Situational Awareness (Leopold Aschenbrenner) 13F Analysis

A lesson on how options are reported and why they are mostly insignificant and meaningless.

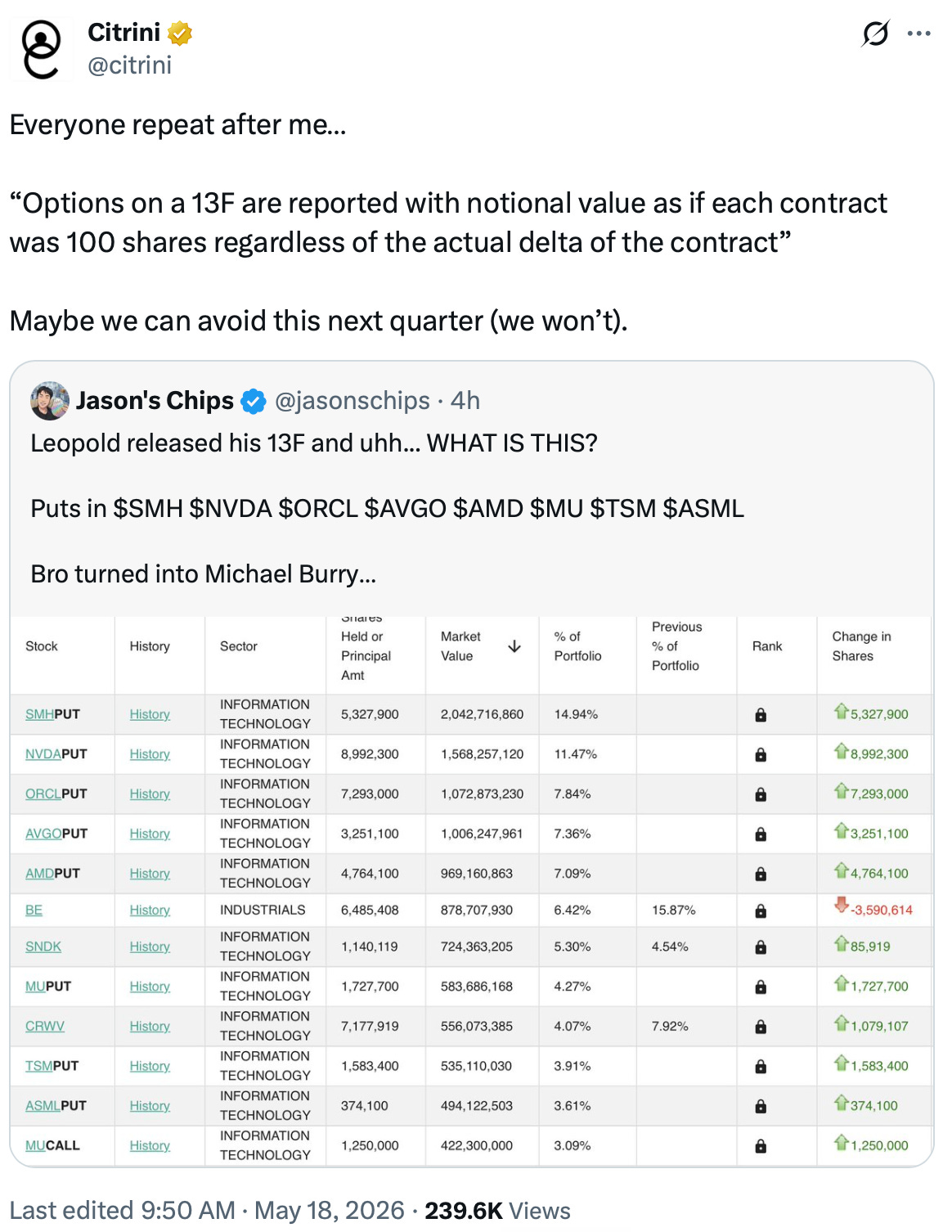

Leopold’s 13F caused a semiconductor sell-off. This Leopold sell-off has to be the most stupid sell-off in the history of all sell-offs.

