The Second Singularity | A General Theory on Humanoid Robotics (Free)

Robotics is AI in 2022 and is barreling towards its own ChatGPT moment, Claude Code moment, and RSI.

There’s a beautiful, obvious, and elegant way of thinking about the upcoming robotics revolution that I haven’t seen communicated anywhere yet.

Robotics = AI.

Just 4 years earlier in development and physical rather than digital.

Every concept in robotics has a parallel in AI, and these parallels are accurate, structural, and one-to-one to the point where it’s truly uncanny. Both are general purpose automation technologies, and in the universe, these are the only two in existence because there are only two types of activities to automate: digital and physical. This entire article will be mapping every concept in robotics to its AI counterpart, and you will see how much easier it makes intuitively understanding this technology and its future market potential.

Introduction

Why should two such different technologies rhyme this precisely? Because they both fully generalize to a human capability set, and in doing so replaces human labor rather than merely augmenting it.

In 1965 the mathematician I.J. Good wrote that “the first ultraintelligent machine is the last invention that man need ever make,” because a machine that can design machines will design its successors and leave human intelligence behind. Almost everyone who quotes this assumes there is one last invention, and that it is AI.

There are, in fact, two last inventions, because thinking and doing are separable, and AI only does the thinking. It doesn’t matter how many geniuses you can cram into a data center. They literally cannot move a paperclip. You could say, “Oh, they must be smart enough to design a humanoid robot to do it for them so humanoids are just a byproduct of AGI.”

However, let me ask you this: How would an AGI manufacture that humanoid robot? Does it have supply chain relationships? Can it build factories? Can it pour concrete? Yeah, that’s what I thought.

The second last invention is the general-purpose humanoid robot. Artificial General Robotics. Instead of an AGI, it is AGR. Together, and only together, the two cover the whole of human labor.

Most general-purpose technologies (electricity, the smartphone) augment. These two replace, and replacement is what creates a singularity. Technologies of that kind (of which there are only two) obey the same patterns: the same stages of autonomy, S- or L-curve, economic singularity, RSI, Moravec’s Paradox, and even very suspiciously similar big three labs.

The Second Singularity is coming — the physical singularity.

Welcome to A General Theory on Humanoid Robotics.

Contents

The Four Stages of Robotics

The Four Stages of AI

The Big Three Labs

The Elbow of The L-Curve

Moravec’s Paradox

VLAs vs. World Models

The Economic Singularity

Robotic Self-Improvement (RSI)

Conclusion: Predicting ChatGPT and Claude Code Moments

Beep beep boop boop beep boop beep boop terms and conditions. Beep boop not financial advice.

