Sivers Semiconductor | The Most Overvalued Stock in Optics (Free)

Crusade against the pump and dump

I hope my jihad against Sivers has brought you excellent entertainment.

It was only a few months ago when photonics was a niche, technically complex subsector of a subsector of a subsector of the AI infrastructure trade, covered by small, undiscovered, and specialized analysts. Today, it shares an investor base with 2021 NFTs and 2024 Solana meme coins.

But unlike crypto, the technology and fundamentals are still there!

So it’s truly become a fascinating contradiction where on one side there are companies with real technology and an almost perfect market position. There is some hype around them, but that hype is not nearly enough, and they still present a great opportunity (see LITE 0.00%↑). On the other side there is Sivers.

Sivers is special. Before all the speculation promoted by unethical large social media accounts, there was a legit investment thesis! Credit to the several analysts that found it pre-cult.

Now I will pretend that Sivers is $130 million market cap again, and pitch the original thesis. It is by doing this that we can fully understand why it has broken after a 20x, unlike names like AXTI 0.00%↑ and SNDK 0.00%↑.

We will be analyzing Sivers (and finding out why it is insanely overvalued) through a purely fundamental lens. I will not comment on the market structure or price action or ethical/legal concerns, or criticize any of the individuals that have promoted this name. I will instead save that for my tweets (lol).

Oh, by the way, for anybody asking me to short, I wish I could, but I can’t because IBKR won’t let me. My account is restricted to cash only.

By accessing this content, you acknowledge and agree to our terms and conditions. This research is not financial advice.

Contents

The Original Thesis

The Valuation is Absurd

Sivers 101: Opportunity Pipeline & NRE

The (Fabricated) Bull Case

Why Is Sivers Fabless?

There is No Moat

The Wrong Architecture

Conclusion

The Original Thesis

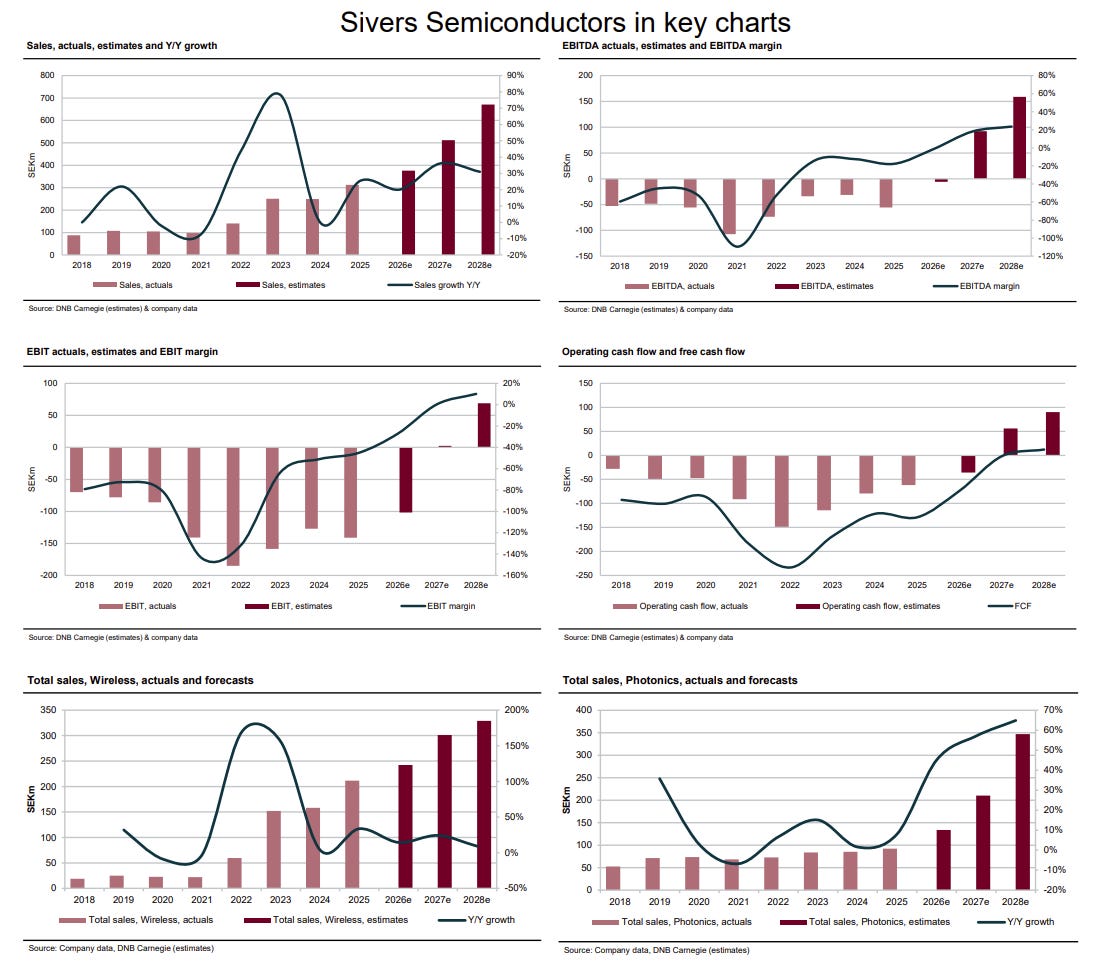

Sivers is a company with two segments: wireless and photonics.

Wireless makes up 70% of 2025 full-year revenues. Photonics (which includes both data center photonics and LIDAR) makes up the other 30%.

The company is cheap. With a $130 million market cap and around $33 million of revenue, Sivers trades at almost exactly 4x EV/revenue.

Profitability is constrained as EBITDA is currently negative, but that’s the whole point. A company that is cheap on EV/revenue with negative EBITDA that has a hidden gem segment (photonics) can show massive operating leverage if that hidden gem segment explodes.

This is precisely what sell side projects. While the legacy wireless segment is forecasted with pretty unexciting growth (5G and radar and satellite stuff), photonics, which includes both LIDAR needed for physical AI and, most importantly, CPO for data centers, carries the company to double-digit sales CAGR and their 20% EBITDA margin goal.

With revenues doubling by 2028 and EBITDA margin inflecting positive, suddenly you go from 4x EV/revenue to 2x EV/revenue and 10x EV/EBITDA. By 2028, photonics would make up half of the entire company’s sales, making this an attractive bet.

Not much has to go right here. At a market cap of $130 million, the thesis can simply rely on management delivering on their own stated goals.

The Valuation Is Absurd

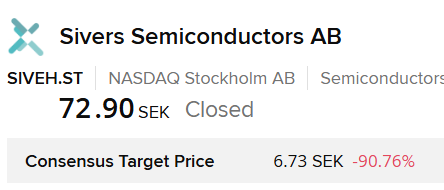

The sell-side price target is less than 10% of the current market price, which I find absurdly funny. (It is really funny.)

