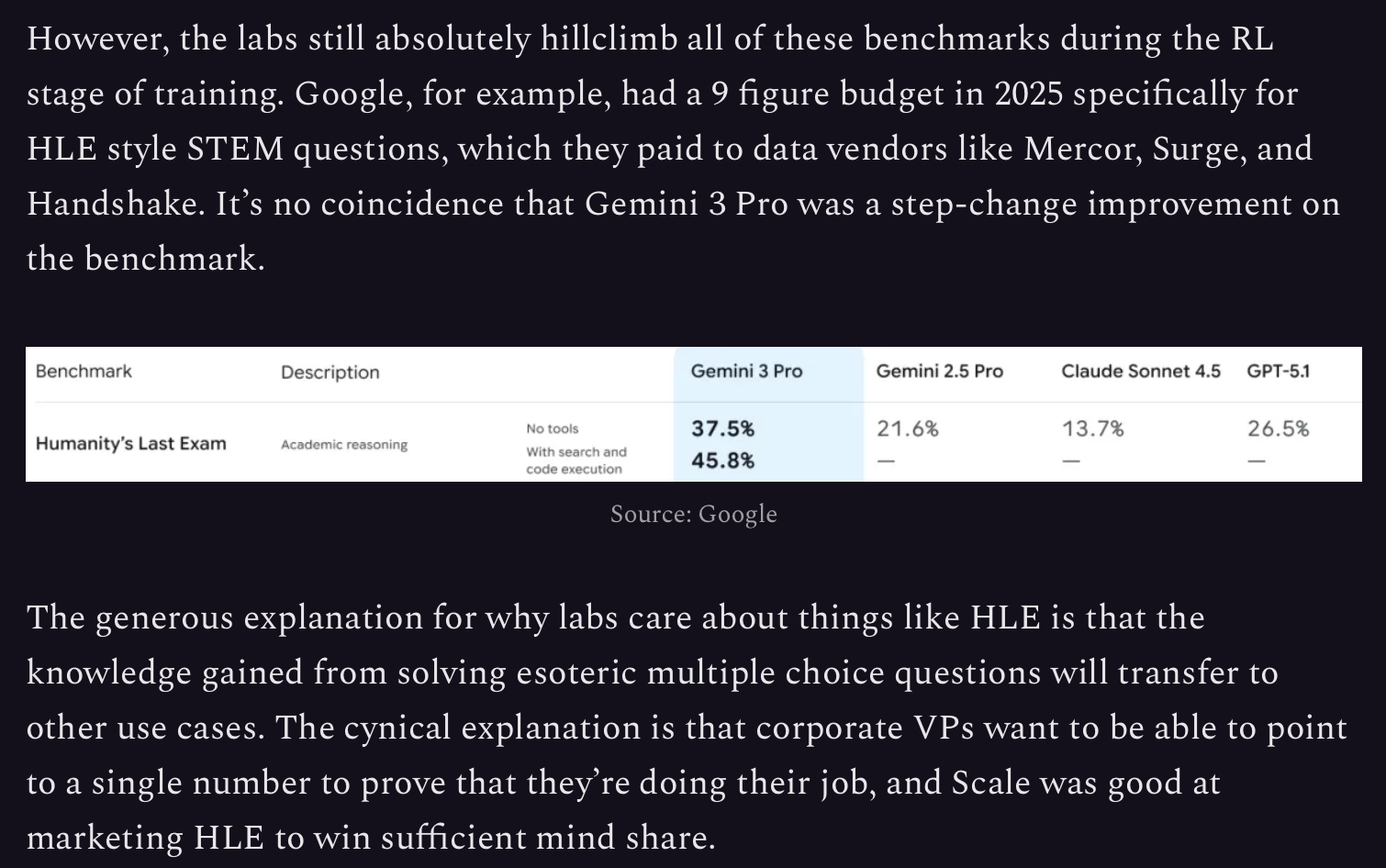

Most importantly, labs are incentivized to hill climb these benchmarks in RL, therefore optimizing for a high score rather than for real-world viability.

The best measure of the capability of the model is probably just simple market share. If people are willing to pay for it, it is likely because it is creating value for them.

Using open router data, we can see the token share of the various labs and then back-solve to get the spend share based on the price of those tokens. And this is where we see Claude completely dominate.

In addition, keep in mind that this is for open router only. Openrouter only makes up about $1.5 billion of annualized token spend, which is peanuts (1/30 of Anthropic’s current $45 billion ARR).

If these open source models were really at parity with a fraction of the cost, why would anybody pay Anthropic a single dollar?

Recursive Self-Improvement

So, what is the structural reason behind the widening lead of Anthropic?

I believe it is recursive self-improvement, a concept you have probably heard of somewhere in the AGI-pilled-San-fransisco-X discourse.

The simplest way to frame it is that although every company has access to frontier tokens, model labs have it the cheapest. They can consume their own tokens at cost, instead of paying 80% gross margin (a 5x markup). As the value of tokens rises over time, access to tokens becomes a larger and larger portion of the success of any firm and the input to any good or service. Model labs take advantage of it the most.

The evidence for this is multi-fold.

