Sivers Semiconductors Earnings Review Q1 2026 (Free)

Can I pay my bills with opportunity?

I think it’s time to stop bashing this company aimlessly (and won’t have any coverage on it until next quarter probably) but I do still think they are a very interesting business and that’s why you are reading this brief on their earnings right now. TLDR: Still a shitco (neutral earnings) but will give them credit where credit is due in some areas (but still bash them in others). Bimodal earnings review.

By accessing this content, you acknowledge and agree to our terms and conditions. This research is not financial advice.

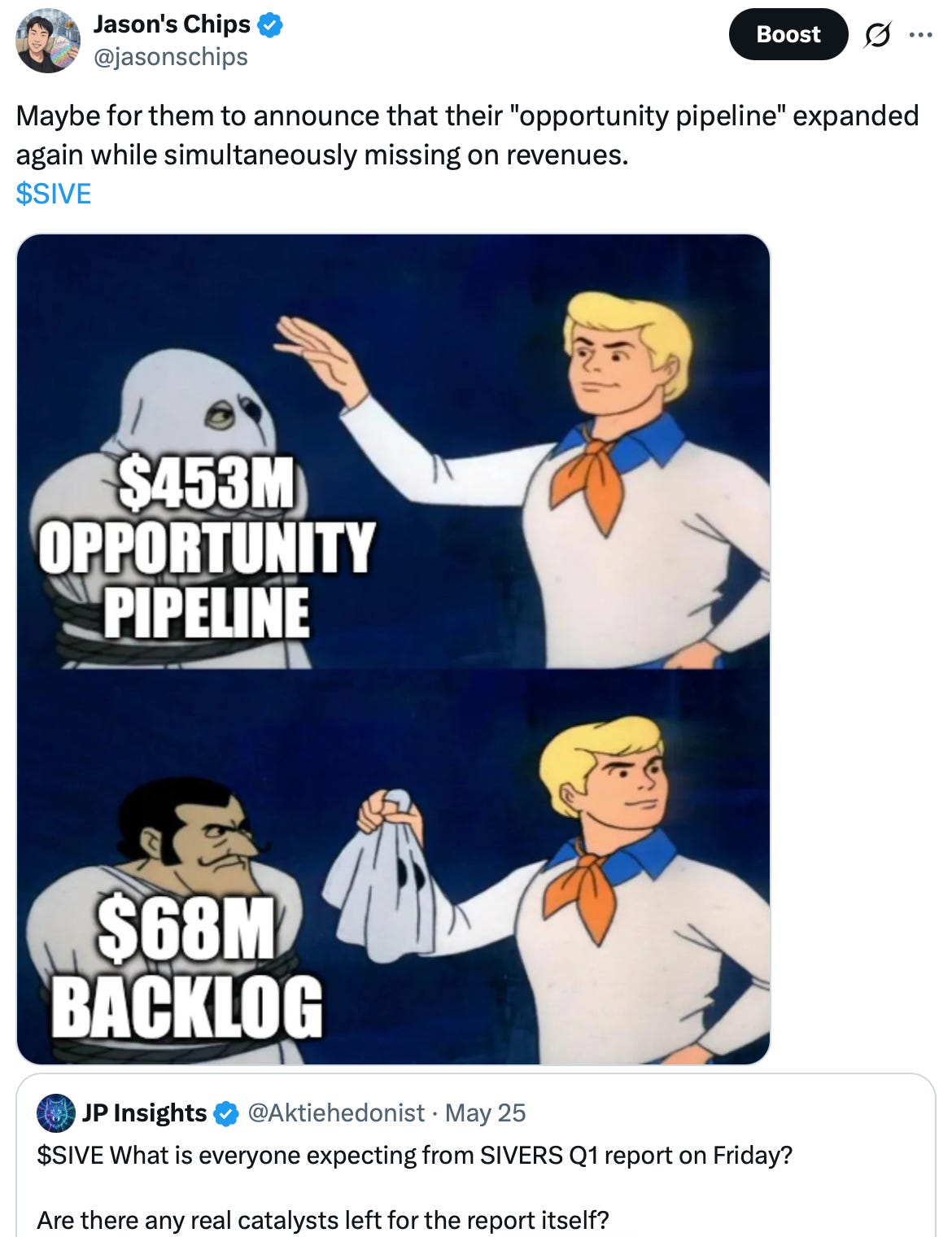

I am a wizard and absolutely nailed their earnings with my tweet.