I think the ridiculousness of this valuation is best explained by my tweets during my retard crusade last weekend.

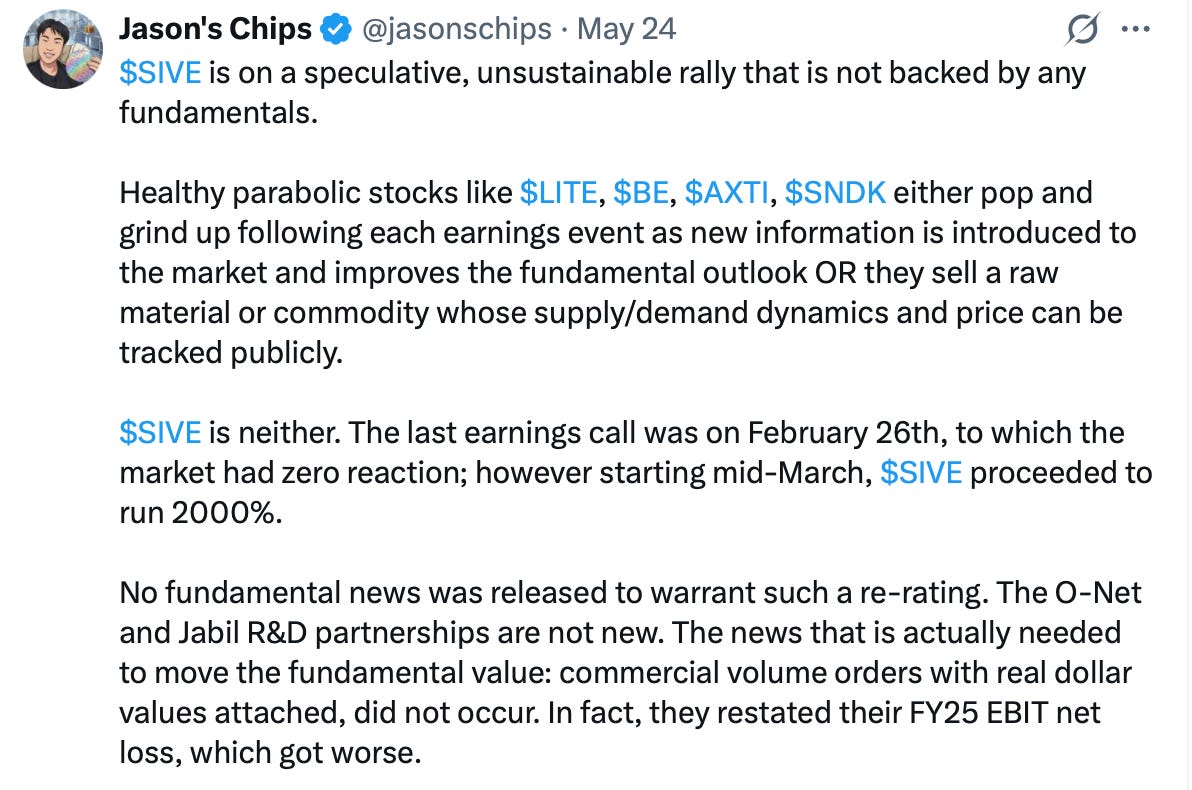

And the way it got to this valuation is also extremely unhealthy.

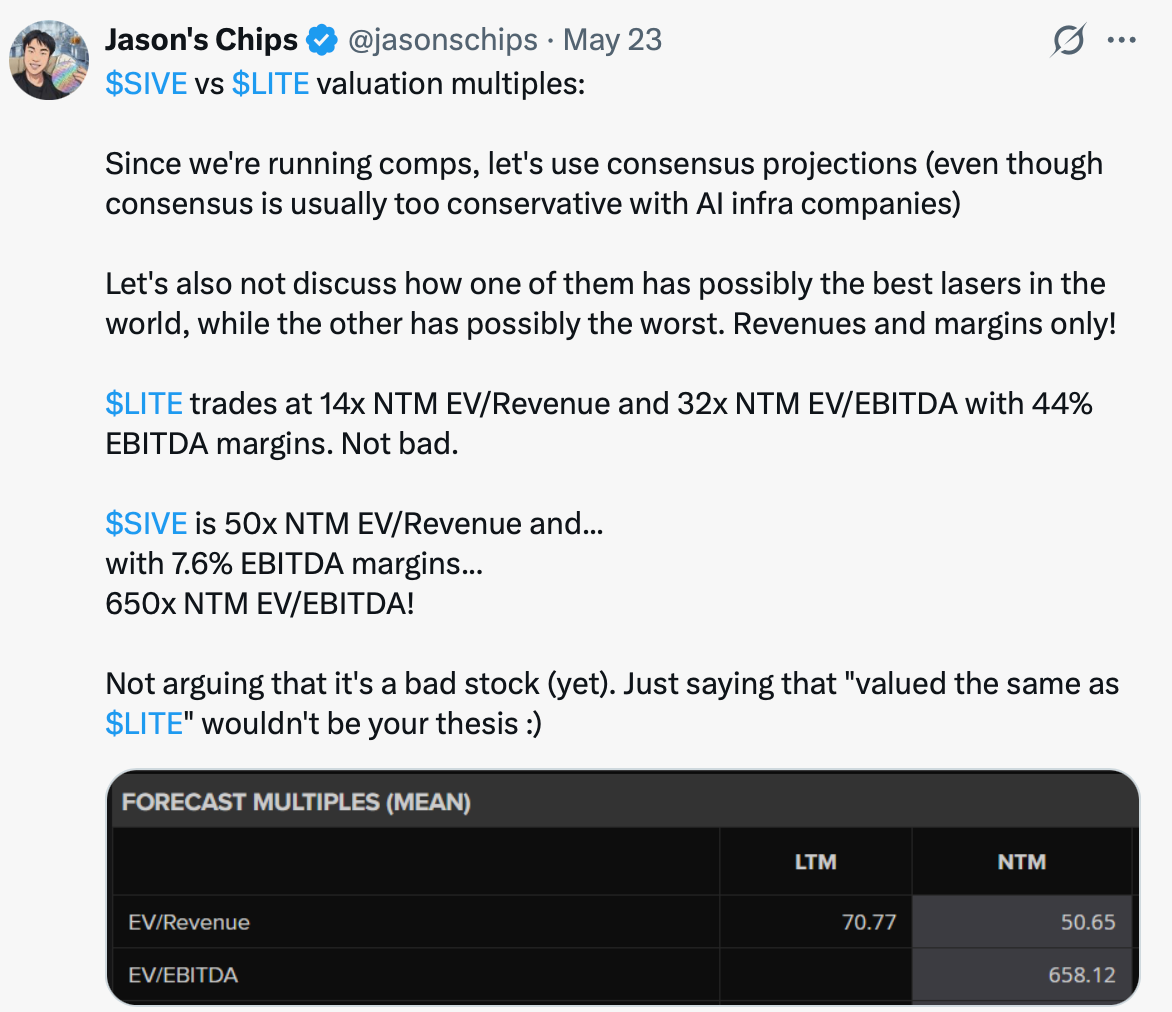

As you can imagine, if the stock is nearly 20x more expensive at a $2.3 billion valuation, the old thesis doesn’t work anymore.