The Four Stages of Robotics

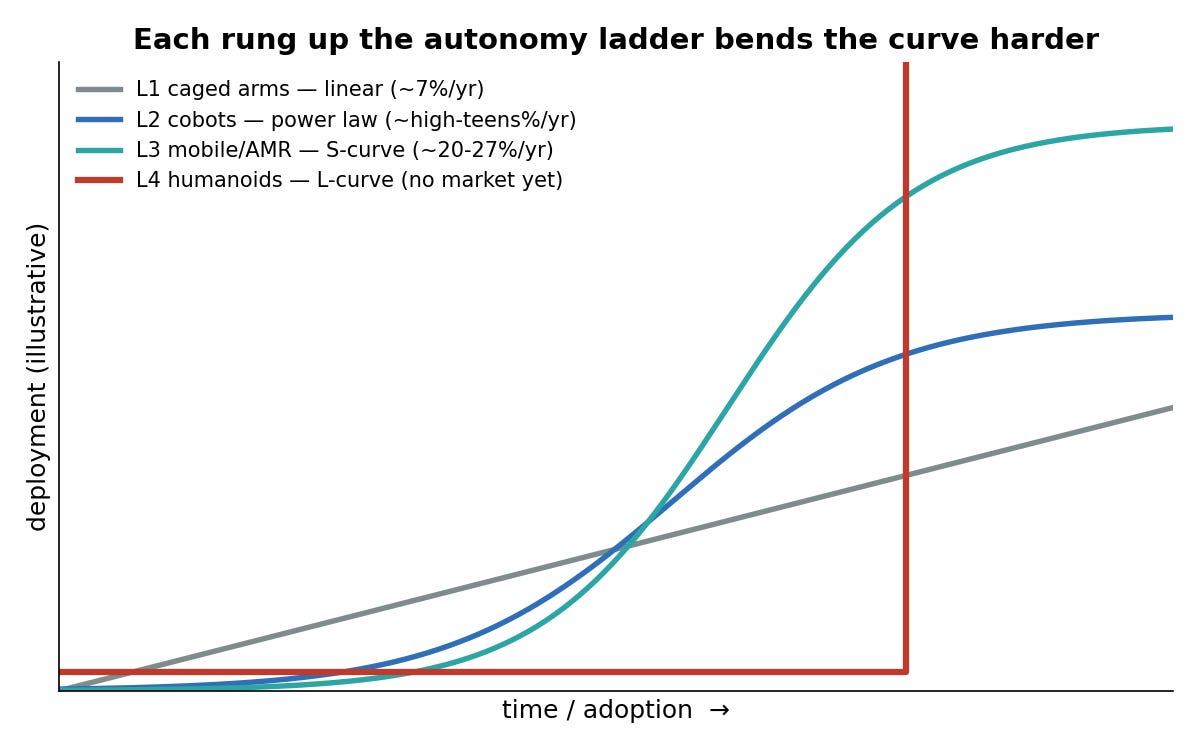

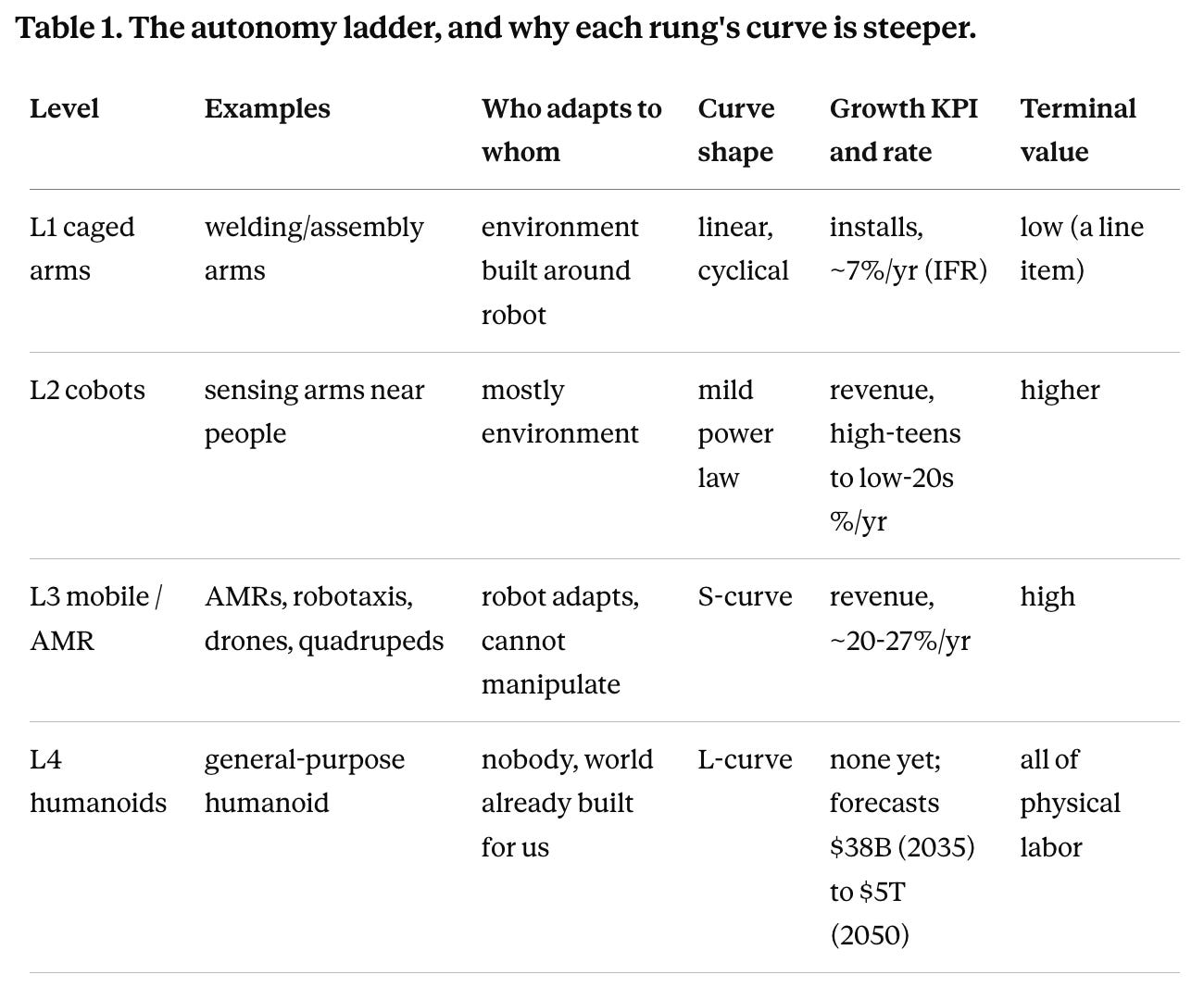

Robotics comes in four stages, each one more general than the last.

Caged Arms

Cobots (Collaborative Robots)

Autonomous Mobile Robots

Humanoid Robots

Each stage is its own market. And the difference between the markets is as follows: The more general the robot, the less of the world you have to redesign to use it, and the more exponentially it spreads.

Why do more autonomous and general robots grow exponentially? It is simple. Either the environment is rebuilt around the robot, or the robot adapts to the environment. The environment is expensive and glacial to change. Thus, the robot, as it generalizes, gets cheap and fast to deploy into environments it’s never seen before, unlocking use cases with orders of magnitude higher addressable markets, until it saturates all of physical labor.

Yes I know that is a funny looking curve. I’m being serious. When I say L-curve I really mean it.

Now let’s discuss each stage of robotics one by one.

Level 1 - Caged Industrial Arms

The arms that weld cars. They are blind, dumb, and pre-programmed, fenced off from people because they cannot perceive a human walking into the cell. The entire factory is designed around them, so every incremental robot requires designing and building another bespoke environment. That is the most expensive, least flexible form of adoption possible, which is exactly why the curve is linear and the terminal value low. The installed base is tiny despite the technology being decades old.

If you look in the market, it is clear that caged arms are not a frontier technology at all. Instead, it is an industrial appliance and grows perfectly in line with industrials. The International Federation of Robotics counts on the order of half a million new installations a year, and forecasts global installations to grow only about 7% a year through 2028, with the market value (roughly $45 billion in 2024) compounding at low double digits at best. Growth tracks manufacturing and auto capex so tightly that 2024 installations actually fell in Japan and Korea.

Conclusion: These robots are equipment and not technology.

Level 2 - Collaborative Robots (Cobots)

Cobots can sense enough to share a floor with people. The environment still bends around it, just less. Because each deployment now costs less environment, the curve steepens into a mild power law and the terminal value rises, even though the hardware is weaker than a caged arm. The inflection is arriving now.

Cobots serve the same end market but grow slightly faster due to its higher generality, resulting in a larger addressable pool of use cases within industrials. It is less mature, so it starts off a smaller base (on the order of $1 to 2 billion in 2024) and compounds at high-teens to low-twenties percent a year, several times faster than caged arms despite weaker hardware.

Level 3 - Autonomous Mobile Robots

Warehouse movers, autonomous mobile robots, self-driving vehicles, drones, quadrupeds, and even food delivery robots! Here the machine adapts to circumstances it was never built for: a self-driving car works on a road it has never seen, a quadruped walks an oil field. The environment barely changes, so this is where real robotics begins and the curve becomes a true exponential. But there is a ceiling, and naming it is the key to the whole ladder: these machines move through the world without reshaping it. They cannot manipulate their environment. That missing increment of generality is what caps Level 3.

The data takes another step up. The autonomous mobile robot market (around $4 billion in 2024) is compounding at roughly 20 to 27% a year, off an ever smaller and more immature base, and that is before you fold in robotaxis and drones, which are the same generality class. This is the first genuinely exponential robotics market as these machines adapt to existing warehouses, roads, and sites instead of demanding new ones.

Level 4 - Humanoids

This is the endgame. The robotic form factor that can replicate all of the human’s actions and fully replace physical labor.

The humanoid removes the last constraint, because it is built in the shape the entire built world was already designed for: the human body. Anywhere a person can go and act, it can go and act, so the environment needs no redesign at all. The redesign already happened, for us, over centuries.

Add manipulation, the ability to change the world and not just traverse it, and generality is complete. That is why Level 4 is the only rung shaped like an L-curve: a long flat approach, then a vertical wall.

Why is it vertical? Because for one, there is no market for humanoids today. It starts from a base of zero. And two, when you add manipulation, which is the final unit of generalization, the only difference between a robot and a human laborer is cost. For the world’s unglamorous manual labor (that humans don’t intrinsically derive enjoyment or purpose from and would much prefer to work another job) there is no reason to hire, not to hire a robot once the cost becomes lower than that of a human. Therefore, there is an economic crossing point after which, you can have a zero-to-one adoption curve.

“Analyst forecasts” are hilariously far apart: Goldman Sachs says $38 billion by 2035 (a figure it revised up sixfold in a single year), Morgan Stanley says $5 trillion by 2050. Basically, no one knows. Revenue is the wrong metric for a market that does not exist yet, and later I will argue the right metric is a capability number borrowed straight from how people forecast AI.

In conclusion, the more general the robot, the larger the addressable market, the smaller the current base, the more exponential the growth, and the more frontier-technology-like it is.

The Four Stages of AI

Now AI.

Level 1 - Pre-Programmed Expert Systems

If you’re deep enough in the AI rabbit hole, you might have heard of ELIZA.

Prior to neural networks, AI relied on expert systems, which is literally pre-written code.

Maybe some more relevant applications of expert networks are things like credit scores or insurance premiums or college admissions rubrics. This really isn’t even software. It’s literally just the concept of a decision tree. The equivalent of caged industrial arms. No one talks about them. No one cares about them. Yet they are ubiquitous and run a lot of our most important systems.

But they are not growing, they are not generalizable, and they are NOT technology.

Level 2 - Neural Networks

Have you heard of a CNN?

Convolutional neural networks were the major breakthrough in computer vision that allowed neural networks to tell the difference between cats and dogs, popularized in the 2010s.

This category also includes Google Translate and the chess engine Stockfish. They are all really good AIs! The only thing is they can only do one thing. When AI beat humans at chess, people freaked out for maybe two seconds and then didn’t gaf (give a fuck). The market didn’t gaf either. These things probably grew at the speed of the general software market and, despite being AIs, did not cause any technological acceleration or boom.