They did, in fact, announce that their "opportunity pipeline" expanded again, while being simultaneously missing on revenues.

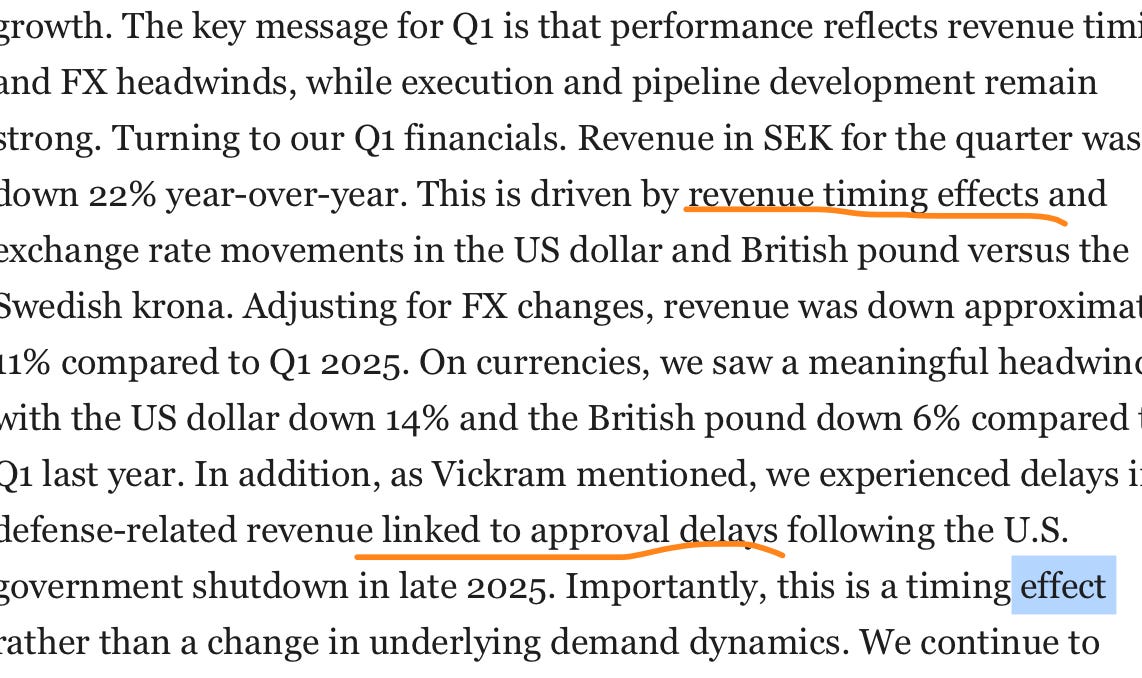

Revenue Misses

I will bash them in other areas, but I am actually not going to do so here. I completely buy this excuse, because if this was any other company that I cover, I would have given them the benefit of the doubt as well. This honestly doesn’t matter as much at all for whether or not their CPO shenanigans will take off.