This is not true for all companies. Some, like AXTI 0.00%↑ or SNDK 0.00%↑ , sell a raw material or commodity whose supply/demand scarcity dynamics have no natural ceiling. This means that one thesis (memory ASP go brr) can justify nearly any valuation.

But for other companies competing in the 10-bagger arena, the thesis must evolve as the valuation gets more stretched.

Sivers could rely on a simple CAGR back at $130 million. At $2.3 billion, they now trade at more than 230x their disclosed 2025 photonics revenue. Keep in mind that the photonic segment isn’t purely data center revenue, either. It also includes LIDAR, and they do not break down sub-segment granularity, so in reality, the actual multiple is higher. I am also only able to use trailing multiples, as the company has not disclosed a single DC photonics volume purchase order or given any DC photonics revenue guidance. They are basically a pre-qualification startup.

All management disclosed is their goal of compounding their revenue at 25 to 30% CAGR, expanding to 65% gross margin, reducing R&D to 20% of revenue, and having an EBITDA margin around 30%.

“Based on the cost structure and margin profile of the business, we would expect to reach cash flow breakeven at annual revenues of approximately $50 million-$55 million, and 65% of revenue stemming from products. This we are targeting in roughly two years’ time. Our long-term ambition is to sustain 25%-30% revenue CAGR, with fabless financial KPIs at around a 65% gross margin, R&D costs of around 20% of revenues, and an EBITDA margin around 30%. We are striving for world-class performance because we believe we have the technology to achieve it.”

This is no longer aggressive enough to save the stock.

Now, we have to evaluate whether there can be an order one or two order of magnitude step function growth from a sudden qualification breakthrough along with massive purchase orders (that can actually be manufactured with their current owned capacity and WIN allocation) that can even remotely justify the current valuation levels. This also means that Lidar and Wireless are pretty much irrelevant because the only segment that could be explosive enough to drive a fundamental breakthrough that justifies the current valuation is the massive CPO market. Other factors that people usually consider “bullish” like Chips Act funding (which is actually for their wireless segment for defense) and a Nasdaq listing (with like $16 million of inflows or something) also, don’t really matter at a $2.5 billion market cap.

If photonics breaks, the entire story breaks too.

Sivers 101: Opportunity Pipeline & NRE

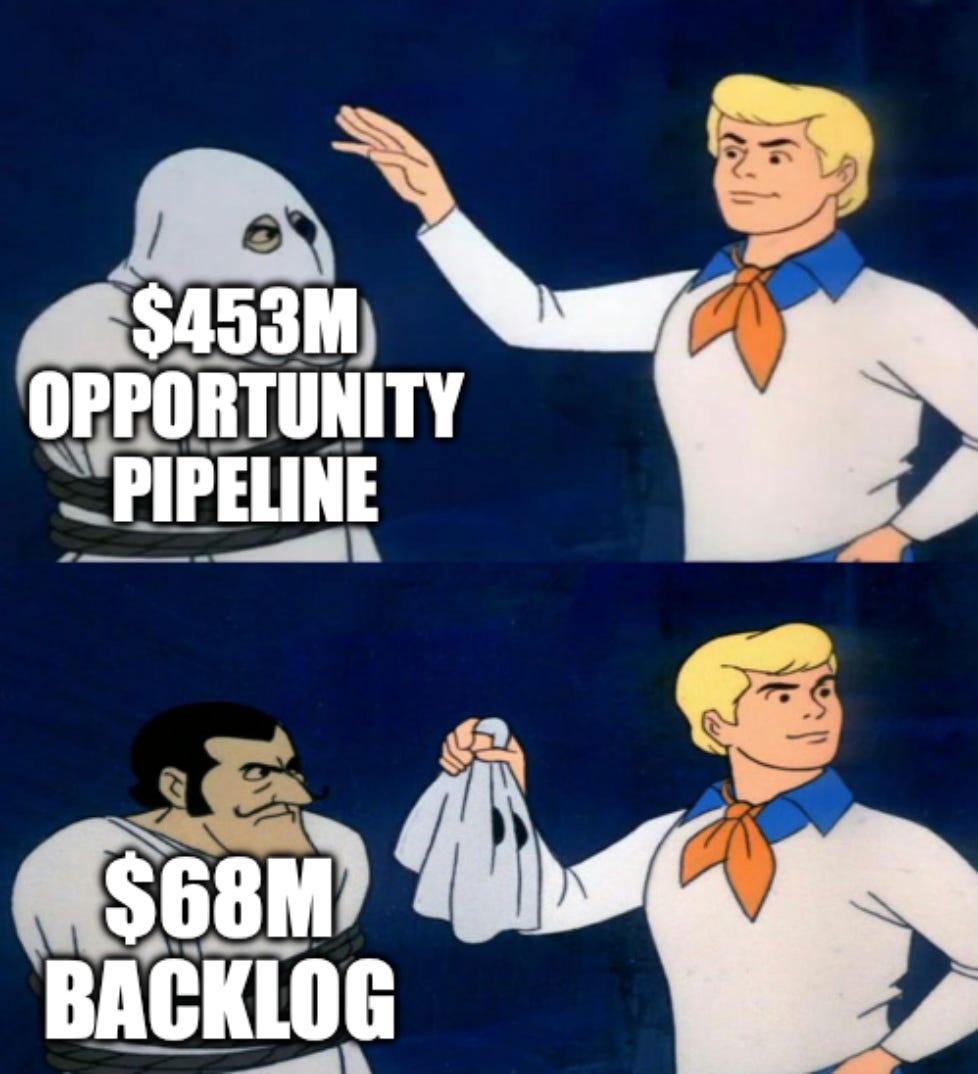

Every earnings call, Sivers presents a KPI known as their Opportunity Pipeline. Their Opportunity Pipeline right now is $453 million, which is up 64% in 2025.

It sounds really big and cool because it takes the place of a number of other companies’ reports, which is very important: the backlog. However, the opportunity pipeline is not a backlog at all, not even close, and treating it as a backlog is extremely misleading.