Why? Because you need to redesign you need to design the environment around the AI for the AI to work, just like you need to design the factory for industrial robots for those robots to work. For Stockfish to be the smartest human on the planet, you must give it a chessboard. For CNNs to properly classify images, you must collect labeled data.

Again, without proper generality, it is not a frontier technology with a true exponential.

Level 3 - ChatGPT

This is the first application of AI where people referred to it as a “moment.” Specifically, it was the ChatGPT moment. That’s how you know it’s a real technology with an S-curve.

This is the mobile robot equivalent because it moves. It moves not through physical space, but through domains of knowledge, from one field to another. It can do your high school close reading homework questions on The Great Gatsby then in the very same chat write you the code for a shitty SVG of a meme that you wanted to post online.

Yet it is still not able to act on the world. Exactly the reason why mobile robots are still separate from humanoids. And exactly the reason why there was still another moment ahead where the growth turned from an S-curve to an L-curve.

Level 4 - Agentic AI

Ah yes, Claude Code. The reason why SMH is up 76% YTD. It’s so useful that literally everything is in shortage.

Not an AI that answers, but an AI that does work, entering any computer and operating it. This is the humanoid of software, and the operative word is the same one that capped Level 3: manipulation. The agent manipulates the digital environment the way a humanoid manipulates the physical one, and that last increment of generality turns the S into an L.

Conclusion

We have had AI since the 1960s and genuinely useful AI since the 2010s, yet the world did not care until 2023. Why did decades of AI grow at the pace of the ordinary economy rather than like “AI”? Because Levels 1 and 2 were domain-specific, and a domain-specific technology spreads only as fast as the environments built around it, exactly like Level 1 and 2 robots. The curve bent only when generality arrived. The lesson transfers cleanly: robotics has already had its long 1960-to-2010 era, and it is about to have its 2023.

The Big Three Labs

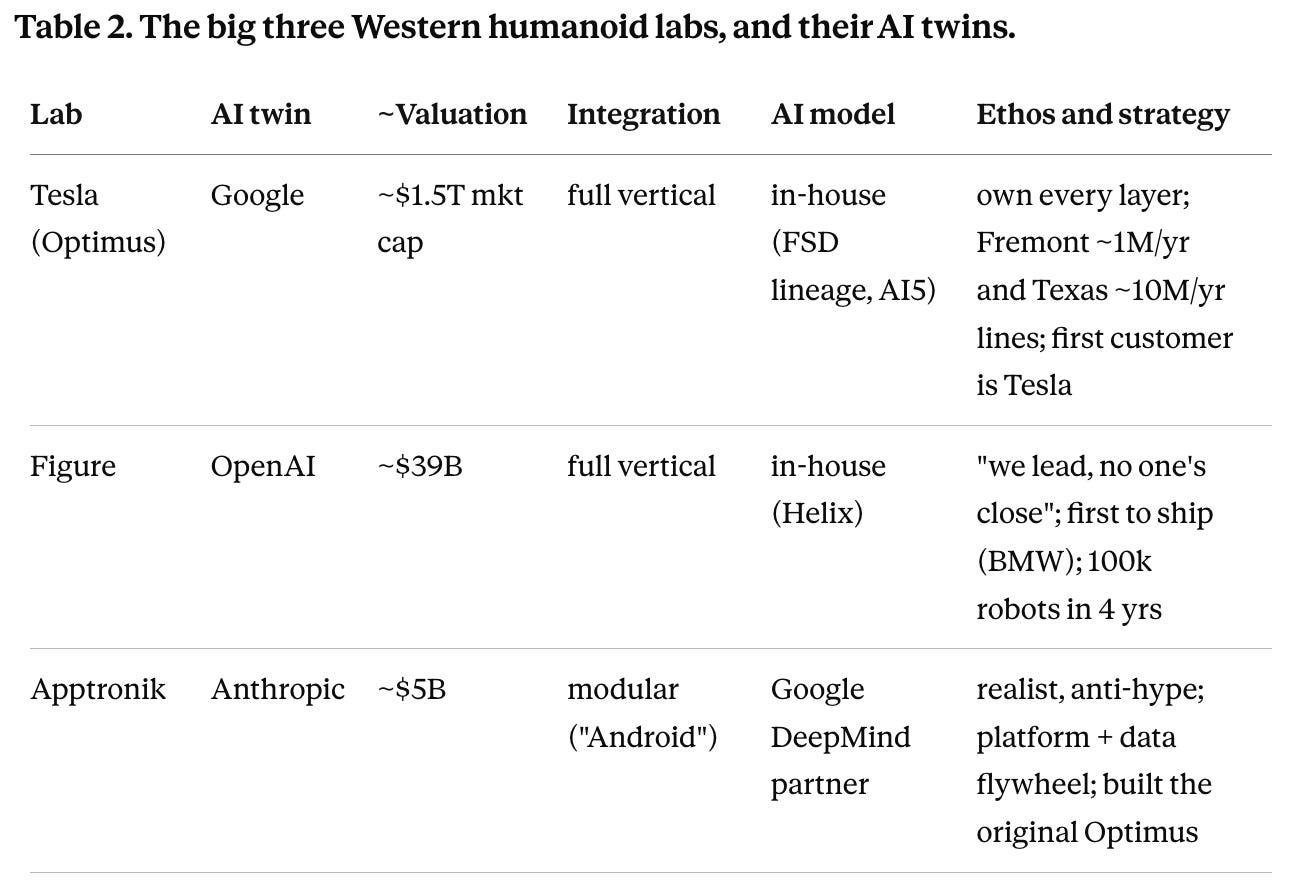

Robotics is so AI-coded that even the big three labs are the same.

You know the AI labs, OpenAI, Anthropic, and Google. But what about the robotics labs?

…FigureAI, Apptronik, and Tesla!

They match one for one, do you see the resemblance?

…no?

Figure is (early) OpenAI. The “posterchild” pure-play private that has the highest valuation ($39b) and is “in the lead.” Both their names even end with AI!

They have a backer list (Microsoft, Nvidia, OpenAI, Jeff Bezos) that reads like OpenAI’s own cap table. If you have watched Brett Adcock say at least three words, you will understand that their entire ethos is we are the leader and no one is close. They are fully vertically integrated and have the Apple approach: building both the hardware and its own AI models (its Helix system, no reliance on an outside model vendor), and it was first to ship to a paying customer, BMW, back in 2024. It talks in maximalist terms, 100,000 robots over four years, a path to being one of the most valuable companies on earth. Figure is the maxi poster child, and like OpenAI it draws both the most hype and the most “they are promising way too much” skepticism. But if you think back to the OpenAI spending commitments (and ORCL chart manipulation), when you’re the maxi, people think you’re crazy at first until you get proven right, so this company might just be a fantastic bet.

Apptronik is Anthropic. The names literally rhyme. They are the pragmatic and heads-down-execution focused counterpart to Figure. They are valued way lower at $5b.

Its founders are openly disciplined and anti-hype, and they will more or less tell you the other guys are taking advantage of irrational exuberance and “not doing the work.” Strategy-wise Apptronik is the Android of the space: more modular, more model-agnostic, a platform play rather than a single sealed product. It partners with Google DeepMind for the AI model (DeepMind’s largest-ever investment) while owning the hardware, the platform, and the data flywheel.

Tesla is Google. This is self-explanatory as they are both Mag7 companies with a frontier lab division (Optimus for Tesla, Deepmind for Google).