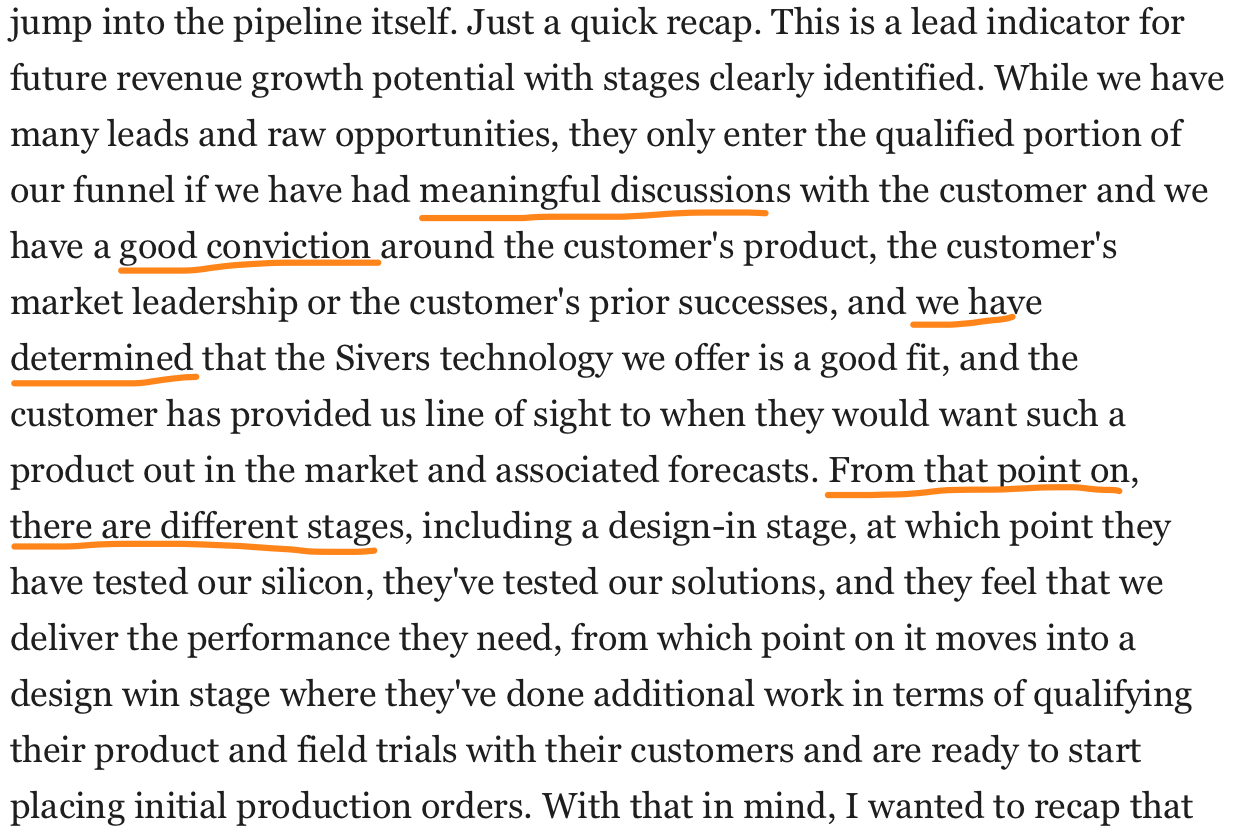

Opportunity Pipeline

Bashing time! If I were sell-side, I would be absolutely dishing out questions to management over this. Every single mechanism for defining the opportunity pipeline is up to the discretion of management. Not a single one is objective. Not a single one relies on contracts.

What does meaningful discussions mean? What does good conviction mean? What does determining that Sivers’s technology is a good fit mean? No one knows. The management can define those however they want. This doesn’t necessarily lead to the opportunity pipeline being an inflated metric per se. Management could be even more conservative if they chose to. It just means that this is a metric that is manipulatable and should mostly be treated as noise and not signal. I’m sure if you had the right incentives, you can easily manipulate this pipeline to be an entire order of magnitude larger or smaller than it currently is.

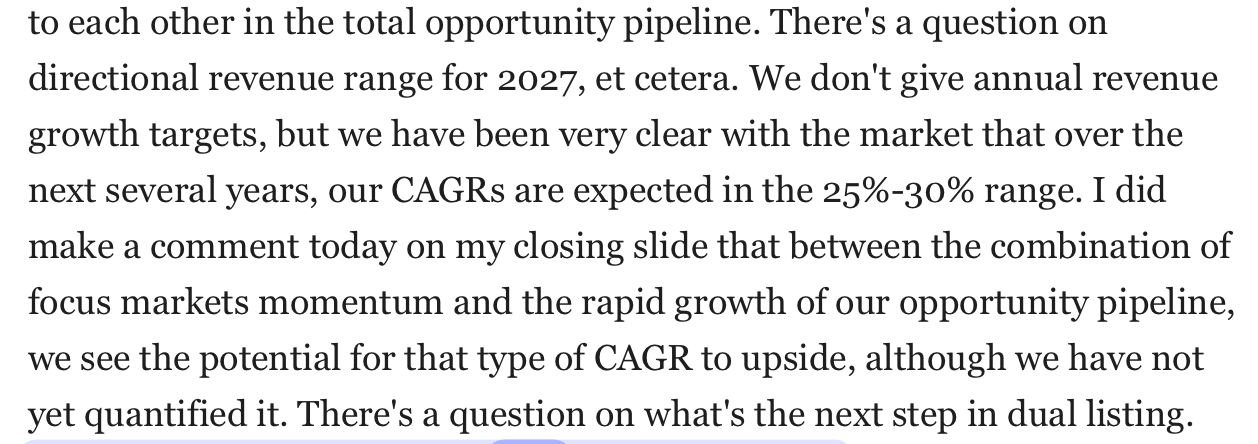

The biggest red flag is that Vickram Vathulya does not address any forward revenue guidance.