His 13F showed a very scary amount of puts on literally every single large-cap semi company.

Yes, I am aware I played a part in the FUD. Citrus correctly called it out.

The lesson today is simple. OPTIONS ON 13-Fs ARE MISLEADING!!

How Options Are Reported on 13Fs

The market value row shown above is simple for shares, but not so simple for options.

For shares, it literally is just the market value at the end of the quarter.

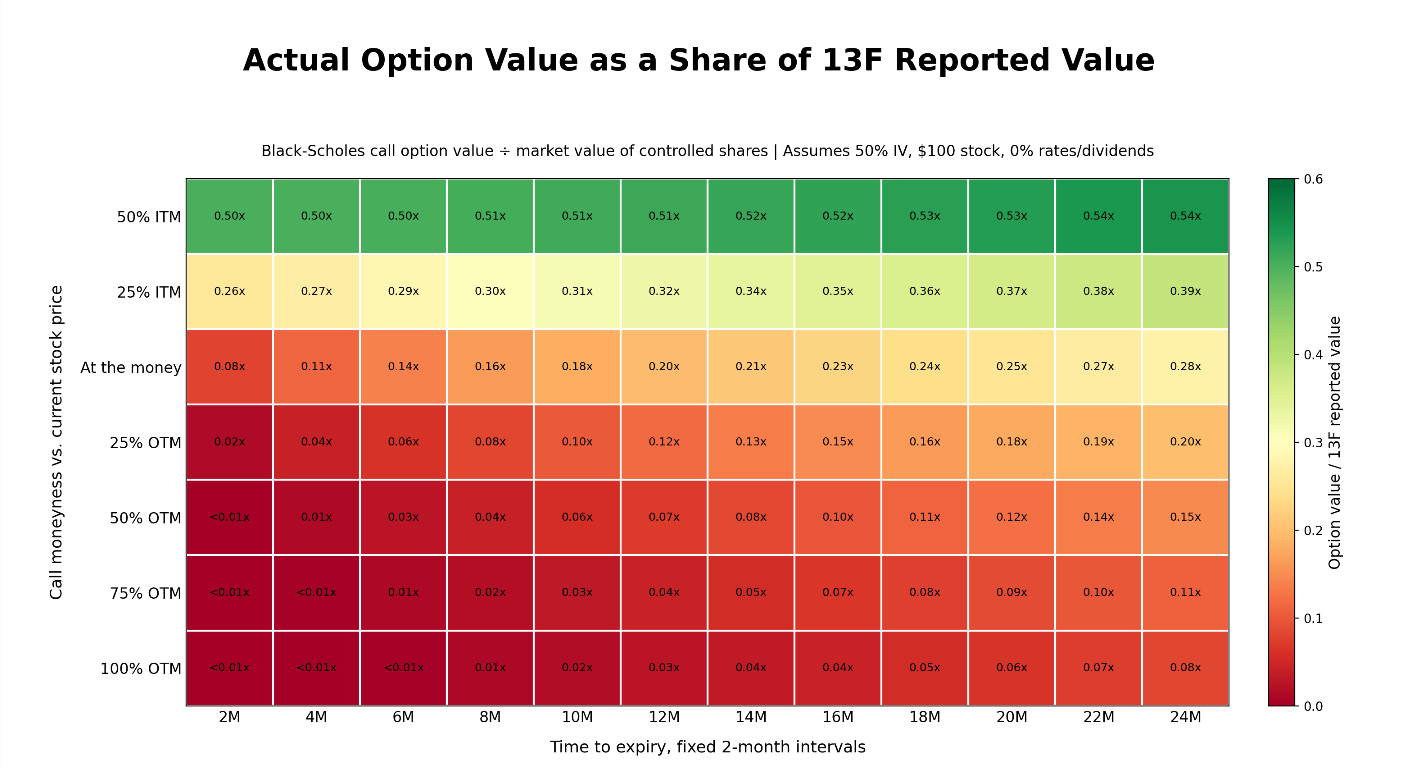

For options, however, it is not the value of the options. Instead, it is the market value of the shares controlled by the options.