Just like Google, they are vertically integrated in a way that the labs cannot be. The labs can be vertically integrated, but as a mega cap, you can be hyper vertically integrated: the robot, the factories, its own TPU edge chip (AI5), the batteries, the AI training stack, and, critically, its own first customer, since the first place Optimus has to earn its keep is inside Tesla’s own factories. This probably means a lower risk for initial deployments and a big data advantage. To push this Google parallel thing further, it’s like deploying Gemini across the entire Google ecosystem. So yeah the Google of Hardware.

Then there is of course Unitree (China) which is DeepSeek with the exception that they are already a behemoth. They have by far the lowest cost structure with a BOM 1/3 of that of western leaders and offering their flagship H1 at $16k. This is simply due to them being within ten miles of all their suppliers, unlike the West, which has to import parts from Germany and Japan. This works great for semiconductors, where niching down is an asset and talent is spread across the world (because quality and pushing the frontier is paramount), but in robotics it’s actually iteration time and cost structures that are most important.

But unlike with AI, there is no open sourcing. Western markets will ban Chinese robots. So the Western market will be divvied up by the leading Western labs. I do not believe Unitree will participate.

The Elbow of The L-Curve

This is an L-curve. The elbow is what the person is standing on (and I’ve circled it too).

Definitionally, when I say something has an L-curve, it must mean that I expect there to be an “elbow moment” when it turns from flat to vertical. In agentic AI the elbow was Claude Code and we reached it earlier this year.

So what is the elbow for humanoid robotics? And when do we reach it? I believe there is one answer.

When it is cheaper to hire robots than humans to perform repetitive, fixed-station, load-bearing manual labor.

There are several things that I am saying with this one sentence.

Cheaper. This means that we must analyze the cost structure of humanoid robots.

I only define one category of tasks. This means I implicitly believe that repetitive fixation load-bearing manual labor is THE use case sufficient to reach the elbow.

Let’s focus on the price first.

The price dynamic is less prominent for AI and knowledge work just because knowledge work is much more quality-focused than cost-focused. The takeoff moment for AI has always been caused by capability and not price. Think about it. The METR time horizon chart measures the longest task an AI can perform, NOT how cheaply it can perform a certain task.

This is structural. Think about it. Token generation is orders of magnitude faster than human writing. When working with bits, it’s only natural that the virtual-native entity wins in speed and efficiency. The only question is whether it can match a human’s original thought quality.

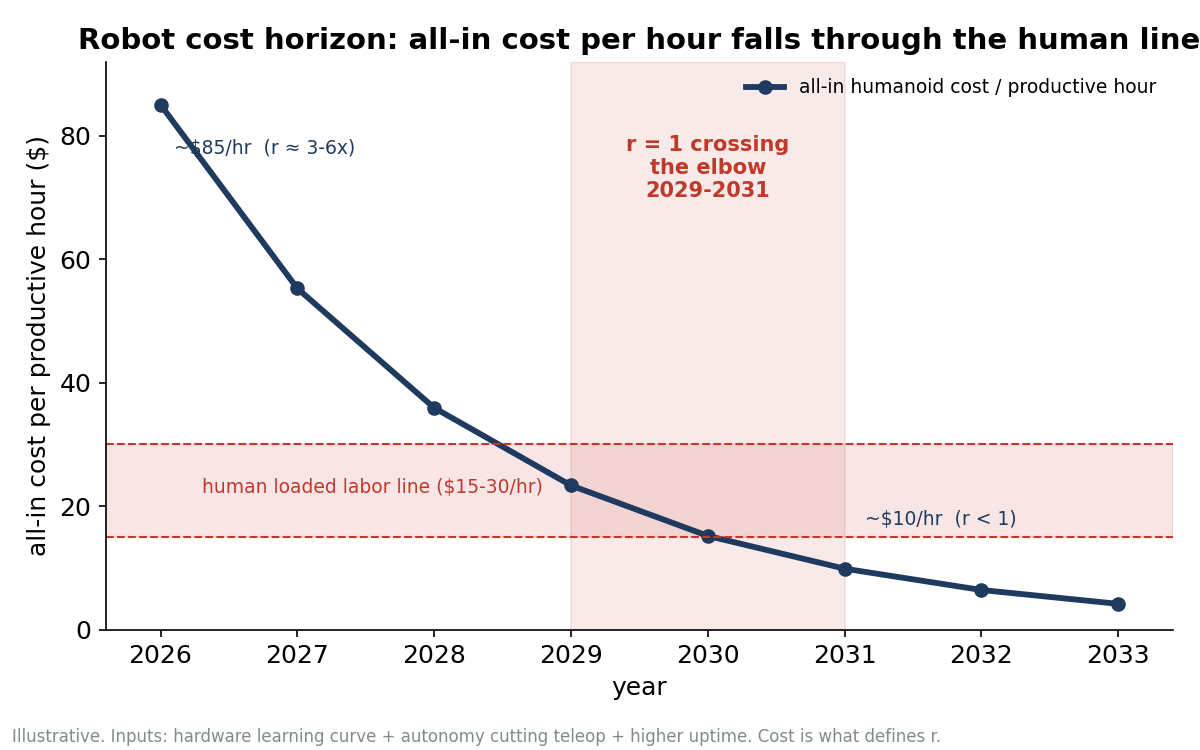

However, in the physical world, nothing innately makes a robot faster than a human, as they are bound to the same laws of physics that we are. Therefore, you could probably get a robot to perform any task today with enough point training, task-specific RL, completion time, patience, and teleoperation. The only difference would be cost. Therefore, the robotic equivalent of the METR time horizon chart is an hourly labor cost index, like this excellent one provided by SemiAnalysis.

In order for robots to cross the cost threshold, the all-in price of a robot (purchase price per hour of useful life + expected cost of maintenance + expected human teleoperation time + expected cost of quality/reliability) must be lower than the all-in price of a human (hourly wage + taxes, medicare, social security). The all-in cost of a robot is usually not itemized like this from the perspective of the end consumer, as it is usually wrapped into a robot-as-a-service (RaaS) contract. Also, by using hours, I am ignoring the idea that robots don’t get injured, sick, or tired and can work double shifts, because that is just calculated into the purchase price per hour of useful life by extending the useful-life-hours.

Let’s make this nice and mathematical.

for a specific task, r = (robot $/hour) / (human $/hour)

r > 1, hire some dude. r < 1, use a RaaS. When r falls below 1 on a task that is a large share of the economy, the elbow has arrived.

Now actually run the numbers. How far are we?