The Opportunity Pipeline is literally everyone that they’re talking to. If they’re having a conversation, it’s part of their Opportunity Pipeline. For it to actually convert into contracted backlog, they need to move into evaluation and sampling, which is still very far away. Then get a design win and finally make it to production orders. I’ve never seen any other company in the world report the numbers this way. It makes it extremely inflated.

In my estimation, only about 10 to 20% of the Opportunity Pipeline actually converts to backlog. Which is around $68 million of their $453 million opportunity pipeline.

I started from the idea that the $453m opportunity pipeline is a five-year, non-binding funnel, not a one-year order book. If all of that were close to backlog, Sivers would already have several years of contracted revenue sitting behind a company that only did about SEK 306m / ~$30m of revenue in 2025. That does not fit the disclosures: contract liabilities were only SEK 11.6m, management says the pipeline is non-binding, and much of Photonics is still sampling/qualification. So the true committed layer has to be much smaller than the headline pipeline.

Then I sanity-checked it from the other direction: Sivers still needs enough near-term committed or near-committed work to support 2026 revenue around SEK 360-376m, plus named programs like CHIPS, Tachyon, Doosan, ALL.SPACE, LiDAR, and FWA. That gets you to a few hundred million SEK of credible revenue-converting opportunity, but not billions. Converting that into pipeline percentage: 10% of $453m is ~$45m, 15% is ~$68m, and 20% is ~$91m. That range maps to roughly 1.5-3.0x FY2025 revenue, which feels plausible for a mix of signed work, near-term NRE, product orders, and late-stage customer forecasts. Above 20-30%, the implied committed revenue starts looking too large versus what they actually disclose. Hence my practical estimate: 12-20%, with ~15% as the center.

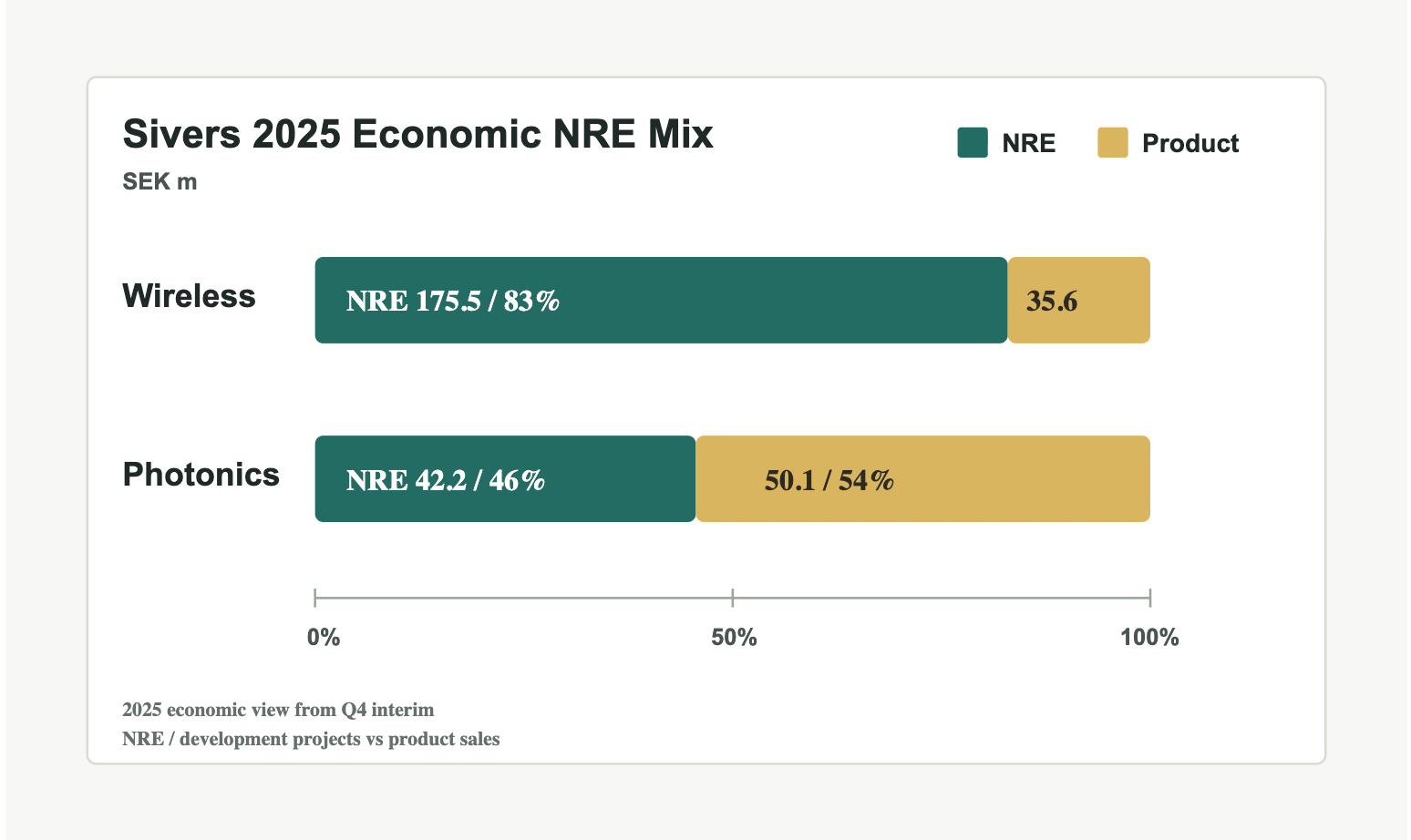

The next Sivers term we need to discuss is NRE.

NRE means Non-Recurring Engineering Revenue. This is customer-funded R&D. The customer pays you to do R&D, and you book revenue. That’s basically what they do to get ciphers to customize their IP to the customer’s needs.

Now, most of their revenue is NRE, both wireless and photonics. That means they’re pretty much a startup at this point. This isn’t product revenue, and it’s not sustainable. Honestly, this would be a bear point at a much lower valuation, but at a valuation this high, this doesn’t even matter. They’re essentially a very frothy VC startup at this point, so NRE or not, what actually matters is if the product revenue can 100x with some massive qualification. Who cares if the tiny revenue base isn’t sustainable? That’s not what is making it a multi-billion dollar company anyways.

The (Fabricated) Bull Case

The few individuals who pump this stock focus on two main things.