This means that the actual market value of the options is way, way smaller than the market value shown on 13F. Plus, it is completely unknowable because we do not know the expiry date and moneyness (if it is in or out of the money and by how much) of the option. These are important because the closer the expiry, the lower the market value of the option relative to the shares it controls. The more out of the money the option is, the lower the market value of the option relative to the shares it controls.

This visual really hits home. There are two main takeaways that we need to have here:

The option value is guaranteed to be very low compared to the reported value on the 13F. In many cases, it is near zero.

The uncertainty is massive. Near-term out-of-the-money options have pretty much zero market value compared to the shares they control (i.e. you can control 100 or 1,000 times your capital in shares) why long-term in-the-money options can reach 1/3 to 1/2 the value of the shares. It is an order of magnitude of uncertainty. The market value therefore is incredibly low signal.

There is a very large chance that these were one- or two-month out OTM puts to hedge Iran, in which case they are like 3% of what the 13F says they are.

Leopold’s Real 13F

So, how should we read 13Fs?

STRIP OUT ALL OF THE OPTIONS. SHARES ONLY. ONLY SHARES.

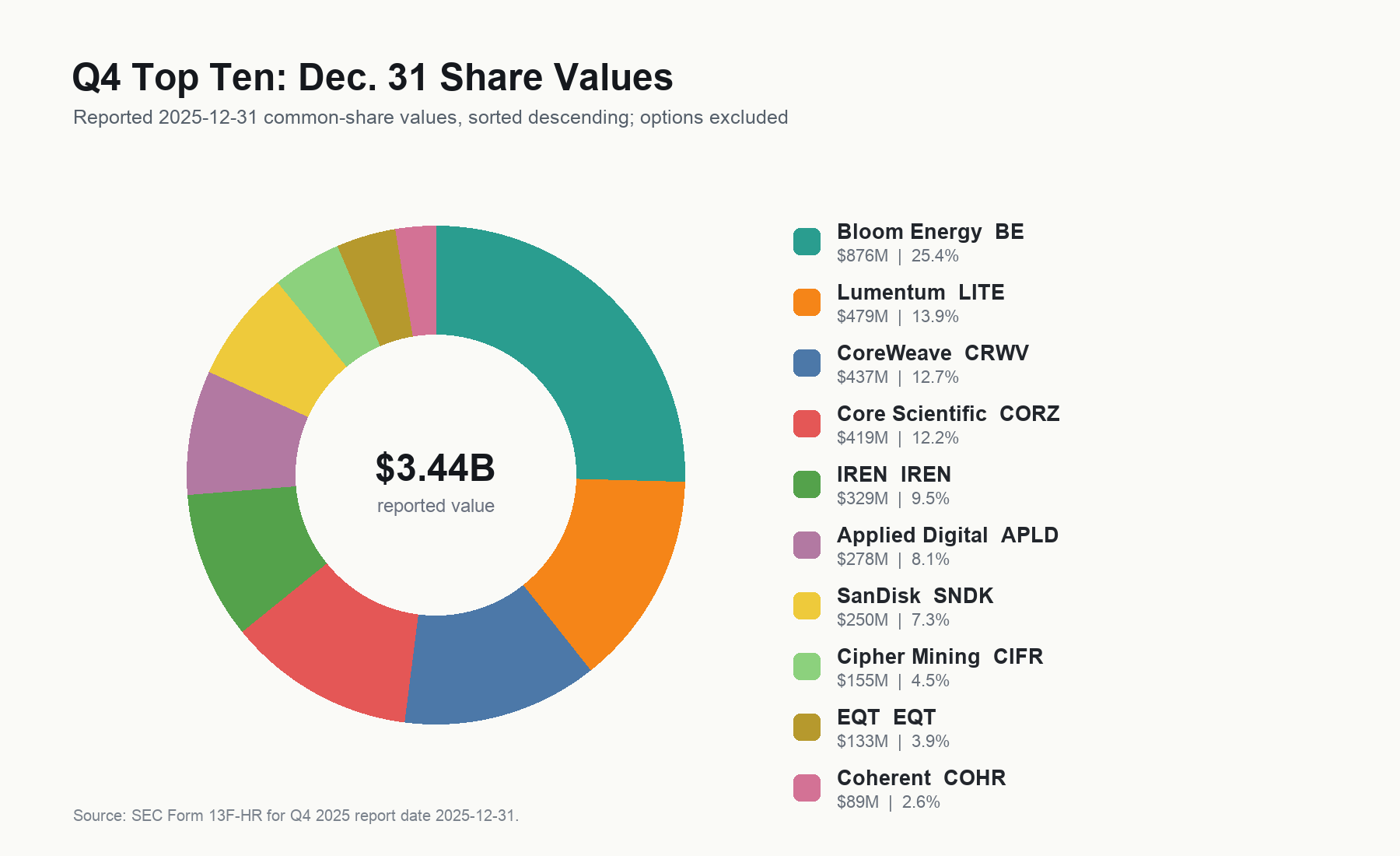

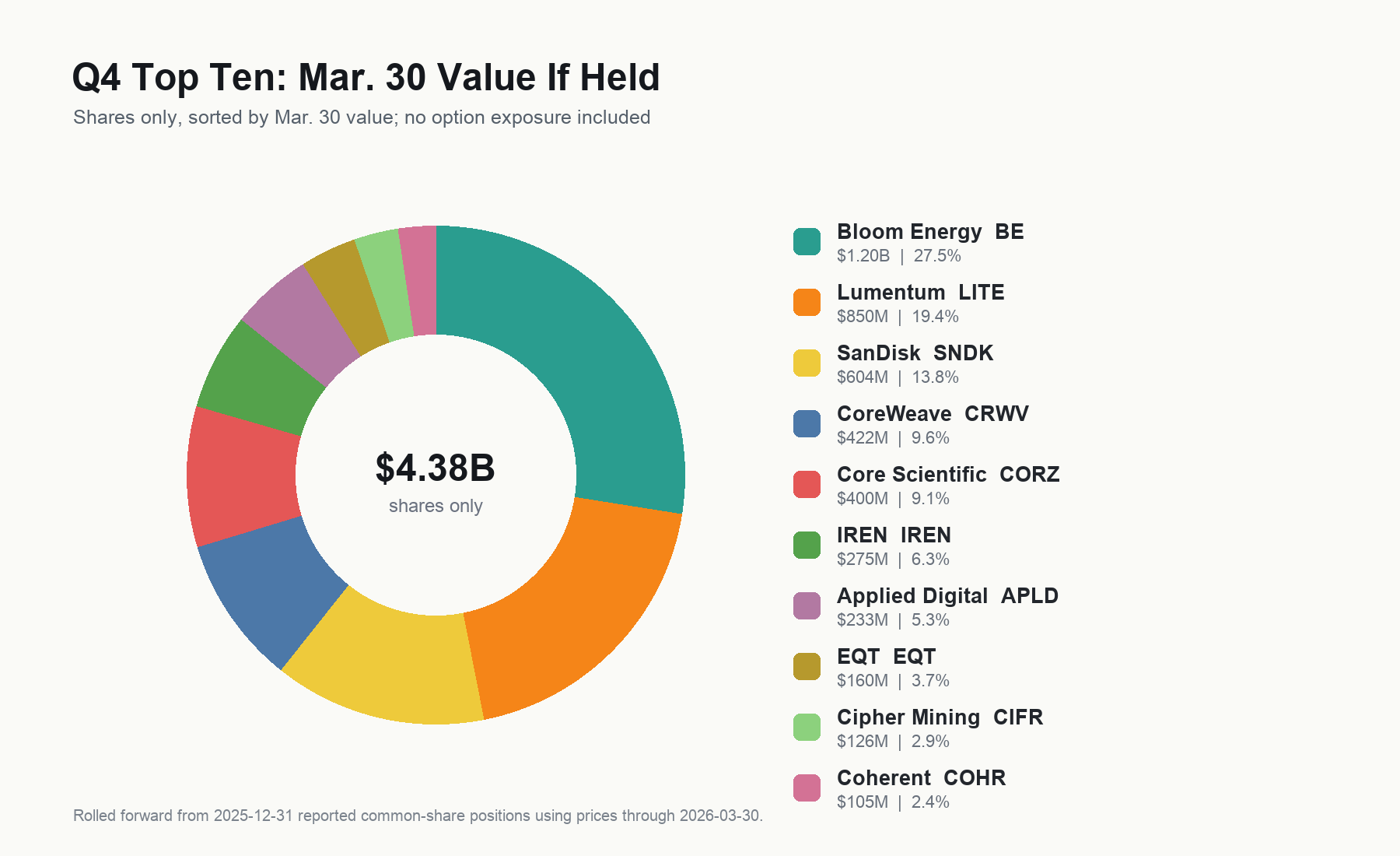

Here was Leopold’s 13F from last quarter. Meaning what he owned on December 31 2025.

As you can see, this is basically your classic super concentrated thematic equity portfolio. Bloom, Lumentum, and CoreWeave pretty much make up half of the portfolio. The rest make up the other half. This was that big Bloom bet that he took in the beginning of the year. Notice that we’re completely ignoring the Intel calls and the CoreWeave calls. They look optically very large in the December 13F, but again, we have no idea how large they are.