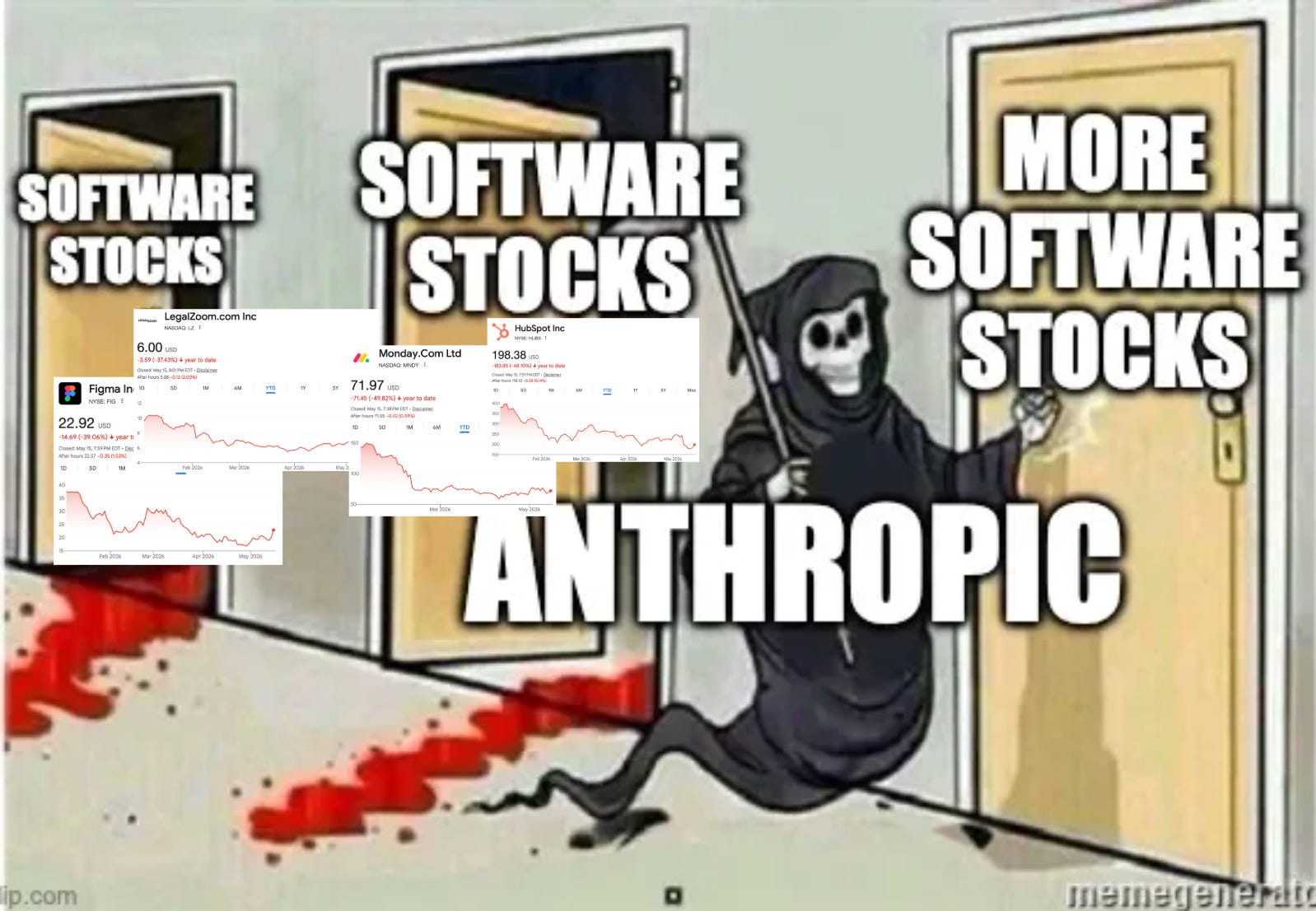

First, from a vibes-based perspective, Anthropic has clearly been shipping like crazy in 2026. There was that famous story where they shipped Claude CoWork in two weeks because they had Claude Code. That was back in January, and everyone was insanely impressed.

They also literally caused the entire SaaSpocalypse.

However, it’s not just vibes. They have objectively been shipping faster.

Perhaps the far more important application of recursive self-improvement is the automation of model development and AI R&D itself. This concept is heavily outlined in the “AGI maxi” literature through pieces like AI 2027 (2025), SITUATIONAL AWARENESS (2024), and The Coming Technological Singularity (1993!!).

The idea is that really smart AI will make AI research faster, which will then develop even smarter AI, and so on. This is the general concept known as the singularity. It was mostly theoretical, so discussions around it as an input to investment analysis were pretty much non-existent. But now Anthropic is actually making this happen.

You can see a clear speedup in model release cadence after Opus 4.5, widely considered to be the first truly autonomous agentic model. Mythos was also a step function above the current scaling laws, and the most important model release in this timeline (even more so than Opus 4.5), and it just so happened to occur in 2026, after the launch of Opus 4.5.

We will discuss the singularity in more detail later, but in terms of relevance to Anthropic’s moat, the way to frame it is that this is a turbocharged version of Helmer’s concept of Process Power in “The Seven Powers,” which is the general competitive advantage possessed by firms with decades of learning by doing, like TSMC’s node leadership.

With a substantially more capable model than its competitors, Anthropic will also have a substantially higher R&D productivity, enabling it to widen the model gap further, thereby widening the R&D lead further. It is a recursive cycle that strengthens their competitive moat over time, until they reach the status of a truly unbreakable monopoly.

Compute

The most credible bear case against Anthropic is that they are GPU-poor compared to OpenAI and Google.

Last year, OpenAI triggered the whole “AI bubble” bubble by signing massive deals with Oracle (5GW), AMD (6GW), NVIDIA (10GW), and Broadcom (10GW).

And Google is literally a hyperscaler. How are they even supposed to compete?

This is the vector by which my mind can be changed. I also have significant exposure to OpenAI-linked stocks because I believe that their compute advantage will help them outperform the currently low expectations.

However, if I had to bet on one of the AI labs, it would still be Anthropic.