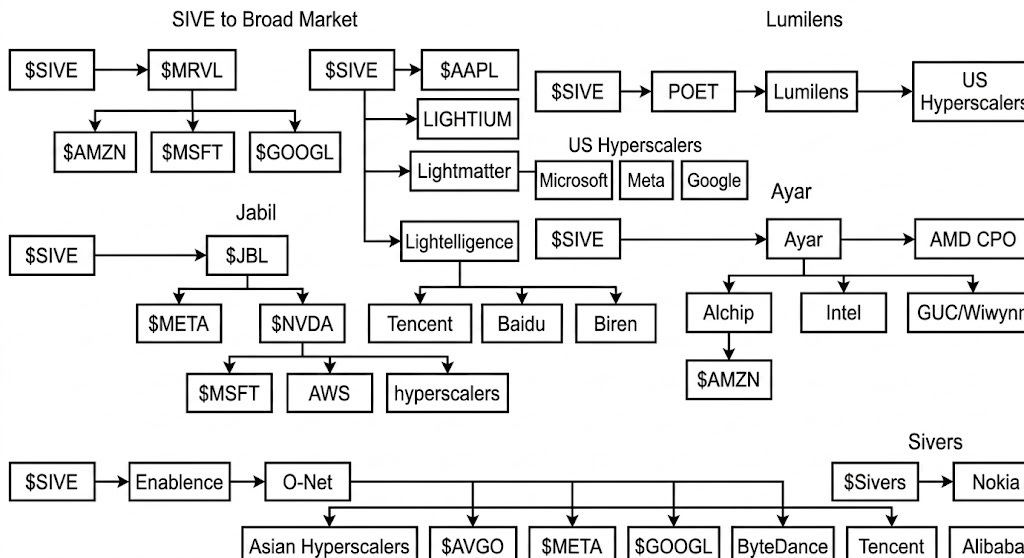

This picture expresses the first one.

Basically, “omg $SIVE is in conversation with Ayar, Poet, LightMatter, and Optical Startup #463 and the ex-director-of-shits-and-giggles of one of these startups once had dinner with Matt Garman’s guinea pig, which means that they are supplying lasers to every single hyperscaler. $SIVE to the fucking moon”

This is completely and utterly wrong because, as I talked about before in the backlog section, conversations don’t mean shit without qualification and production orders. It’s not the hard part. It’s not what’s valuable. I don’t give a shit who supplies what to whom. If the product is uncompetitive, the buyer will find another supplier. If you have no customers, build a great product and the customers will come. What’s valuable is having a good product that passes qualification and performs well and then having the manufacturing expertise to ramp it at high yields and high gross margins. I can write a cold email and say I’m in conversations with Ayar Labs tomorrow if I wanted to. And not only that, the architecture of that startup has to actually be viable too (looking at you POET why do you even think you can beat hybrid bonding).

The second is possibly worse, which is that Sivers is a “chokepoint” or “bottleneck.”

(And no, a chokepoint is not different from a bottleneck. They’re the same thing.)

Sivers is literally the opposite of a bottleneck. They’re a fabless startup that people are calling a bottleneck.

Sivers hasn’t qualified anywhere. They are not choking off anyone. It’s like saying that the bottleneck for AI inference is Cerebras (lmfao). To find the real bottleneck for inference, you must look at who has majority share (Nvidia), then who owns the hard assets behind that majority share (memory and TSMC N3). The equivalent for optics here is Lumentum and AXTI.

A bottleneck must have both hard physical assets and substantial majority market share. Sivers has neither.

Why Is Sivers Fabless?

Today, Sivers is a fabless company. They have a facility in Glasgow which produces pilot volumes for R&D purposes, but in order to scale up to production volumes, they have WIN Semi as their contract manufacturer.

However, it wasn’t always this way. Turns out that in the past, Glasgow was pitched as a fab that could do up to $150 million in revenue. Yes, that is something around ten times their current photonics revenue base. It was only around the end of 2024 to the beginning of 2025 where this changed.

What happened? My best guess is yield.

Making lasers is really fucking hard. InP is brittle. Aixtron’s management said that Lumentum is their best customer in terms of their ability to use MOCVD machines to make lasers and even the best player out there only achieves 50% yields (on EML). That means one in every two dies is binned!

Manufacturing is brutal. Manufacturing is the moat, and that moat is what kept Sivers out of making their own lasers. That means that what they have left, which is just design IP, is a lot less valuable.

There is No Moat

Technology analysis will always be superior to supply chain analysis.