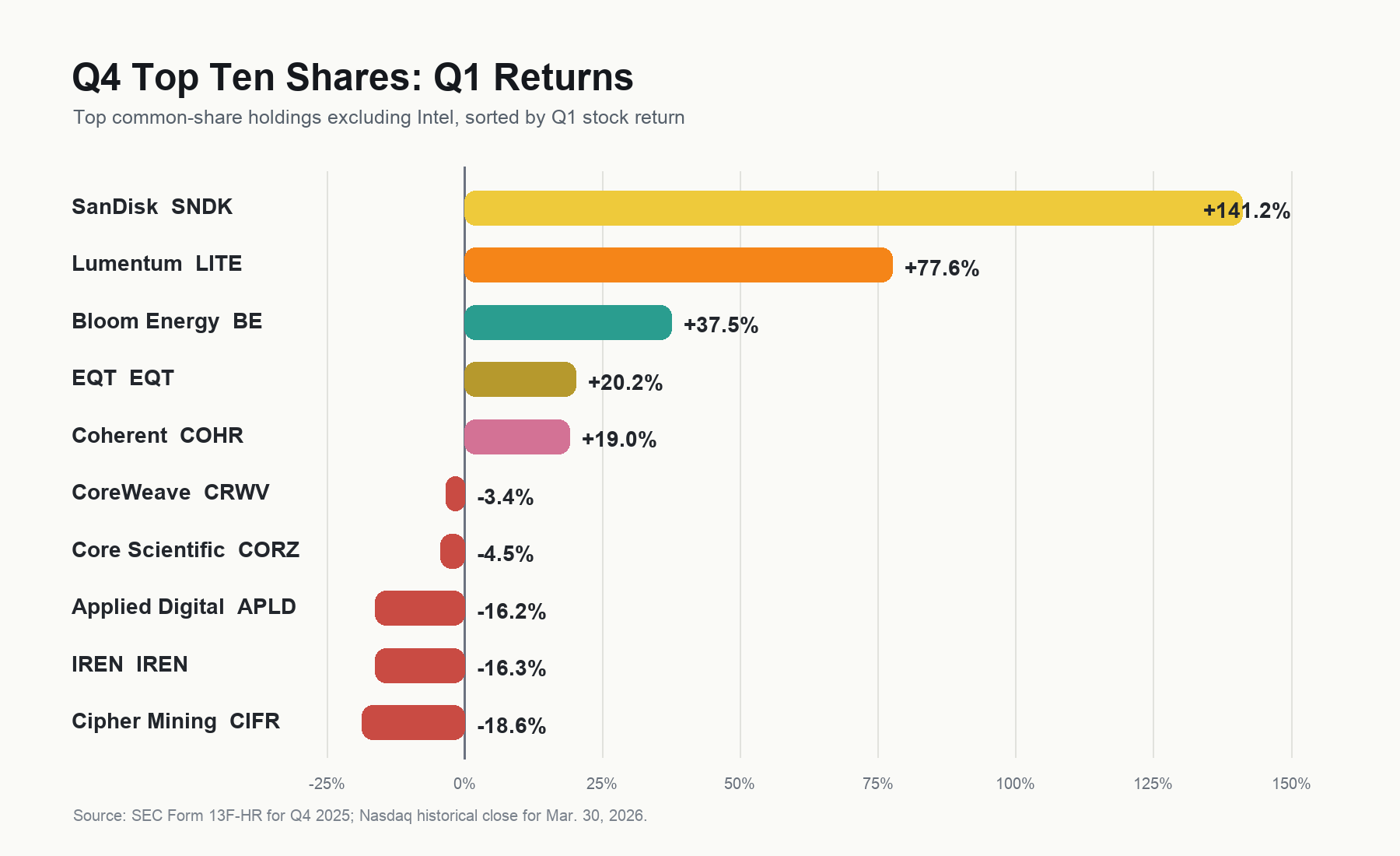

Here is how his holdings performed during Q1. As expected, Sandisk and Lumentum absolutely mog everyone else. The Neoclouds and miners are the laggards. Leopold has a pretty high affinity for the Neoclouds and miners and regularly adds to them, even through some rough performance over time. He gets his god-like status purely from his bets on the vertical chart crew (aka Sandisk, Lumentum, and Bloom). And honestly, that’s enough because I’ve never seen anybody successfully bet on all three. I am a Big Bloom Bull (BBB), but I came in late.

Here is his portfolio if he’d held the exact same equities through the entire quarter. His Q1 return would have been 27.3%. This is interesting because, despite a very large divergence in the performance, it looks relatively similar. At least everything outside of SanDisk. That’s really the only difference. SanDisk now takes up 14% of the portfolio, where before it was 7%. It is doubled in size. But of course, he partook in a common hedge fund activity known as “trading.”

