Onto Innovation | Earnings Review: High Bandwidth Mogging

Jestermaxxed in CoWoS but HBMogged Camtek at Micron

Opinions are my own and do not represent past, present, and/or future employers. All content is based on public information and independent research. This newsletter is not financial advice, and readers should always do their own research before investing in any security. I am invested in the semiconductor industry. As of the date of this publication, I may hold long or short positions in securities discussed in this article.

Pre-Earnings Vibe Check

(This section was written prior to the earnings call to communicate the prevailing narratives and provide a contrast to post-earnings sentiment)

I’ll keep this section short for today because the thesis I published yesterday says most of what’s necessary already. Required reading before you continue!

The Onto Series | Part 1: The Ultimate Advanced Packaging Comeback

Opinions are my own and do not represent past, present, and/or future employers. All content is based on public information and independent research. This newsletter is not financial advice, and readers should always do their own research before investing in any security. I am invested in the semiconductor industry. As of the date of this publication, I…

Onto trades at $220, up 30-ish percent YTD, driven mostly by very very robust strength in the semicap factor. This is all beta no alpha IMO, so the idiosyncratic situation hasn’t changed much.

Consensus Expectations

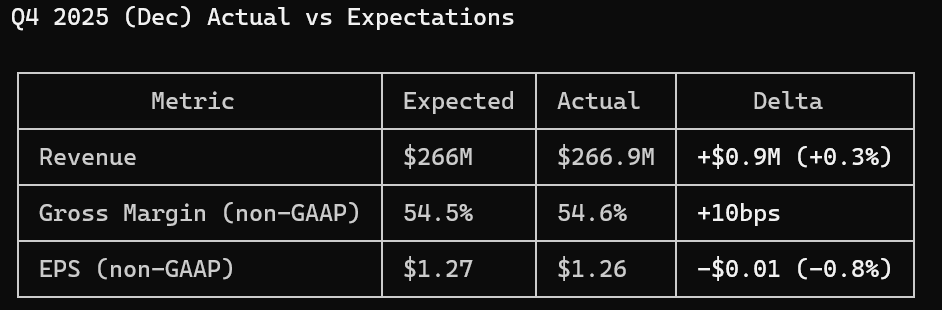

Expectations for Q4 2025 revenue is $266mm, gross margin 54.5%, EPS $1.27.

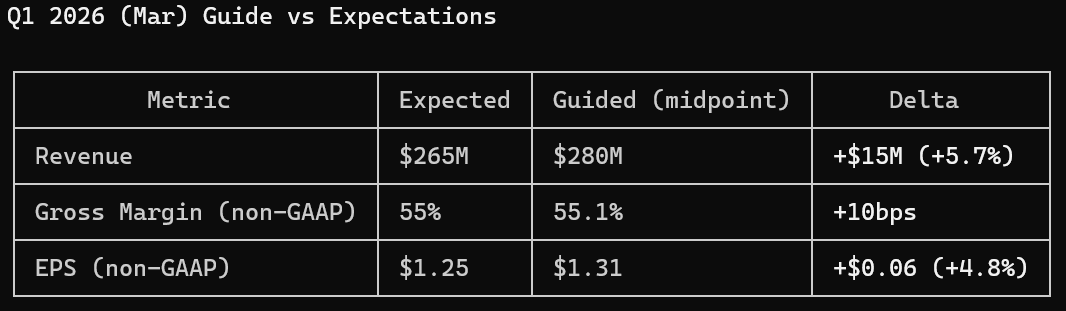

Expectations for Q1 2026 revenue is $265mm, gross margin 55%, EPS $1.25.

In addition, they revised their 1H26 over 2H25 growth from 5% to “at least 10%” at a recent conference. They reiterated expectations of 20% advanced packaging growth.

Therefore, they probably need a moderate beat on these to stay flat. Big beat is big upside because something unpredictable happened, in-line will be downside. Camtek only beat slightly (1-3%) and was down to flat today.

CoWoS Share Recapture at TSMC

The most important indicator today is commentary around TSMC qualification. Based on recent sellside reports, they seem to be “far along” and could be within 3-6 months. They have passed “optical validation” which is NOT qualification but is a very good sign.

After that, Onto has specifically stated aspirations to regain 50% of lost share in 2026, which was also my assumption in my writeup. Watch for if that changes.

Share Gains at Micron

Onto has fully qualified for Micron. They are in and orders are flowing. The only question is how much.

There is some interesting Camtek commentary I wanted to address. They have flatly denied any share loss.

“We have not lost any market share to competitors. We also estimate that we will be able to increase our market share this year.”

Called HBM4 a “major opportunity” — claims their Hawk platform handles the higher density/accuracy requirements

Got a $45M order from an “IDM customer” expanding capacity for AI components — sounds like a memory maker

Says they’ll penetrate “additional production steps and expand our total available market”

However, there was also zero mention of the infrared integration problem.

I doubt this means that they would never lose share. It is expected that the incumbent would not admit to share loss. If Onto’s management specifically calls out infrared integration as an important competitive advantage and backs it up with tens of millions in new orders, Camtek’s defense is disproven.

Share Gains for Front-End Metrology (OCD and Thin Film)

This is the only theme I did not mention in my writeup. Onto also plays in front-end metrology and that segment is deserving of its own article (which will be Onto part 2).

Onto has two front-end metrology tools: OCD and thin-film. Right now, Onto and KLA sort of split front-end metrology 50/50. Onto has more share in OCD while KLA has more share in thin-film.

Any upside bias to this split means Onto go up, downside means Onto go down.

WFE Demand Upside

For advanced packaging, last quarter, customer conversations suggested the need for as much as 20% more tools in CY26 (according to Oppenheimer) which also matches what Onto themselves stated at their recent conference. My assumption for packaging growth this year is 25%.

Upside here comes from CoWoS expansion, HBM demand, and Intel’s EMIB.

In the front-end, all that matters is TSMC’s expansion of the N2 node. I don’t think we are yet at the point where Intel 18A-P and 14A can be considered upside, but any long-term commentary there can also be a source of strength.

The leading edge is in a massive shortage so let’s see if that shows up today.

The Print

Behold my Claude Code terminal tables once again

Q4 2025 was in-line. A bit disappointing, definitely some softness. We’ll see how they explain this on the call.

Moderate beat, above consensus, probably missed buyside bogeys slightly, enough to keep the stock flat I think.

However, the actual numbers aren’t what validates or disproves the thesis. Almost all the information should be related to commentary.

From the PR, we already get the following.

“Next generation Dragonfly shipped to multiple customers with evaluation periods now ongoing.”

That’s Dragonfly 5. Nothing new here. Looks like no major qualification news for TSMC before the call starts.

Hold on. Hold on. WOAH

“$240M+ volume purchase agreement with a leading HBM manufacturer for Dragonfly 2D inspection and 3D bump metrology through 2027.”

That’s almost certainly Micron. $240M through 2027 is VERY BIG. I assumed $30M in 2026, seems like I undershot by a lot. Let’s see how much of this ships in 2026.

Soft numbers + no TSMC news + BIG HBM order. Interesting…………

Excited for the call.

Price Action

flat ahh price action. nothing to write home about here.