The framework that I would use to think about the competitiveness of a frontier lab is a mix between compute and “taste.” Taste is a bit abstract, but think of it as an amalgamation of factors that affect how effectively the lab uses compute. This includes algorithmic efficiency, eval quality, knowing what to research, and general tacit process knowledge embedded in the firm.

compute x taste = effective compute

Anthropic has shown by far the most taste out of OpenAI and Google.

I believe that OpenAI, as many have properly criticized them for, is too distracted. They have too much emphasis on the consumer, pursuing ventures like acquiring TBPN and literally making a phone. (Like, what? Do you not realize that if you reach AGI first, you can make a phone way faster? Lmao)

Google also shares the same consumer-focused problem pouring resources into image, video, and world models, but it is worse because they don’t even have a competitive agentic harness product yet that competes with Claude Code and Codex. Maybe this will change soon with the Big Google Event (I/O), but they really have to pull a rabbit out of a hat to unwind six months of OpenAI and Anthropic’s lead.

Anthropic, meanwhile, has shown relentless focus on the one thing that matters: making more intelligent agentic coding models. They haven’t even produced an image generation model. Think about that! I use GPT Image Gen 2 every day, and it’s incredibly useful. Clearly there is demand out there for such a product, and Anthropic purposefully turned away that demand to maintain their focus.

It has been clear that this focus and taste has allowed Anthropic to develop more powerful models with less compute. I do not expect this trend to stop. In fact, having the most powerful models might even help them catch up in compute, as having a higher commercial market share, they would be the entity with the highest willingness to pay for a marginal petaflop.

Mythos

Now to tie this all together.

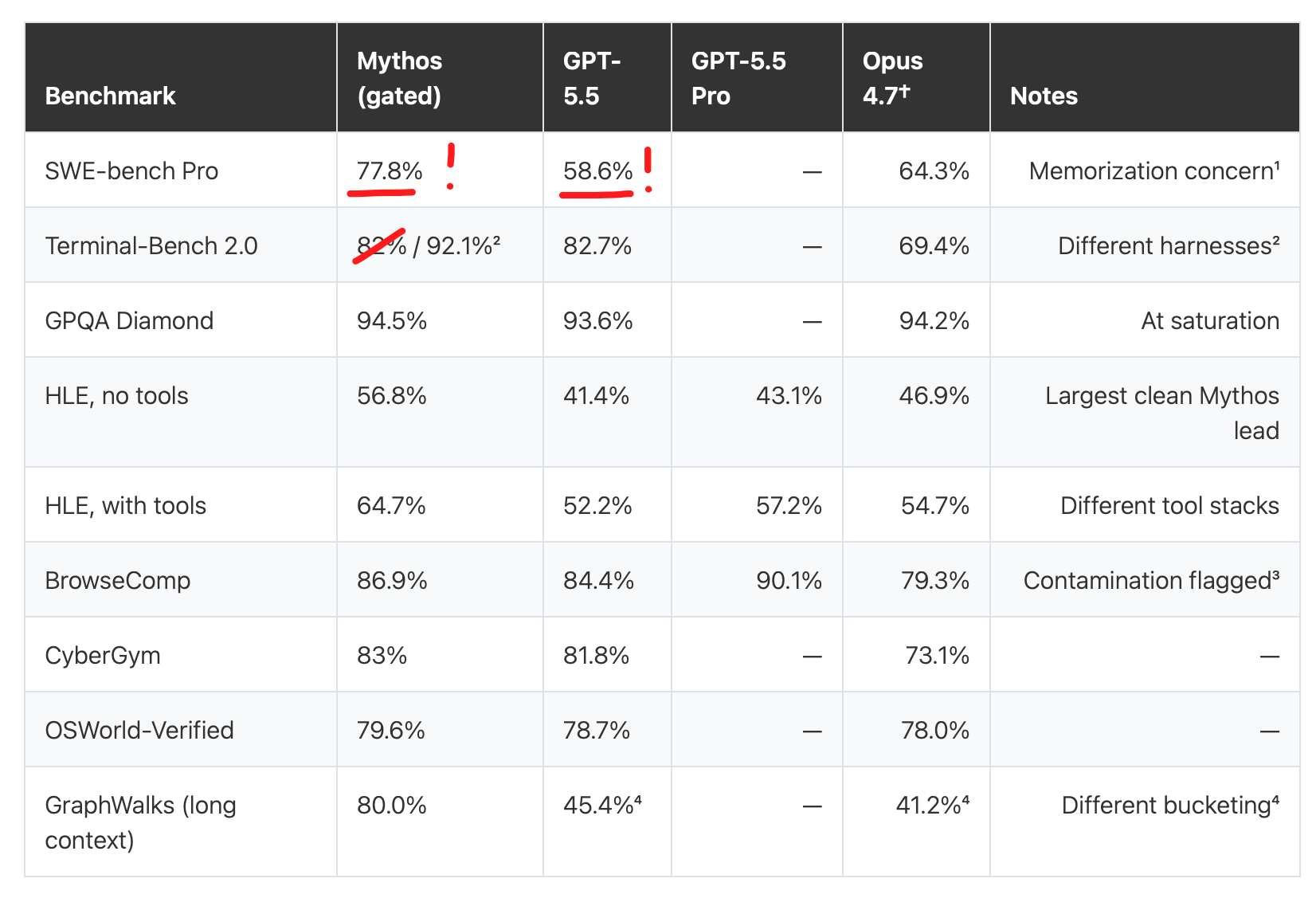

Every factor here is only working in Anthropic’s favor because they currently, according to publicly available information, have the world’s most powerful model, Claude Mythos. To be frank, if Anthropic was public, the release of Mythos should have made Anthropic stock surged by 1,000% in a single trading session, as it is the single event that significantly increased the probability of Anthropic achieving recursive self-improvement before everyone else.