This question is a clear invitation to share numbers, and it was dismissed with a one-sentence answer on their themes.

Their end markets are growing way faster than this BTW. CPO should be triple-digit growth.

No qualifications, no production volume orders, nothing changed.

Competition

Here they just completely conceded that they are worse than Lumentum in every way. All they needed to mention, like most companies when they’re asked this kind of question, was at least one area in which they are competitive and to talk that up as the more important trade-off. You can see Coherent doing this all the time with their 6-inch wafers, even though they are uncompetitive everywhere else, but they still have something to talk about.

The only response Sivers could give was “…but the pie is growing!” TAM doesn’t pay the bills if you can capture none of it.

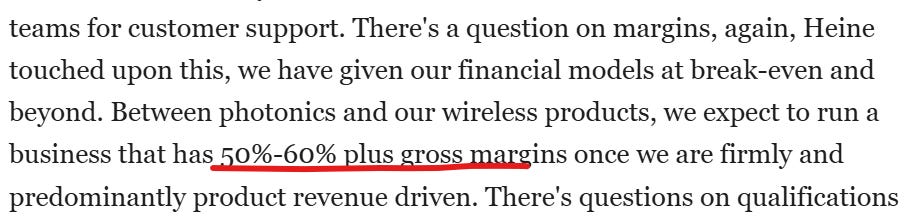

Margins

This is very good. COHR GMs are barely above 40% for reference. Achieving this would actually be remarkable. Credit where credit is due.

Conclusion

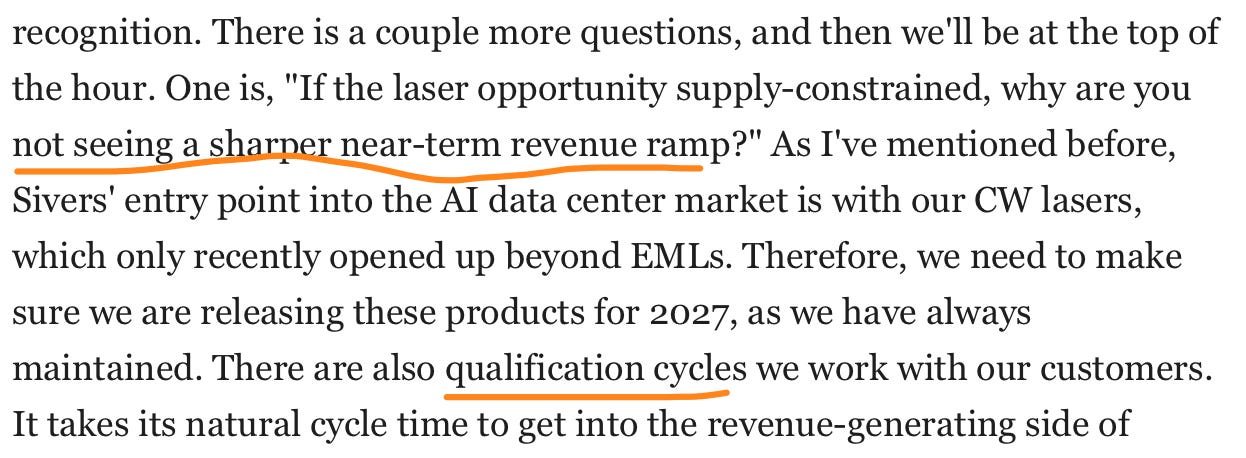

This last question in the Q&A captures perfectly the essence of Sivers today.

Maybe because they’re not actually a volume supplier to the market since they haven’t qualified anywhere?

Everything else is noise until they give purchase order announcements with clear numerical amounts, and provide year-by-year revenue guidance. Until then, they’re a startup, and nothing has changed.

Both on the good side and bad, for example, the revenue miss today doesn’t matter at all, and neither does the “opportunity pipeline.” I guess that just means I’m saying that earnings don’t matter at all. LMAO.

See you next quarter!

This aged poorly. I wished i have not read this and increased my position

repeatedly stressing that the opportunity funnel is bogus bc its up to management discretion is not intellectually honest