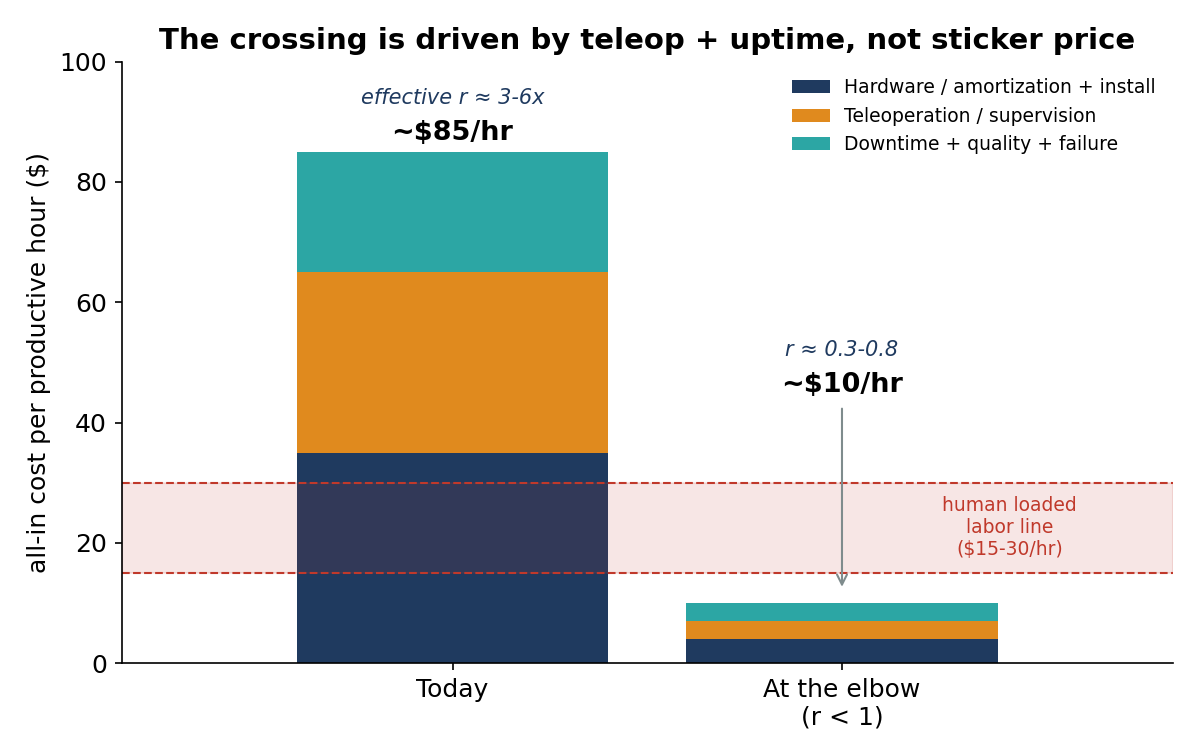

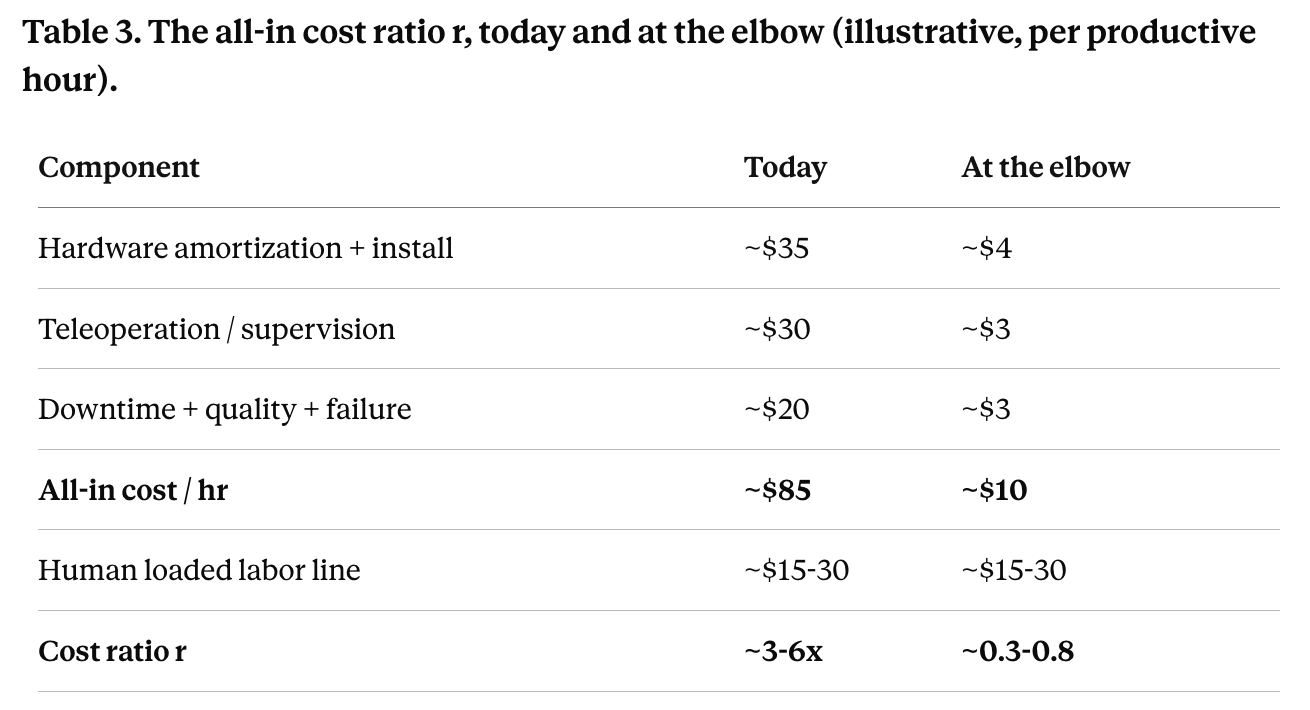

Figure leases its robot at around $100,000 a year, and experts describe a real deployment today as something like a $50,000 robot plus six figures of onsite integration plus a human minder to babysit it. Amortize the hardware, add a teleoperator who can supervise only a few robots, and account for low uptime and rework, and a robot’s all-in cost today lands somewhere around $85 per productive hour, against a human line of $15 to $30. So today’s r is roughly 3 to 6x.

Robots are not close, which is why current deployments are really subsidized pilots and data-collection exercises, not real business. But it’s not an order of magnitude off!

But look where the cost is. The sticker price is already near parity: a $100,000-a-year robot that runs two or three shifts is competing with two or three human workers, so the hardware alone is only slightly above the line. The thing keeping r at 3 to 6x is the teleoperation and reliability. That is the entire game. The crossing does not require a cheaper robot so much as a robot that needs far less babysitting and runs far more of the day. When autonomy rises enough that one supervisor covers fifteen robots instead of three, and uptime climbs toward multi-shift, the all-in number collapses toward $10 per productive hour and r drops below 1.

Moravec’s Paradox

In my definition of the elbow, I only defined one category of tasks. Now we will discuss why.