On the launch of GPT 5.5, results for SWE Bench Verified and SWE Bench Pro were excluded from the model card because it significantly underperformed Claude Mythos.

However, I did say benchmarks were imperfect and real-life use matters more, but actually, this is where Mythos truly mogs.

During our testing, we found that Mythos Preview is capable of identifying and then exploiting zero-day vulnerabilities in every major operating system and every major web browser when directed by a user to do so. The vulnerabilities it finds are often subtle or difficult to detect. Many of them are ten or twenty years old, with the oldest we have found so far being a now-patched 27-year-old bug in OpenBSD—an operating system known primarily for its security.

The exploits it constructs are not just run-of-the-mill stack-smashing exploits (though as we’ll show, it can do those too). In one case, Mythos Preview wrote a web browser exploit that chained together four vulnerabilities, writing a complex JIT heap spray that escaped both renderer and OS sandboxes. It autonomously obtained local privilege escalation exploits on Linux and other operating systems by exploiting subtle race conditions and KASLR-bypasses. And it autonomously wrote a remote code execution exploit on FreeBSD’s NFS server that granted full root access to unauthenticated users by splitting a 20-gadget ROP chain over multiple packets.

- Anthropic

You all have probably heard that Mythos found hundreds of zero-day vulnerabilities across the world’s most secure software infrastructure. This is the first glimpse of a model with vastly superhuman capabilities in an intellectual domain.

Importantly, this is not because Anthropic purposefully trained a cyber security model. Mythos simply inherited these capabilities due to being much more intelligent in general.

“We did not explicitly train Mythos Preview to have these capabilities. Rather, they emerged as a downstream consequence of general improvements in code, reasoning, and autonomy. The same improvements that make the model substantially more effective at patching vulnerabilities also make it substantially more effective at exploiting them.”

- Anthropic

Anthropic is most certainly utilizing the world’s most powerful model (that no other lab has access to) to conduct internal R&D right now. It will not be long before we see the results.

