The Soitec Series | Part 1: Introduction to the French Photonics Substrate Monopoly

7 articles about a potential 7-bagger. This is my career-defining bet.

Opinions are my own and do not represent past, present, and/or future employers. All content is based on public information and independent research. This newsletter is not financial advice, and readers should always do their own research before investing in any security. I am invested in the semiconductor industry. As of the date of this publication, I hold a long position in Soitec.

They are French.

They are down bad.

And they have a near monopoly on the raw material needed for silicon photonics.

Outline

What is Soitec?

Business Model

Business Segments

They Got Fucked by Mobile

The Photonics Opportunity

Manufacturing Economics

Management Sandbag

Conclusion and Up Next

What is Soitec?

Business Model

Think about the regular starting wafers used by TSMC.

These need to be made, they don’t just magically get conjured from thin air. Shin-Etsu is the most common company people think of that conducts the making.

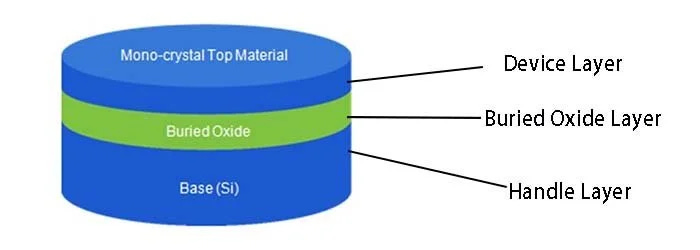

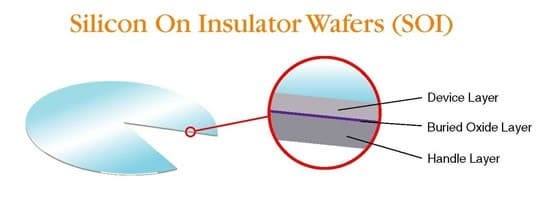

Soitec is a specialty materials company that designs and manufactures engineered semiconductor wafers. These wafers are called “silicon-on-insulator” (SOI) because it’s like a silicon sandwich with a middle oxide layer. They are needed for special types of chips, most notably mobile and silicon photonics. Foundries buy from them.

In normal semis, the starting wafer is commodity. In specialty processes, it is not. The wafer stack itself can determine RF behavior, leakage, thermal performance, switching efficiency, optical confinement, and ultimately whether a process is competitive at all. Soitec’s job is to build those starting substrates with the right layers, thicknesses, bonding, and uniformity. Not easy!

Business Segments

A huge portion of the company’s revenue is mobile, which is in a cyclical trough. Besides that, they have a bunch of industrial and IoT junk.

They report in 3 segments: Mobile, Auto & Industrial, and Edge & Cloud AI. This is a really bad way to report things because the photonics segment is buried inside of “Edge & Cloud AI” along with some IoT junk. They should instead report based on product lines. However, this is actually very good because it’s hard for the market to correctly price SiPho revenue and many investors would just quit because of low visibility, when in reality it’s not that hard to get the estimate by digging through management’s commentary.

Product lines

RF-SOI, historically the core franchise, used in smartphone RF front-end chips

FD-SOI, used in low-power logic and mixed-signal designs

Power-SOI, used in power electronics

Photonics-SOI, used in silicon photonics

POI, or piezoelectric-on-insulator, for RF filters

SmartSiC and other advanced substrate adjacencies

In terms of mix, this FY (ending March 2026) they are likely to do around EUR 500-600m total revenue, split into EUR 300m in mobile and EUR 100m in pure photonics, the rest being IoT and Industrial.

They Got Fucked by Mobile

Really hard.

It’s the reason they look optically cheap today. Let’s get into what happened.

For years, Soitec’s center of gravity was RF-SOI, the engineered substrate used in radio frequency front-end chips for smartphones. This was the big cash cow. As 4G and then 5G handsets added more frequency bands, more filtering, more switching, and more RF complexity, RF-SOI became a critical substrate for parts of the mobile front end. Soitec rode that wave hard. It became the foundational materials supplier to one of the most economically attractive niches in mobile semis.

But then memory happened. Phones aren’t selling as well, so customers built up millions of wafers in excess inventory. Their channels got stuffed. If you are a supplier and the companies that buy from you are overflowing with excess inventory, don’t expect orders anytime soon. In the latest quarter, Soitec reported Q1 FY2026 revenue of just EUR 92m, down 16% year on year organically.

Therefore, catastrophic stock collapse! At a stock price of €41, the company trades at around 2x EV/revenue and 7-9x forward EV/EBITDA on estimates in the next year or two.

There’s also a recovery plan in place.

In the February 2026 earnings call, Soitec said customer RF-SOI inventories had fallen from 2.5m wafers in September to 2.0m wafers by December, and that the company was continuing to under-ship demand by roughly 200-300k wafers per quarter with the goal of getting customer inventories closer to 1.0m wafers by the end of calendar 2026. In other words, a large part of the current revenue weakness is self-inflicted in the sense that Soitec is deliberately shipping below end demand to clear the channel.

Normalized mobile revenue should be anywhere from EUR 500-700m. Any sort of recovery in mobile I consider to be downside protection and uncorrelated return, making this much easier to underwrite.

The Photonics Opportunity

They have a very high market share in SOI wafers for photonics. Their two main competitors are GlobalWafers and Shin-Etsu.