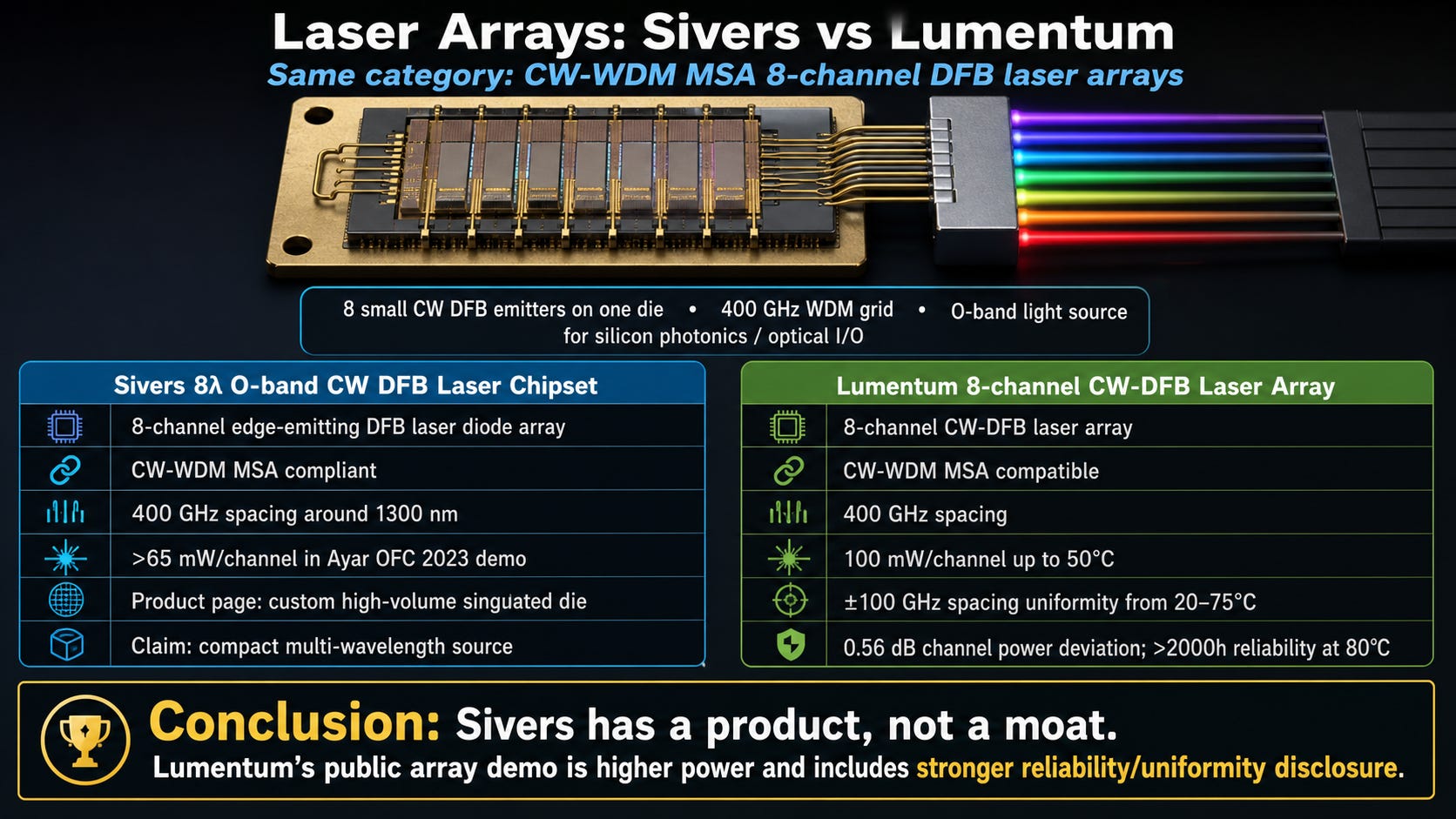

Here’s where I want to introduce you to a surprise. Sivers has no moat. Turns out that Lumentum also makes these laser arrays, and in fact Lumentum’s specs are even better, offering up to 100 mW per channel at 50°C, way higher than Sivers’ 65 mW per channel (with unspecified temperature).

As in classic Lumentum style, they also disclose way more other specs like spacing uniformity, channel power deviation, and reliability results. They literally do it better in every way.

This leads us to two main conclusions:

Laser arrays are not proprietary to Sivers. They don’t have a moat here that makes them better at making this specific technology.

Regular ultra-high power 400 mW lasers that send one powerful beam of light and split it, instead of using WDM and an array of lasers, are the superior default architecture.

The Wrong Architecture

Let’s zero in on the second one a bit further.

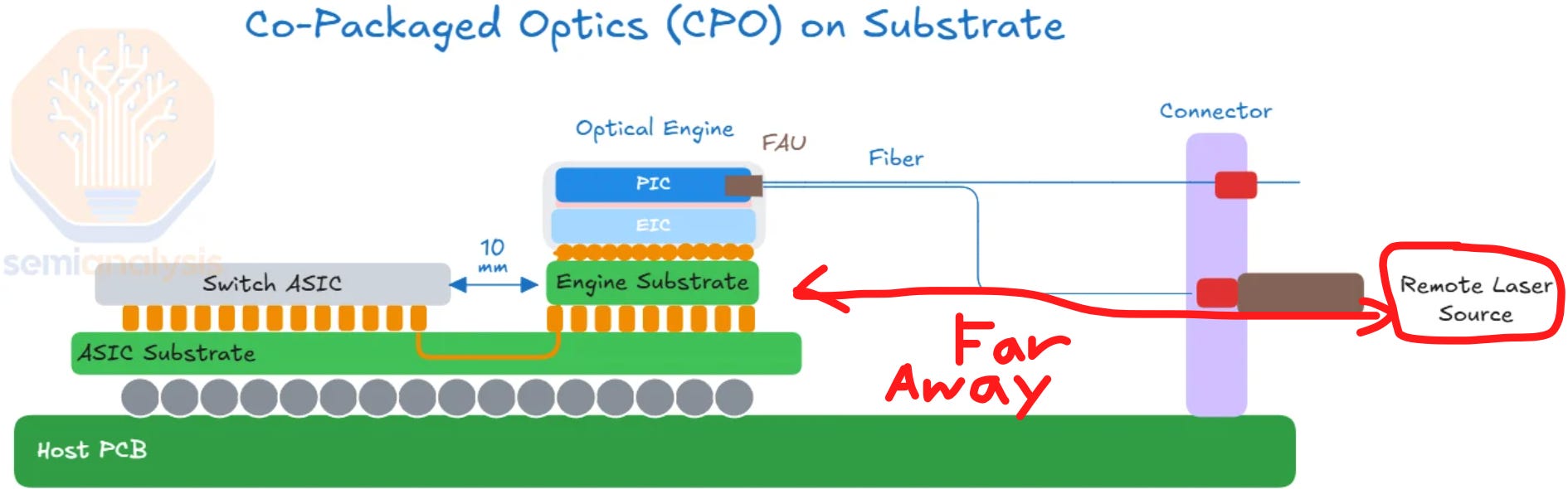

Lasers for CPO must also be placed far away from the optical engine.

Because this laser is so far away, in order for the light to reach the optical engine, it needs to survive a lot of coupling loss meaning that the light gets much less powerful every time it has to go through fiber and whatnot.