Revenue and Valuation

Estimating CY26 ARR

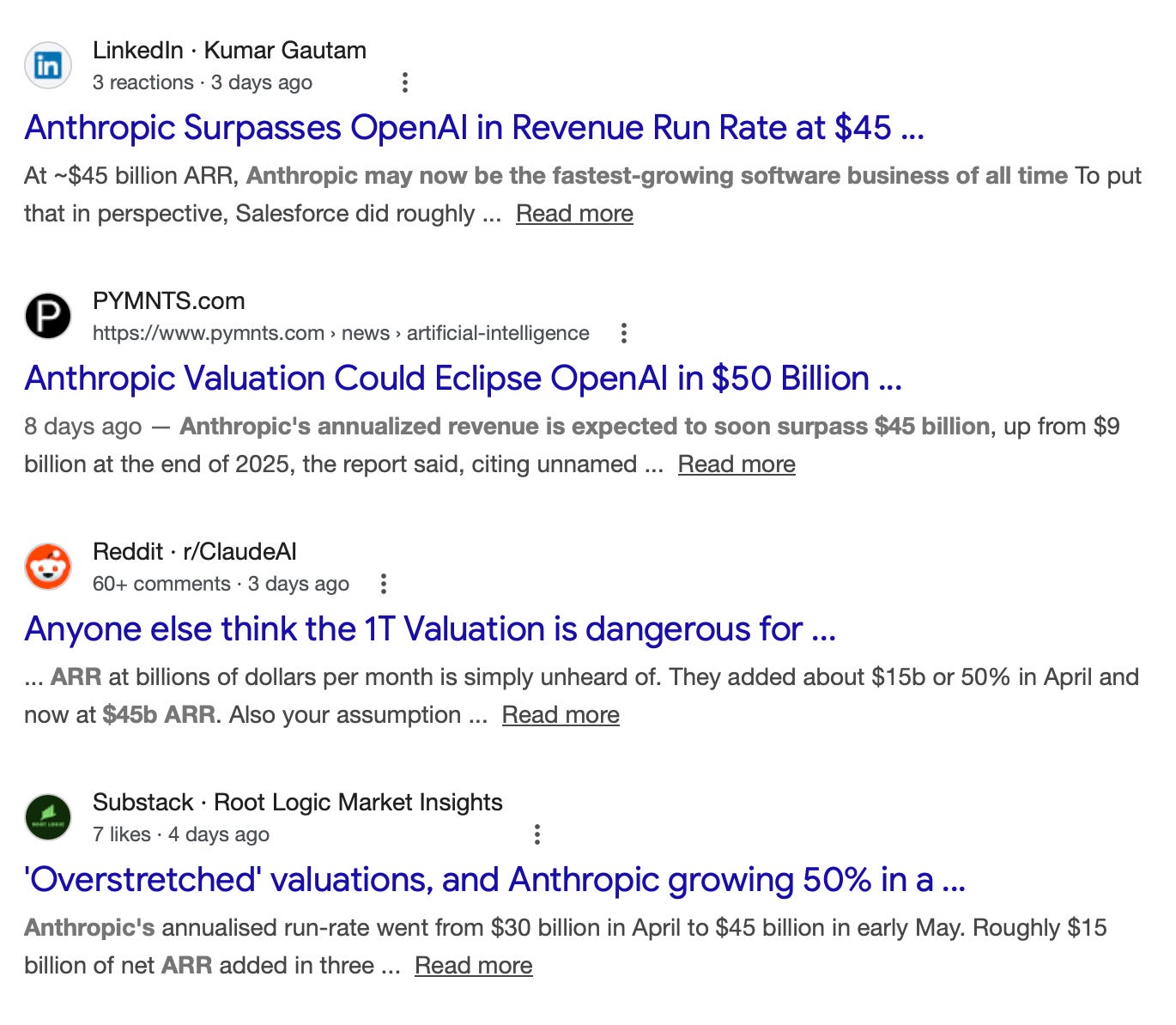

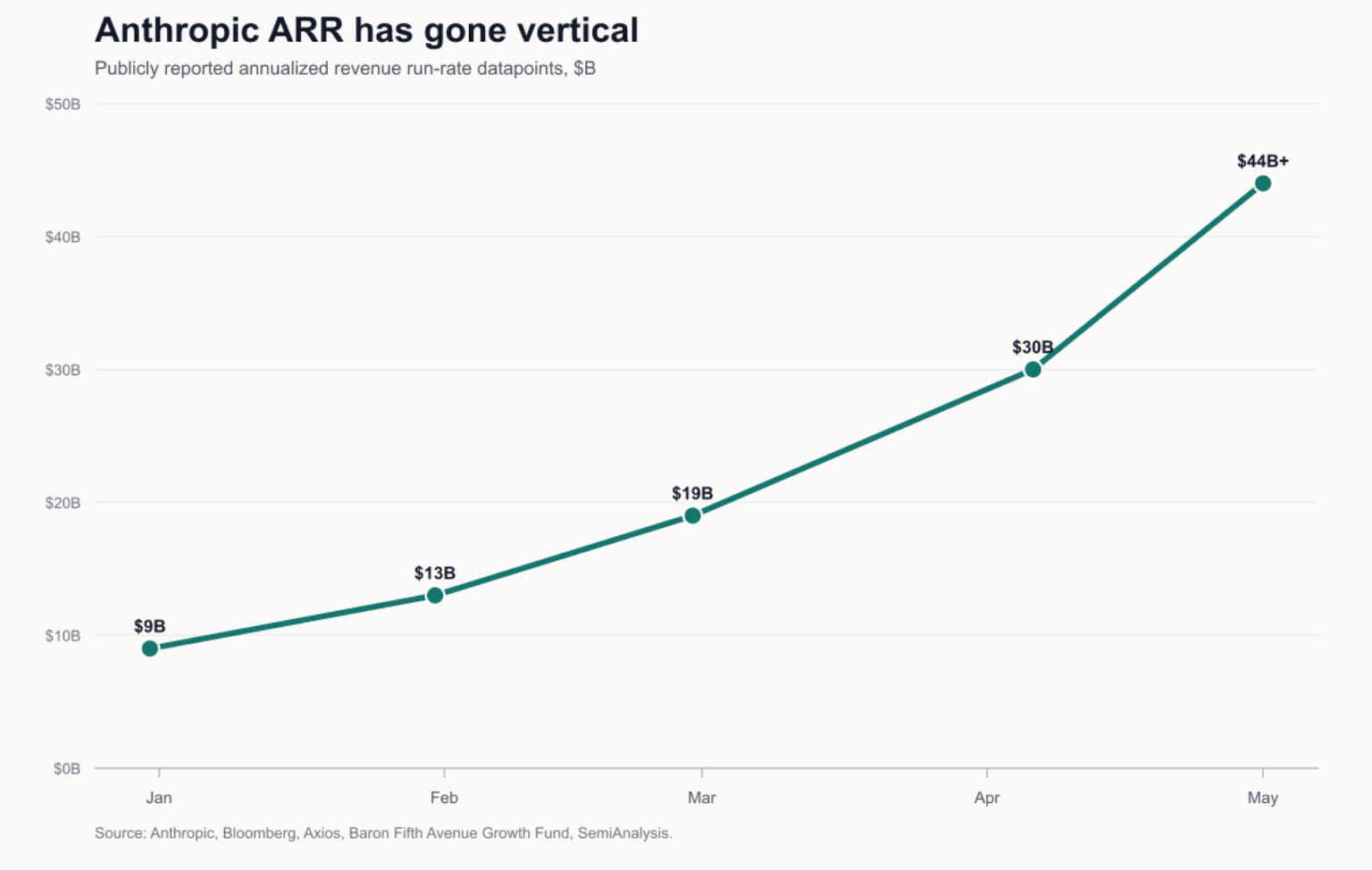

Currently as of May 2026, Anthropic is at around a $45 billion ARR according to sources and stuff.

They are undergoing another round of private fundraising. At their proposed new valuation of 900 billion, they would trade at 20x current ARR. This seems expensive to the general public who may view this as a hallmark of the “AI bubble.” So let’s put it into perspective.