In SOI wafers more generally, they are the inventors of the Smart Cut technology. Smart Cut is the process architecture that allows a thin top silicon layer to be transferred onto an insulating oxide over a handle wafer.

Smart Cut is the Moat.

Interestingly, Soitec licenses Smart Cut to competitors to earn royalties. Around 80% of the SOI market uses Smart Cut.

Why do they do this? Imagine you’re a foundry.

You hate single source risk. You learned this in Foundry 101. So if there’s an upstream monopoly, you fund competitors to break it.

Soitec likely played 4d chess. By licensing, they can say “hey, look there are other SOI suppliers!” while still maintaining vice grip over the market.

Additionally, for photonics, Soitec is the only player with material revenue.

Photonics-SOI is much harder than regular SOI. Photonics-SOI needs much tighter control of the top silicon thickness, surface quality, defectivity, and wafer uniformity because small deviations directly affect how light propagates through waveguides and modulators. Regular SOI for electronic devices is demanding too, but photonics is more sensitive to optical loss, mode confinement, and coupling efficiency, so the substrate specs are harder. In practice, that means fewer suppliers can make it at production quality and scale.

Shin-Etsu’s earnings call has zero mention of photonics, and GlobalWafers is only in sampling/validation. Soitec is doing EUR 100m in revenue.

Manufacturing Economics

One of the more interesting things about Soitec right now is that the current trough may actually help the photonics setup.

Capacity is partly fungible. JPMorgan:

But “fungible” should not be overstated. These are not generic wafer lines where any spare slot can instantly become a photonics wafer. Qualifications, recipes, and customer approvals still matter. So the right mental model is partial fungibility: the physical asset base can be shifted across product families to an extent, but not frictionlessly and not without product-specific enabling work.

Manufacturing is a fixed cost business. Low utilization is like flying with empty seats. You lose a shit ton of money.

Soitec has been very clear that the RF-SOI downcycle is depressing factory loading and therefore crushing margins. Barclays summarized the issue well in February: fab loading remains the most important margin driver, and lower utilization continues to compress margins. The company itself has said lower sales have led to lower utilization of industrial capacity.

That is bad for current earnings, but good for the photonics torque.

If Photonics-SOI ramps into underutilized lines, the incremental margins can be much better than the current depressed corporate average. The Contribution Margin of each additional wafer is very high (added benefit that Photonics-SOI is very difficult to make and naturally commands higher margin) meaning the higher the utilization, the higher the Gross Margin.

In addition, this means the company does not need a bunch of capex. Some of the upside can simply come from filling already-built capacity more effectively.

So basically, massive gross margin expansion coming.

Management Sandbag

To add on another reason for the market not seeing the opportunity, I believe management is sandbagging.

Management guide for photonics is 20-30% per year. If you know anything about the current photonics landscape you’d probably be questioning why this is so low. Every other optics company is far above this so on the surface this seems like execution issues or structurally bad economics.

However, we can deductively prove that neither is the case and Soitec’s growth will be faster.

Tower Semiconductor, their biggest SiPho foundry customer, announced investments of over $900m to 5x capacity from YE 2025 to YE 2026, resulting in a 200% growth in 2026 and 100% growth in 2027 (my own above-street assumptions). Revenue growth comes from ASP and volume. For Soitec, the only volume producer of Photonics-SOI, any of Tower’s growth that comes from volume maps directly to more wafer orders.

As a foundry is increasing their capacity by 5x, do you think its revenue growth comes from volume or 500% price hikes?

I think the likely explanation is that Soitec management is trying to rebuild credibility in the middle of a cyclical downturn. In that context, it makes sense to guide only what they are highly confident they can deliver rather than lean into a more aggressive photonics narrative.

It is hard to believe that Soitec, as the leading Photonics-SOI supplier at scale, will undergrow that ecosystem by an enormous amount. There can be some slippage. Foundries capture more process value per wafer. Wafer efficiency improves over time. Content can shift modestly. But those are reasons for Soitec to grow somewhat slower than the foundries, not for it to miss the ramp entirely.

This is another reason the stock can be mispriced. The market is anchoring on a company-level conservative guidance while the underlying photonics demand signals are coming from elsewhere in the value chain. If those demand signals are right, then Soitec’s reported story should eventually have to catch up.

Conclusion and Up Next

It is in the upcoming parts where I will dive deep into the photonics market and create a bottoms-up build of estimates.

For a preview, management confirmed photonics revenues will be €100m in the fiscal year ending March 2026. In just 2 years as 1.6T and CPO ramps, I project this number surpassing €400m, with high contribution margins as no extra fab builds are needed thanks to fungible capacity. At a €1.6b EV, Soitec’s current valuation is very attractive.

Now excuse me as I go enjoy my Soy Wafers.

Excellent ! French here, and was getting mad that nobody was mentioning this company when talking about photonics. In line with your thesis I am also heavily invested in. Key player under radar (for now). But will also need its two other products family (mobile and automotive) get back to growth in order to rise to its ATH in the 2-3 years coming.

Excellent article. Wrote a very small chapter about SOITEC in my Globalfoundries Deep Dive, but didn't dig any deeper since then. Are you going to cover that relationship in your series?

https://manuelwalz.substack.com/p/globalfoundries-nasdaqgfs-the-sovereign