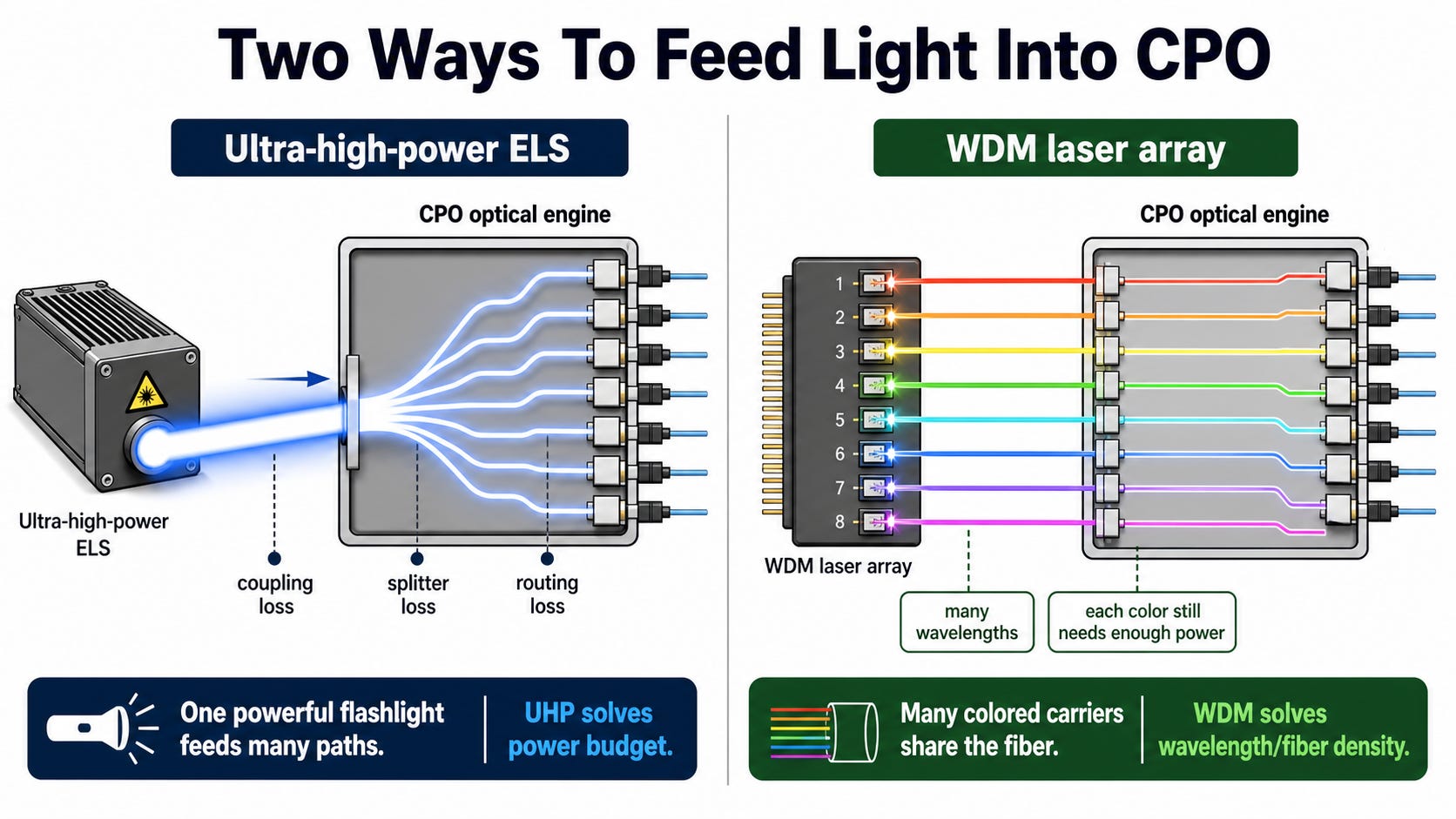

There are two ways to feed light into a CPO system.

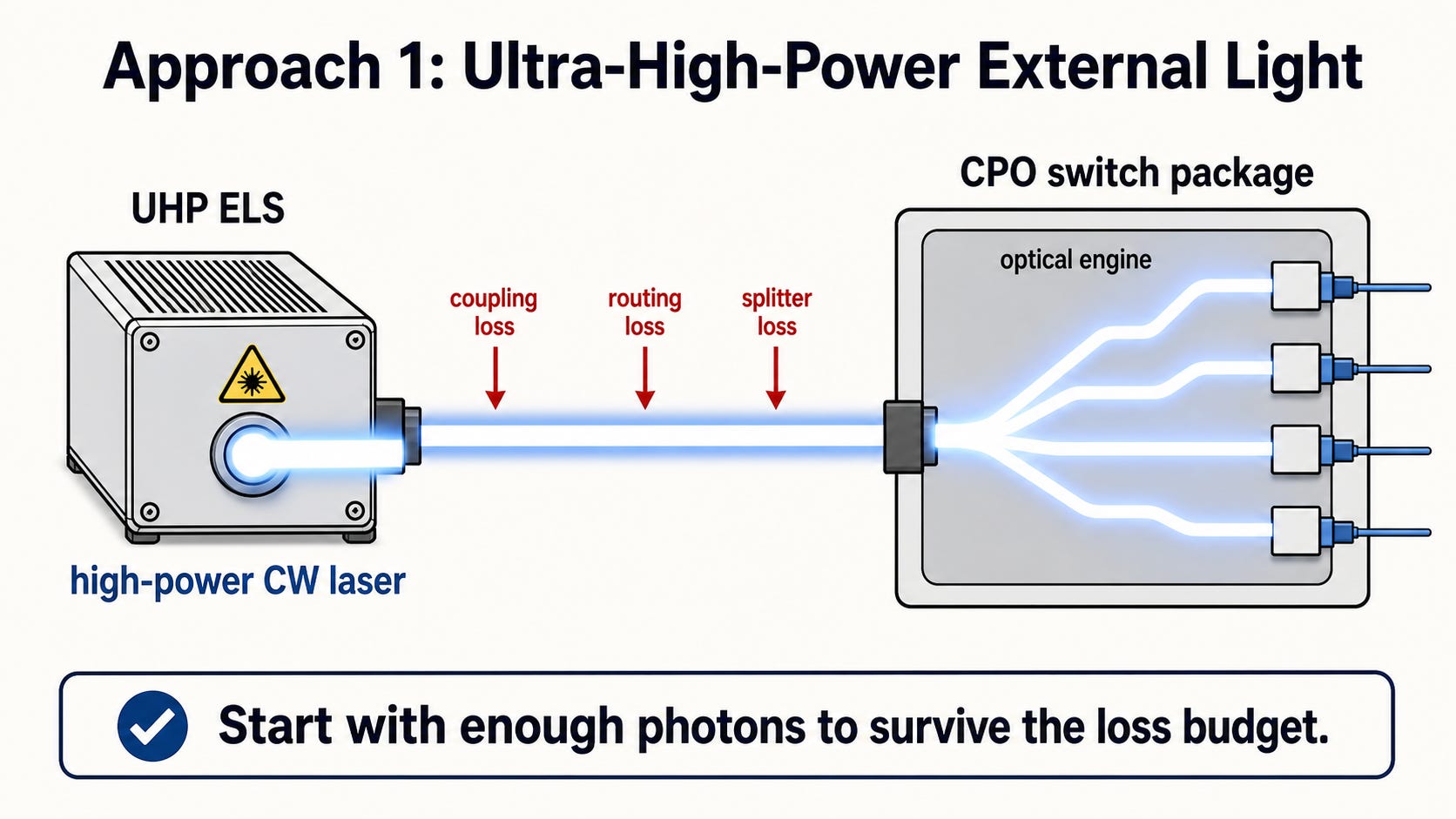

The first is the ultra-high-power approach. You start with one very powerful continuous-wave laser outside the optical engine. That light enters the CPO package, survives the coupling loss, and then gets split into multiple lanes. This is the Lumentum-style architecture. The whole point is simple: start with so much clean light that even after losses and splitting, each lane still has enough photons to carry data.