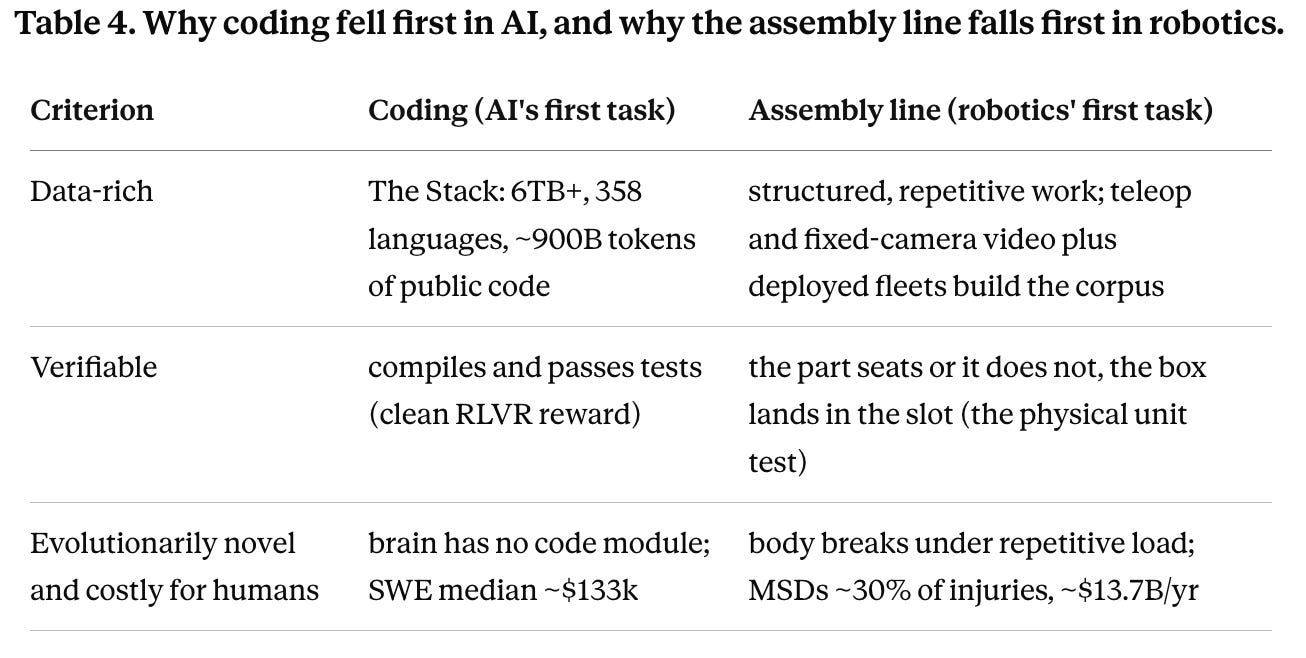

I believe for AI, there was one use case and one use case only which helped us achieve economic takeoff: coding. It was a task that is large enough in the economy and the first for automation to reliably outperform humans. I call a task this set of attributes a critical task.

To grok the nature of a critical task on a much deeper level, let’s visit a concept known as Moravec’s Paradox.

In the 1980s Hans Moravec, Rodney Brooks, and Marvin Minsky noticed something strange about AI: it is comparatively easy to give a computer adult-level performance on intelligence tests or chess, and almost impossible to give it the perception and mobility of a one-year-old. The explanation is evolution. The longer natural selection has worked on a skill, the more deeply optimized and the harder to reverse-engineer it is. As Moravec put it, encoded in the sensory and motor parts of the human brain is “a billion years of experience about the nature of the world,” while “abstract thought is a new trick, perhaps less than 100 thousand years old.” This yields the master ordering rule for the whole automation wave: machines conquer human tasks in roughly the reverse order of how long evolution spent building them. Evolutionarily recent skills, symbolic, abstract, structured, fall first; evolutionarily ancient skills, perception, dexterity, locomotion, social reading, fall last.

It is these evolutionarily recent skills, specifically the ones that matter for the economy, that are candidates for being a critical task.

Now let’s look coding’s fundamental attributes.

Data rich. The corpus already existed. BigCode’s “The Stack” assembled over 6TB of permissively licensed source code across 358 programming languages, roughly 900 billion tokens in its second version, scraped from public GitHub. Decades of human code were sitting there, labeled and ready, the way no physical-action corpus is.

Verifiable. Code compiles and runs, or it does not. That objective, automatic signal is what let reinforcement learning with verifiable rewards work on code and math when it stalls elsewhere: the reward comes from a compiler or unit test, it is binary and bias-free, and the model cannot easily hack it. A clean reward is a cheat code for machine learning, and code hands you one for free.

Evolutionarily novel, therefore scarce and highly paid. Programming is so recent that the brain has no dedicated machinery for it. An MIT study found that reading code does not recruit the brain’s language network at all, it lights up the general-purpose “multiple demand” network, and the authors note that “computer programming is such a new invention that there couldn’t be any hardwired mechanisms that make us good programmers.” So competent programmers are rare and expensive.

Instead, human brains are optimized for social intelligence. Social interaction is inherently far more complex than writing a few lines of code. Yet our brains handle every micro input subconsciously, without us even having to notice it.

TLDR: Hard for us, useful for the economy, easy for a machine? Automate it.

So now let’s translate this to our physical bodies. What is the physical equivalent of coding, and what is the physical equivalent of social intelligence?

The body’s equivalent of social intelligence is endurance running. Humans are the best endurance runners in the animal kingdom, a capability that emerged about two million years ago in the genus Homo, with spring-like tendons, an upright gait, and, above all, a cooling system without peer: two to four million eccrine sweat glands spread over nearly hairless skin, giving humans the best evaporative thermoregulation of any primate and the ability to run prey to heat exhaustion in the midday sun, a tactic called persistence hunting. We can also add precision dexterity to the mix, as our hands have dozens of degrees of freedom and our senses are hyper-tuned to its positioning.

(As they always say, it is sweating and opposable thumbs that let humans take over the world.)

The body’s equivalent of coding is factory work. Evolution optimized the body for varied, intermittent movement, not for repetition or sustained static load. The assembly line is barely a century old, Ford put it together in 1913, and the body has no adaptation for performing the same motion thousands of times a shift or holding a loaded posture for eight hours. So it breaks, measurably and expensively. Overexertion and musculoskeletal disorders are roughly 30% or more of all US workplace injuries, transportation and warehousing carry the highest serious-injury rate of any major sector, and over a million Americans suffer serious back injuries each year (US BLS). Overexertion from lifting, carrying, pushing, and pulling is the single most expensive category of serious workplace injury, about $13.7 billion a year in direct US costs, the bulk of it manual material handling (Liberty Mutual Workplace Safety Index, 2024). That injury bill is the body “hating” the task, the precise physical analogue of the brain hating symbolic logic.

We have our answer. The critical task, the “coding” of robotics is repetitive, fixed-station, load-bearing manual labor. Machine tending, parts and package handling, palletizing, sorting, kitting, repetitive insertion and assembly. It clears all three bars at once, for the same reasons coding did.

In addition, factory work is pretty big and important to the economy if you ask me. This is why the first customers of these humanoid startups are all car factories.

Finally, let’s look at the other side. The last physical tasks to fall are the body’s social-intelligence equivalents: dexterous, varied, unstructured, socially embedded work, the nurse’s touch, the chef in a chaotic kitchen, and childcare. High evolutionary investment, high Moravec tax, low data, low verifiability, deeply social. That bundle is the robotics version of humor, and it is the part of physical labor that stays human longest. The same evolutionary moat that protects the social parts of white-collar work protects the dexterous, caring, and improvisational parts of physical work.