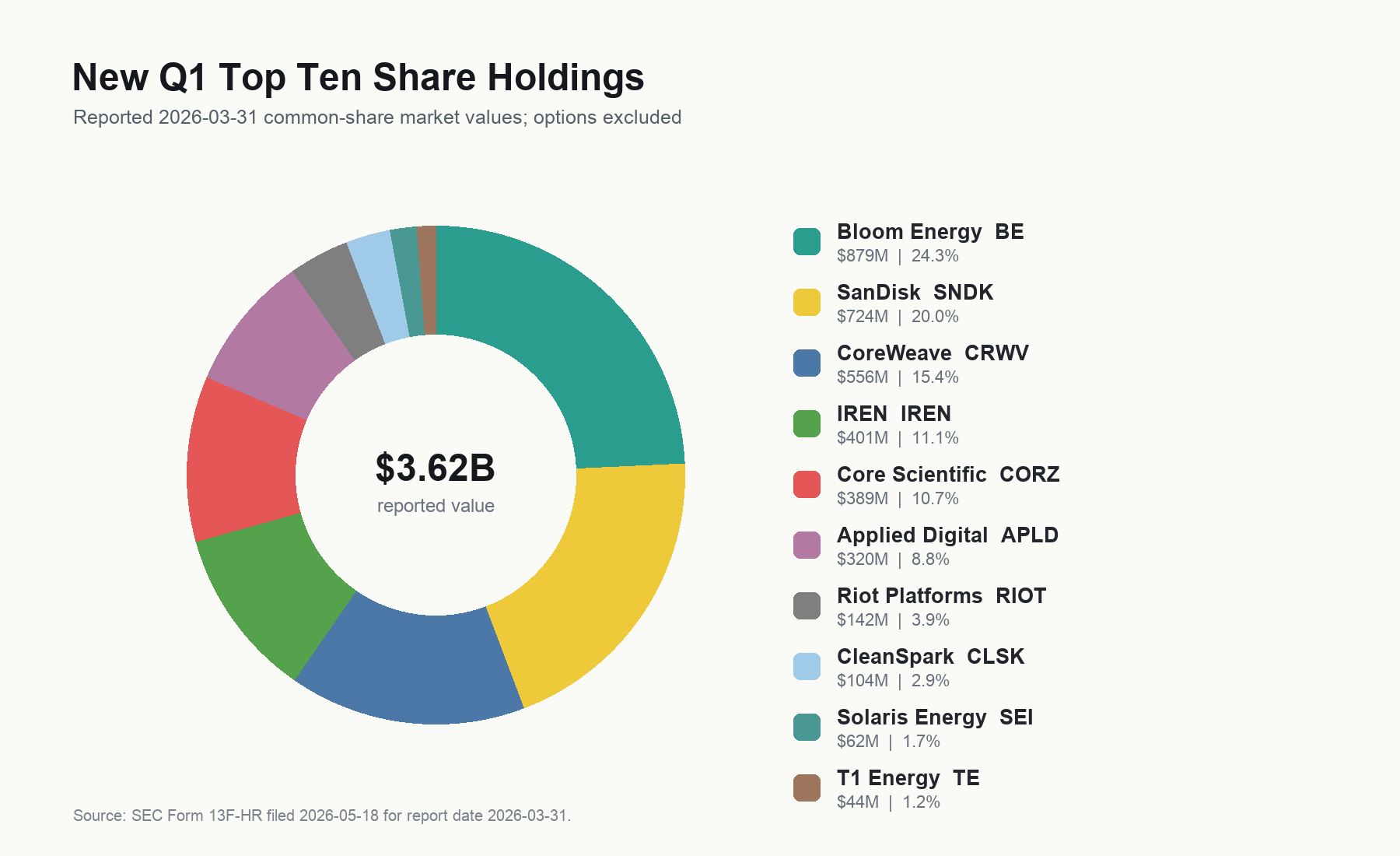

This is his new portfolio. Notice anything different?

First of all, it is only slightly (5%) larger than the Q4 portfolio.

Second of all, both Lumentum and Coherent are gone. Tower Semi, which weren’t in the top 10, are gone as well. Every single optics play was liquidated, and because this isn’t options, this is actual shares, this is real signal.

Third of all, because everything optics is gone, even though he reduced Bloom slightly by around 20%, it still makes up around a quarter of the portfolio (bc shares appreciated). His relative conviction on Bloom hasn’t really changed. The similar thing can be said for Core Scientific: reduced very slightly, but now actually makes up a larger portion of the portfolio.

Continuing on this train of thought, anything kept or slightly added to actually now takes up a larger portion of his portfolio. This includes CoreWeave, IREN, and Applied Digital.

However, the standout here is SanDisk. Not only did it appreciate materially more than the others, but he also added to it through the quarter. It is now his second-largest position, right between CoreWeave and Bloom Energy.

Below the paywall, I will attempt to read the mind of Leopold and tell you what he is thinking. I think I have read the original Situational Awareness essay like five times, and I followed every single 13F since Q2 2025, soooo I think I’m pretty qualified.

Contents

Optics Exit

Bitcoin Miners

NAND

Energy