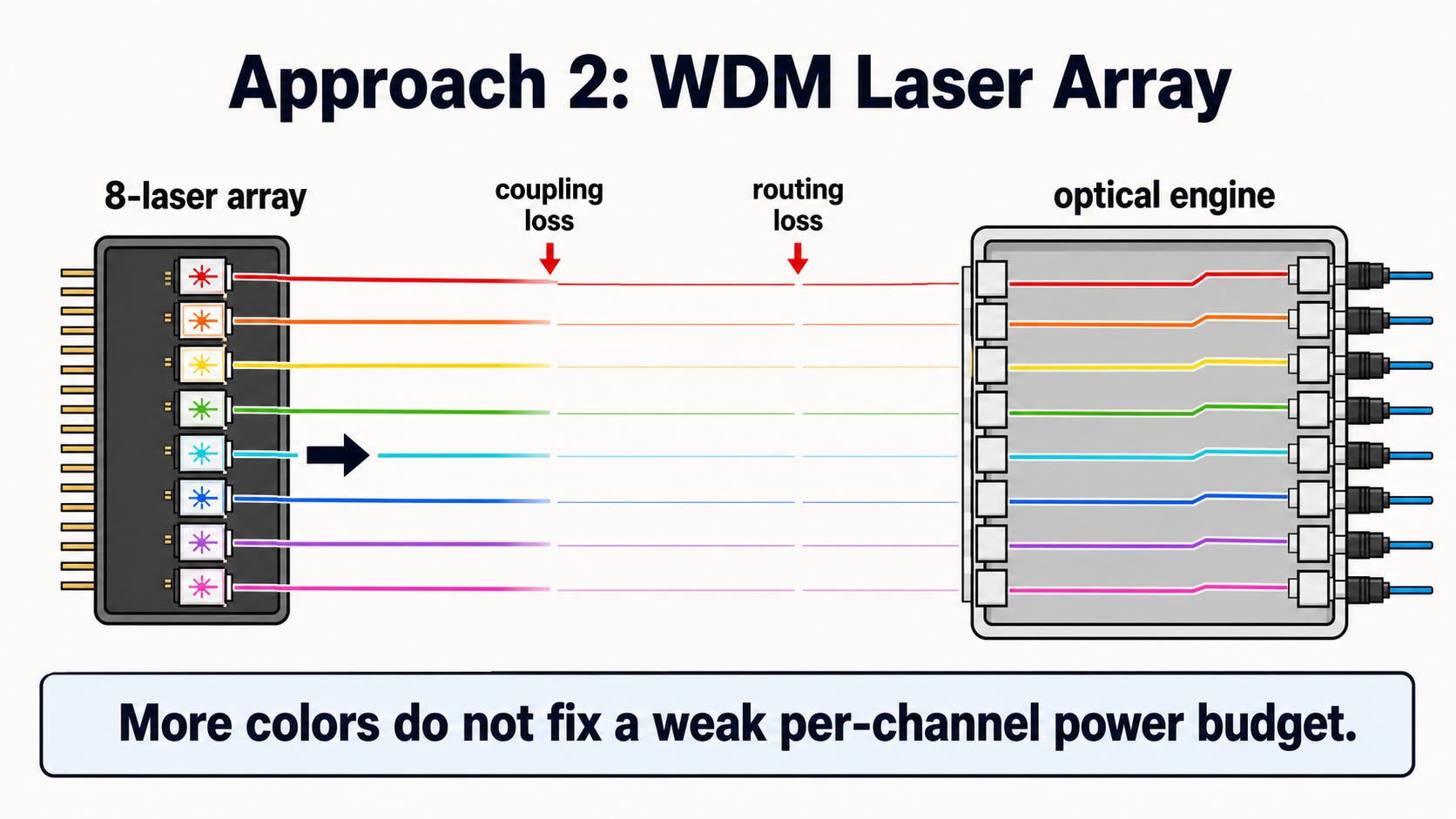

The second approach is WDM, or wavelength division multiplexing. WDM just means using different colors of light. Instead of one very powerful laser, you use a laser array: many small lasers on one chip, each at a different wavelength. One color carries one data stream, another color carries another data stream, and so on. This is what Sivers is pitching.

WDM is a real and useful optical technique. But it solves the wrong problem for our beloved CPO application.

WDM solves a bandwidth density problem. It lets you push more data through fewer paths by stacking multiple colors together (and each data stream is one color).

UHP solves a more important problem: giving you way more starting photons.

CPO does not care about multiple colors. It fails if the light is too weak by the time it reaches the optical engine. Every connector, fiber attach, splitter, coupler, and waveguide eats optical power. If the source starts weak, adding more colors does not fix that. You just have many weak colors instead of one usable color.

In addition, Lumentum’s regular UHP architecture does not need WDM to push enough data. It can scale bandwidth through spatial parallelism: more lanes, more fibers, more waveguides, more parallel optical paths. That may be less elegant than WDM on paper, but it focuses on the one thing customers actually need first: actually having photons per lane after all that coupling loss.

WDM adds its own complexity. You need wavelength locking, thermal control, filters, tighter testing, more channel matching, and more ways for one bad channel to ruin the package. In CPO, the binding constraint appears to be optical power, reliability, and qualification.

So the conclusion is very clear!

Use many smaller lasers with different colors < < < Use much stronger lasers and split the light.

And this isn’t a Lumentum vs. Sivers thing where Lumentum wins the market with their architecture. It is that Lumentum has both architectures. They’re the leader in ultra-high power CW, and they’re also the leader in WDM laser arrays, but look at what they chose to ramp for production volume. What is their Greensboro fab going to churn out? UHP CW lasers!

Sivers is in the right market, but it is targeting the wrong architecture. Laser arrays may be useful in R&D programs, lower-loss systems, or niche WDM architectures, but the default CPO production ramp is being built around ultra-high-power external light. That is where the volume is.

Conclusion

Let’s recap. Sivers used to be an undiscovered small cap with a respectable thesis, but after a 20x return facilitated by large social media accounts (unethically and illegally) promoting the ticker, the valuation has gotten absurd. The only way to save the stock is through its optical division gaining a foothold in the CPO market, which is much less likely than what the cult is hoping for.

The cult believes Sivers will gain a foothold because they are in conversations or have remote connections to hyperscalers through various optical startups. This is wrong because what actually matters is its technology, and it is precisely technology where Sivers falls apart.

Sivers is fabless because they lack the manufacturing expertise in the very difficult process of indium phosphide fabrication. Which means they lack a moat, as they are skipping the hard part to do the easy part.

Sivers owns no exclusive technology, as Lumentum makes the same exact laser arrays, but better.

And finally, but most importantly, Sivers is targeting the wrong architecture entirely. Lumentum has a choice between UHP and WDM, and they made a choice to ramp the exact thing that is the opposite of what Sivers is doing, for volume production.

Sivers Semiconductor is the most overvalued stock in optics.

Glad you speak up

If you consider TSMC COUPE platform and modulator choice, maybe you will realize ultra high power ELS is only good for switch and scale out or scale across. For ultimate package level or even rack level CPO, Ayar Labs approach using low power, multiple wavelength with microring modulator maybe the best one in future.