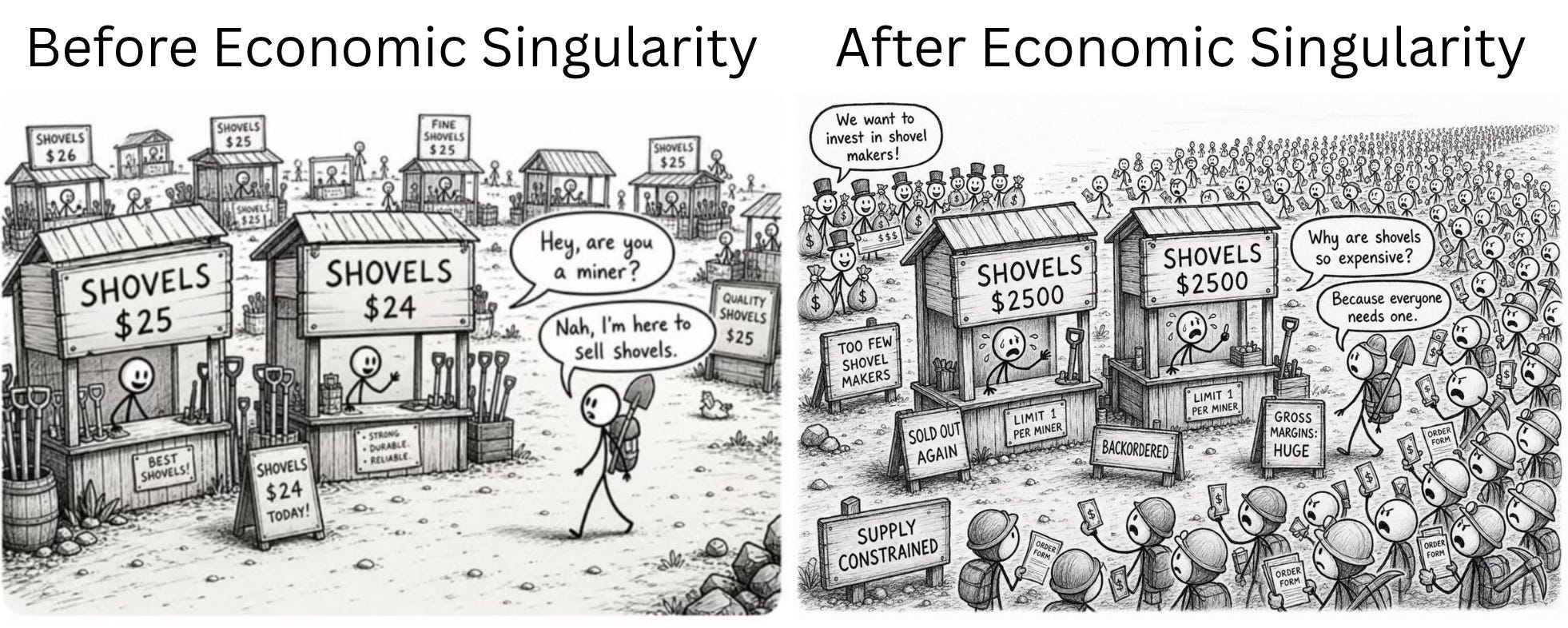

The Economic Singularity

What happens once the elbow’s reached and the critical task is automated? Well, my friends, I introduce you to the concept of economic singularity.

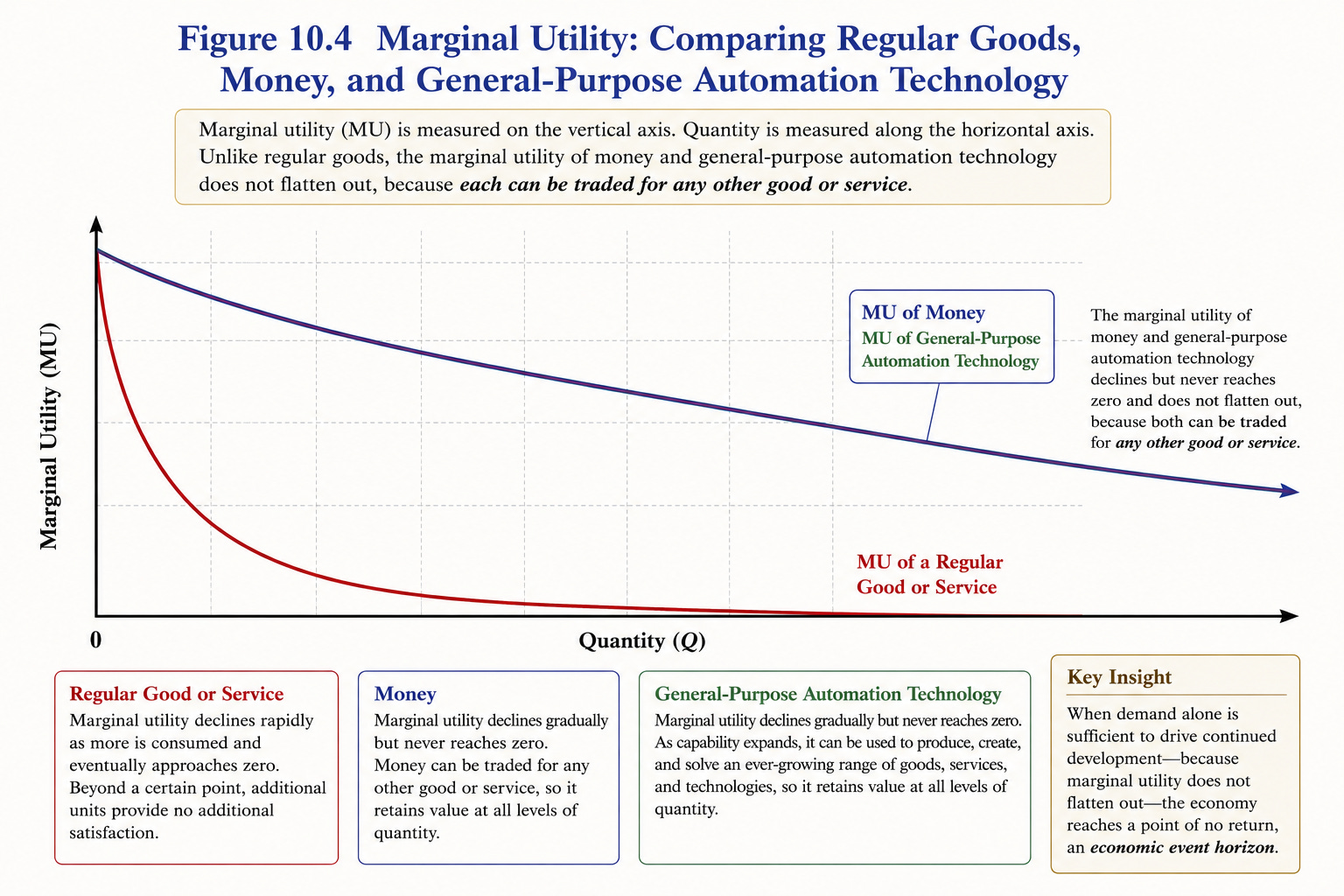

Economic singularity: the state in which a technology is so cheap and so useful that no actor retains the agency to stop its development, because demand alone now forces it forward.

It is not necessary for a technology to be in the economic singularity state for a huge build out to occur. Take AI in 2023 and 2024. Hundreds of billions were being poured into capex while the bears argued that there is no way chatbot subscriptions can pay for all of it, and I agree! But that doesn’t mean the build-out has to stop. It just meant that its continued development was contingent on the decisions of the parties funding the development. You could have stopped it by convincing Satya Nadella, Andy Jassy, and Sundar Pichai to halt AI capex.

I believe the economic singularity has occurred (or more accurately, an economic event horizon, a point of no return) when demand alone is sufficient to drive continued development. The reason why this is a “point of no return” and not simply a temporary supply-demand imbalance is that, theoretically speaking, the marginal utility of a general-purpose automation technology like AI or robotics never flattens out, similar to the marginal utility of money itself, as it can be traded for any other good or service. Smartphones saturate when everyone owns one, but here, the TAM is GDP itself.

This is what happened with Claude code. Now you can convince those same three CEOs to stop tomorrow and nothing changes, because demand is so overwhelming that someone else simply spends to meet it. Capability is now sufficient to ensure AI’s own continuation. Development left the agency of any company and passed to the market. That is the singularity: capitalism, not a boardroom, drives it.

This is what will happen to robotics once r < 1.

Today humanoid R&D is a discretionary bet placed by a few well-capitalized companies. Development contingent on their agency. Once the critical task crosses r below 1, Level 4 hits the elbow: buyers demand robots faster than anyone chooses to build them, demand becomes the driver, and production becomes self-pulling.