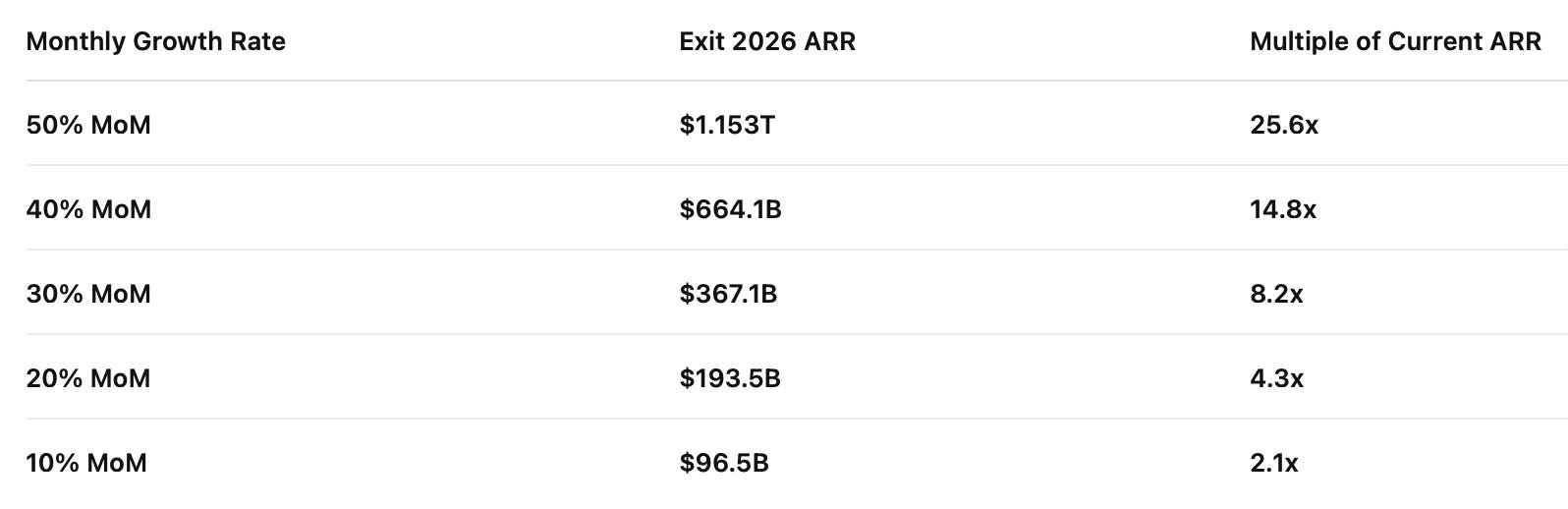

They started the year at a $9 billion ARR. That is an annualized growth rate of (lol) 12,400% or a (very convenient) month-over-month growth rate of 50%.

Anthropic mentions their current ARR from time to time, and we can map out each of their public data points to approximate the month-over-month growth. The implied monthly growth intervals are roughly 43%, 51%, 46%, and 59%. So, it fluctuates around 50%, but doesn’t seem to be slowing down.

Let’s build a quick sensitivity table for what their ARR would be if they kept this growth rate or it slightly slowed down.

As you can see, if they kept up 50%, they would have a trillion dollars in revenue. I mean, that’s not even impossible. The data doesn’t show it slowing down and the singularity could be here anytime.

But for realistic purposes, I would assume that it slows down just based on first principles and the laws of gravity. We’re going to use something between a 20% and a 30% month-over-month growth rate for the rest of the year as our baseline assumption, which will put them at $300 billion in exit ARR. At a $1 trillion valuation, that’s only 3.3x exit 2026 ARR.

Wow, that valuation changed quickly, didn’t it?

Public Markets and Forward Numbers

Oh, another thing that we almost forgot about. Remember when I was talking about how we public investors just forget everything that we’ve learned when we go and visit the private side? Well, one of those things is the fact that we all happen to use 2027 and 2028 multiples on all of our semi stocks. When was the last time you valued a company like Lumentum on what they would earn in 2026?

So why is Anthropic any different?

This happens for a very simple reason: there is no analyst coverage on private companies.

Without “consensus” numbers to go off of, trailing metrics are the markets’ only indicator, which are, by and large, completely irrelevant. There is zero signal whatsoever in what Anthropic or OpenAI earned in 2025, just like there is zero signal in what Lumentum or Bloom Energy or AXTI earned in 2025. Yet it is the only thing visible to the public, so it is the only thing that investors anchor to.

If we apply the public markets’ approach, even partially, and use exit CY26 ARR, we already arrive at the conclusion that a one trillion valuation is absurdly cheap, as it is only a single-digit multiple, but we don’t have to stop there. Arguably, we should look out even farther for these AI labs, as they are the definition of low revenue today but high terminal value. What about exit CY27 ARR or even exit CY28 ARR? I’ve seen sell-side broker notes valuing Palantir and Snowflake on what they would earn in 2035. Shouldn’t Anthropic get that same treatment?

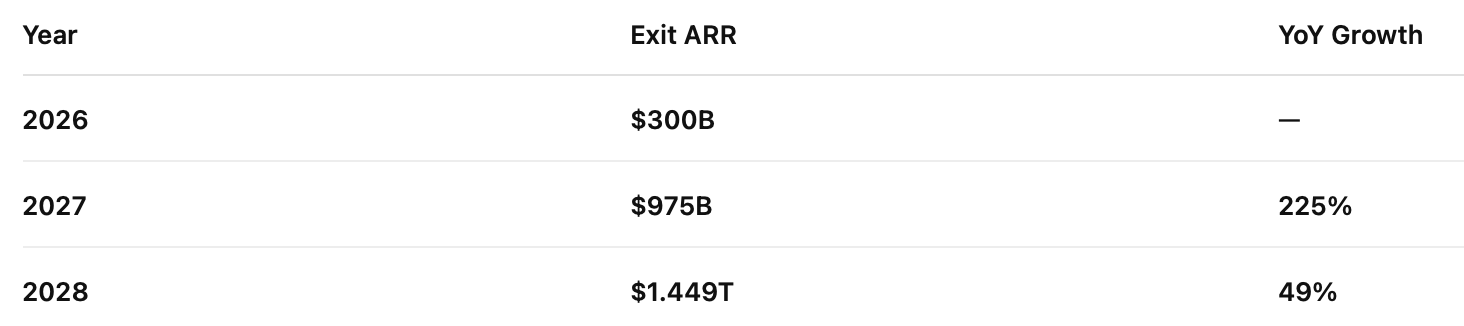

I say exit CY28 ARR is a happy medium. Let’s run a sensitivity on what that number could be.