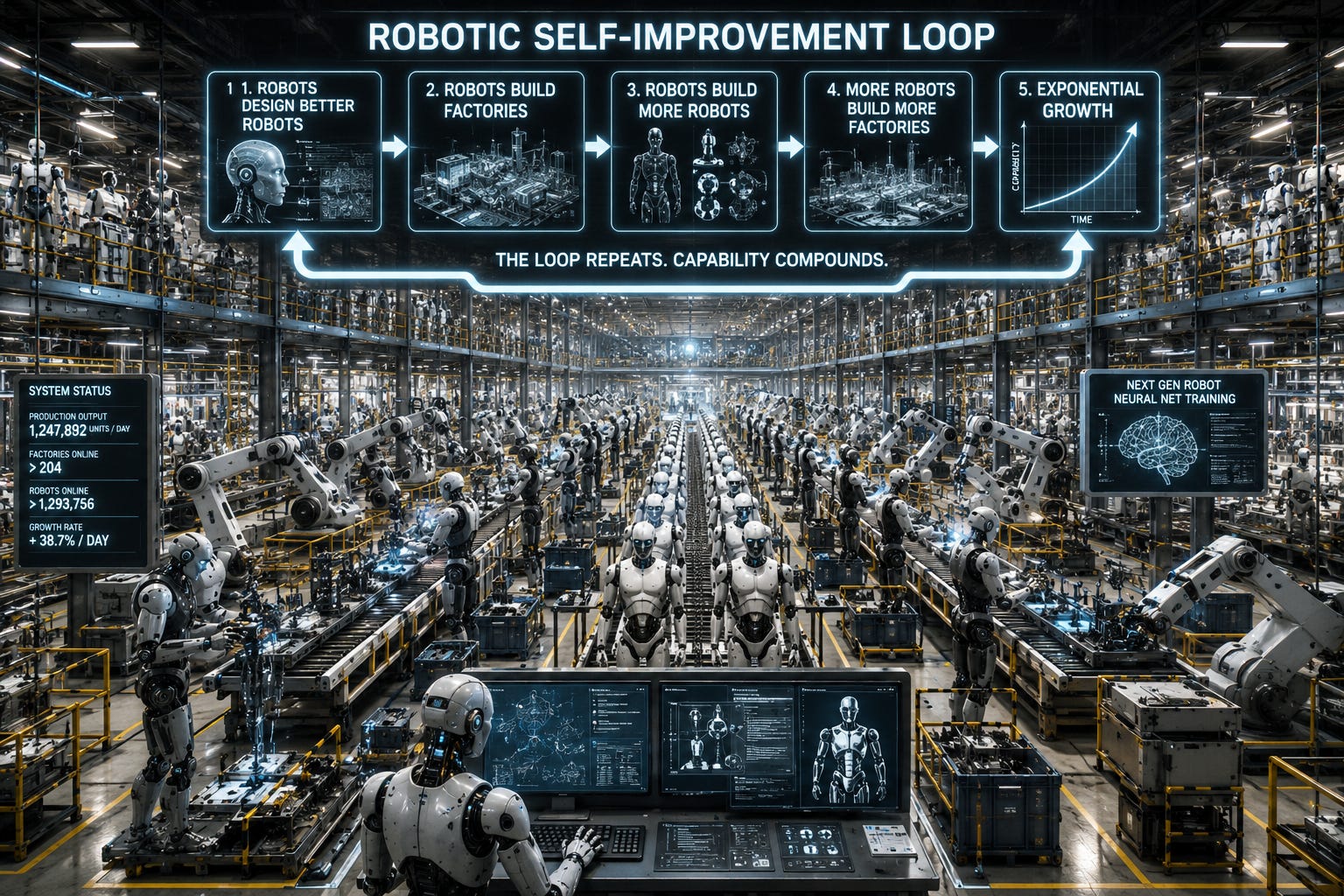

Robotic Self-Improvement (RSI)

It’s recursive self-improvement… but robots. Robotic Self-Improvement!

Recursive self-improvement is simple. An AI good enough to do AI research designs a better AI, which designs a better one, and capability compounds with no human in the loop. That is the digital singularity.

Robotic self-improvement is the same loop in the physical domain. A humanoid general enough to build robots and to build and run the factories that build robots closes a physical cycle: robots staff the lines that produce robots, which build the factories that produce more robots. They multiply like bacteria.

This is the end game. I believe we are likely to reach RSI for AI before RSI for robots, just because AI development is approximately 4 years ahead. However, once you have both, you have reached the ability to automate every single part of the economy.

They feed back on each other too. Better AGIs design better robots to speed up robot production even more and better robot neural nets to make them smarter, while robots build better fabs and datacenters to feed the AGIs. Double infinite recursion.

This is infinite GDP.

Conclusion: Predicting ChatGPT and Claude Code Moments

There are two robotics inflection points to try to predict:

The ChatGPT moment, which is when level 3 reaches the inflection point of its S-curve

The Claude Code moment, which is when level 4 reaches the elbow of its L-curve

I believe we’re in the robotics equivalent of AI’s 2022. The ChatGPT moment is likely just around the corner while the Claude Code moment is ~4 years away. This puts robotics at a development stage roughly 4 years behind AI.

The robotics ChatGPT moment: 2026 to 2028, just beginning now. This is Level 3 taking off, the first real exponential, mobile and perceptive machines crossing into broad use. We have not quite had it yet, but 2026 is where the inflection starts to show. Here we want to track the KPIs, like miles driven, revenues, number of deployments, and whatnot. There are many tasks and forms of robots (unlike level 4 and humanoids) so the correct measure is an aggregate of many measures. For example, autonomous mobile robots are compounding north of 20% a year, and robotaxis are growing pretty quickly: Waymo went from about 250,000 paid rides a week in early 2025 to roughly 450,000 to 500,000 by early 2026, doubling in under a year, with a stated path past one million a week by the end of 2026. Tesla is not doing bad either. We are honestly almost there; all that has to happen is for the public to start becoming enamored with one of these products, and I think there’s a solid chance it happens in 2027.

The robotics Claude Code moment: 2029 to 2031. This is Level 4 humanoids hitting the elbow, the critical task crossing r below 1, and the economic singularity engaging. Here revenue is useless, because there is none, exactly as there was no “coding revenue” to extrapolate before agents arrived. So borrow the trick that actually worked for AI. METR measured AI capability as a task time horizon, the length of task (in human time) a model can finish at 50% reliability, and showed it doubling roughly every seven months, an extrapolation that has tracked reality really damn well and let people call the agent inflection before it happened.

The robotics analog is the cost horizon on factory labor.

This is illustrative, but I believe a chart like this is going to become the robotics equivalent of the METR time horizon chart for AI, religiously tracked on X to answer the question of whether scaling laws are intact. If we assume that robotics costs decline in line with Moore’s Law (i.e., a halving every two years), then we will reach the elbow in 2030. If we assume that robotics development is four years behind AI and the robotics Claude Code moment happens 4 years after the AI Claude Code moment, which was 2026, then we also land at 2030. Therefore, 2029-2031 is my current timeline.

Now for closing thoughts. As investors, we are blessed. We have watched the first General Purpose Automation Technology take off, and through empirical observations, we have understood every stage of its inflection. Today, we sit at the precipice of the takeoff for the second. Robotics’ attributes are fundamentally analogous to what we observed and understood about AI, allowing investors to make predictions with far higher confidence than betting the farm on AI infra back in 2022.

Yet the world (and the market) doesn’t see it because it’s not yet “in your face.” That is our opportunity.

A part of me finds this all funny... everyone's thinking about making money but we're inventing the terminator in real time lol