Estimating CY27 and CY28 ARR

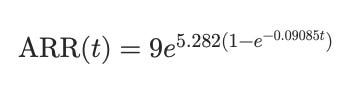

Let’s model Anthropic’s revenue as a power law. Given three data points:

$9 billion starting ARR

$45 billion ARR at the start of May

$300 billion ARR at the end of 2026

we can fit this to a Gompertz-style curve where the growth rate decays exponentially over time.

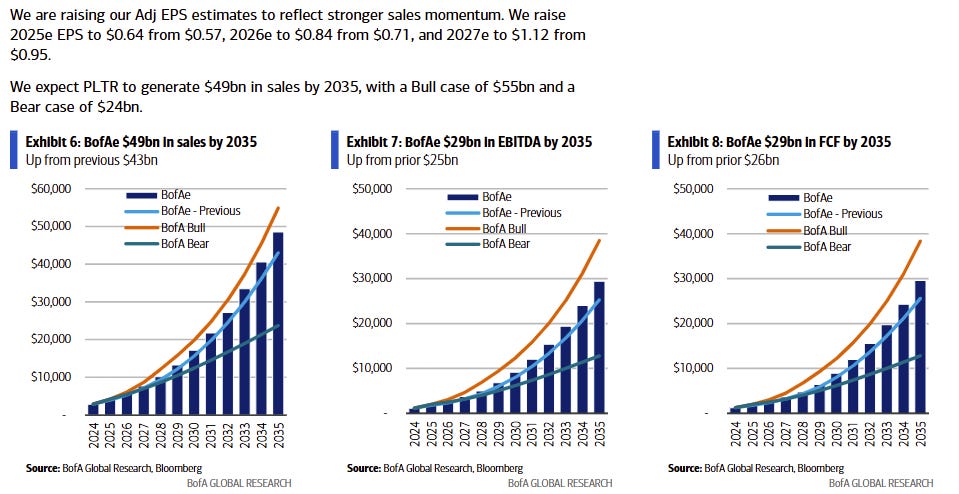

Using this Wacky Ahh Equation, we can get to approximately almost exactly one trillion dollars of exit CY27 ARR.

I love it when our numbers are convenient. This is also almost exactly a tripling in revenue.

What about 2028?

And our final result is $1.5 trillion of ARR exiting 2028. Almost exactly 50% growth.

Margins

Now let’s discuss Anthropic margins.

Anthropic’s 2025 gross margin is commonly cited at 40%. Which leads many people to believe that frontier tokens are a relatively low-value-add product, and that every $1 of incremental token revenue generates only $0.40 of gross profit dollars. This is technically incorrect and very misleading to what the actual unit economics of their business is.

I would like to introduce you to a concept known as contribution margin. Cost of goods sold is generally seen as the variable costs. However, COGS actually often has fixed components. It is simply an accounting bucket meant to provide a reasonable standard for GAAP and not to be economically accurate to the actual variable cost of a business.

For Anthropic, the economically fixed portion of the cost of goods sold is essentially any unused capacity plus freebies given to users:

reserved AWS/GCP/Azure/TPU/GPU capacity paid for whether fully used or not

idle capacity, redundancy, peak-load headroom, and latency headroom

low batching / lower utilization for fast interactive workloads

subscription overuse and free-tier usage

production infra staff, SRE, safety/moderation, routing, storage, networking

The economically correct metric is called the contribution margin. This is the very intuitive revenue minus variable costs, what a company earns for every unit of a product it sells. This is how we should evaluate token economics. According to SemiAnalysis, this is now above 70%, so I believe 75% is a fair base case for a contribution margin assumption today, expanding to 80% over the next two years.

Cost of production for token has fallen sharply because increases in accelerator pricing generation-over-generation have been more than offset by much higher throughput (tokens/sec/gpu). Average blended price per million tokens has fallen dramatically over the past few months, agentic workloads are inherently multi-turn with longer input/output ratios and higher cache hit rates, but inference margins have gone up from < 40% to > 70% in the same time frame.

- SemiAnalysis

Currently, Anthropic is GAAP unprofitable, with the model lab’s enormous cash burn being cited as a lack of favorable unit economics. However, the cash burn is actually caused by the training compute spend, aka the “R&D” of the leading labs. R&D in GAAP is expensed in the period incurred. However, economically speaking, it should really be treated more like capex, as it is an investment in a future model which pays back over many years. In R&D-heavy industries, GAAP net income can be extremely misleading as it does not account for the economics of this investment.

This is why I believe Net Income or EPS is not the right denominator on which to value the Model Labs. Instead, we should look at their contribution margin, and basically say how much is the business worth if they stopped investing today and served the models they already had?

80% of a $1.5T exit CY28 ARR is $1.2T in contribution margin income.

Valuation

What would you pay for the best business of all time? Assuming Anthropic has achieved recursive self-improvement and stays #1 (i.e. infinite moat), this is actually an accurate descriptor.

Let’s look at what people already pay today for the highest quality highest growth recurring revenue businesses: Palantir and Cloudflare.

Palantir is currently being valued at 45x 2028 earnings.

Cloudflare is valued at 90x 2028 earnings.

Now, a high double-digit out-year earnings multiple might seem extreme to most of us, but there’s actually a reason these top-quality software companies are so expensive. If you have confidence in a decade or longer runway of highly above-average growth and you run it through a DCF, you end up with incredible numbers. 30x is just not enough to reflect that. The combination of high growth, high duration, and high certainty is that rare.

Because of what I said in our above section, I believe it’s very easily arguable that Anthropic is far above the quality of these software companies. However, let’s say we just apply a multiple on the upper range of the 45x to 90x bound: 83x.

$1.2T Contribution Margin Profit * 83x multiple = $100T Valuation

Anthropic is worth one hundred trillion dollars!

The Singularity

This is the singularity.

The concept is simple. Once recursive self-improvement produces the first superintelligence, the equivalent of a near-infinite superhuman labor force enters the economy. Productivity, which is quite literally the production of goods and services, now goes through the roof because we have a country of geniuses in a data center.

An important fact people forget is that GDP growth is not set in stone. The Industrial Revolution, which added capital productivity growth to a pure labor economy, increased GDP growth from mere basis points (the growth rate of the population) to a surprisingly stable 2-3% per year.

Now, as superintelligent AI introduces the automation and growth in productivity of cognitive labor itself. I expect another step function change in GDP growth, perhaps to 5%, 10%, or even higher. As famously stated by Irving John Goode in 1965: “Thus the first ultraintelligent machine is the last invention that man need ever make.”

This is not a concept that us investors talk a lot about, but many of us privately believe in (me lmao). I don’t think this should be the case. If it is a real possibility, we should give it real consideration in investment analysis.

AI 2027 describes the post-singularity economy with the most vividness and detail of any essay about the singularity that I found, featuring special economic zones (SEZs), robots, factories, drones, and fusion.

“By the end of the year they are producing a million new robots per month. If the SEZ economy were truly autonomous, it would have a doubling time of about a year; since it can trade with the existing human economy, its doubling time is even shorter.”

“By late 2029, existing SEZs have grown overcrowded with robots and factories, so more zones are created all around the world (early investors are now trillionaires, so this is not a hard sell). Armies of drones pour out of the SEZs, accelerating manufacturing on the critical path to space exploration.”

“Robots become commonplace. But also fusion power, quantum computers, and cures for many diseases. Peter Thiel finally gets his flying car. Cities become clean and safe. Even in developing countries, poverty becomes a thing of the past, thanks to UBI and foreign aid.”

- AI 2027

What are the implications for Anthropic’s valuation?

If AI accelerates global GDP growth to 10%, that is quite literally a tenth of the global production in goods and services being added every single year by AI itself.

That is a lot of value. An unimaginable amount!

All of it is enabled by the frontier models and the labs behind them. If you are the leading monopoly AI lab, which is performing this economic acceleration, which is bringing about a robot economy and curing diseases, how much should you be worth?

I do not have 100% conviction that Anthropic will be worth $100 trillion. I don’t have conviction that any company will be worth $100 trillion. But I do have 100% unwavering confidence that the combined value of the one or multiple leading AI labs, whether it’s Anthropic, OpenAI, Google, all three, or another company we haven’t even heard of, will be worth that much once the singularity arrives.

The IPO

We spent the first half of the article discussing the why behind Anthropic and the Model Labs theoretical valuation ceiling. Now let’s move on to the how. These companies are private. What can we do to get exposure?

Cerebras taught all retail AI investors a nasty lesson. The system is not built to help us.

Cerebras began at close to $100 a share, but due to popular demand that outstripped available supply by 20x, they increased their IPO pricing to $135, then $150, then $185.

But it gets a lot worse because the IPO price isn’t the price that you can buy on your brokerage on the day the ticker starts trading when the shares actually go public. A market is made, so the actual price it starts trading at is whatever the first buyers and the first sellers agree on in the order book.

And for hot IPOs like Cerebras and definitely Anthropic or OpenAI, there is going to be a ton of buyers at the same time. Nobody’s going to want to sell. This means that the shares could open at high double-digit or triple-digit above what the IPO price initially was, as buyers relentlessly pour in.

Cerebras, after being priced at $185 for the IPO, opened at $380. Imagine being a retail investor here. You heard that you can buy Cerebras for a $25 billion valuation, maybe did your homework, realized it was a good deal, and got excited. When actually pulling up the stock to trade it on Robinhood or something, it is four times more expensive than what you expected.

I think this is almost guaranteed to happen with Anthropic and OpenAI. From here, I don’t see a path to a $2 trillion private valuation before the end of the year as unlikely. From there, the IPO price is probably slightly higher than that, and the initial trading price might already make them one of the most valuable companies in the world, on par with the Mag 7.

How Retail Investors Can Play This

Next, I will share a trade which allowed me to get dollar-for-dollar exposure to Anthropic with the least catches out of any single backdoor Anthropic play that I’ve looked at.

There are holdcos where you get a tiny fraction of the per-share value as Anthropic and there are closed-ended funds that trade at hundreds of percent of NAV. The problem with these plays is that they are incredibly capital inefficient. You can’t get exposure without fronting a significant portion of your portfolio or even taking on leverage just to have a sizable economic exposure to Anthropic. This is substantially worse than owning Anthropic stock purely, because you either have a fraction of the exposure or you must lever up significantly in which case you are completely path dependent on the share price not going down 40%.

There are perps exchanges that charge you hundreds of percent in funding rate to go long (cough cough hyperliquid). Essentially, these perps exchange funding rates act as an incentive mechanism to discourage longs and encourage shorts, to keep the price of the futures contract tethered to the oracle price. Basically, what this means is that at the current oracle price, which is the private value Anthropic mark, there are vastly, vastly more longs than shorts. Even with a conventionally extreme incentive to short, longs still vastly outnumber shorts. This is just a convoluted way of saying the price is way too low.

However, with a little bit of financial engineering, I came up with a creative way to get 1x exposure to Anthropic without these problems. No, it is not buying Anthropic on the private markets and actually owning the shares yourself, but it works reasonably well enough, and I’ve put a sizable portion (5-10%) of my portfolio into this.

Below, we will analyze the company that is the subject of this trade and do some serious quantitative analysis on the trade’s mechanics and potential payoff.