Nvidia Earnings Review Q1 FY27

New Reporting, Compute vs. Networking, Neoclouds, Growth Rate vs Hyperscaler Capex, Frontier Labs share, CPUs, Supply Commitments, Capital Returns, Groq LPX, VR Ramp

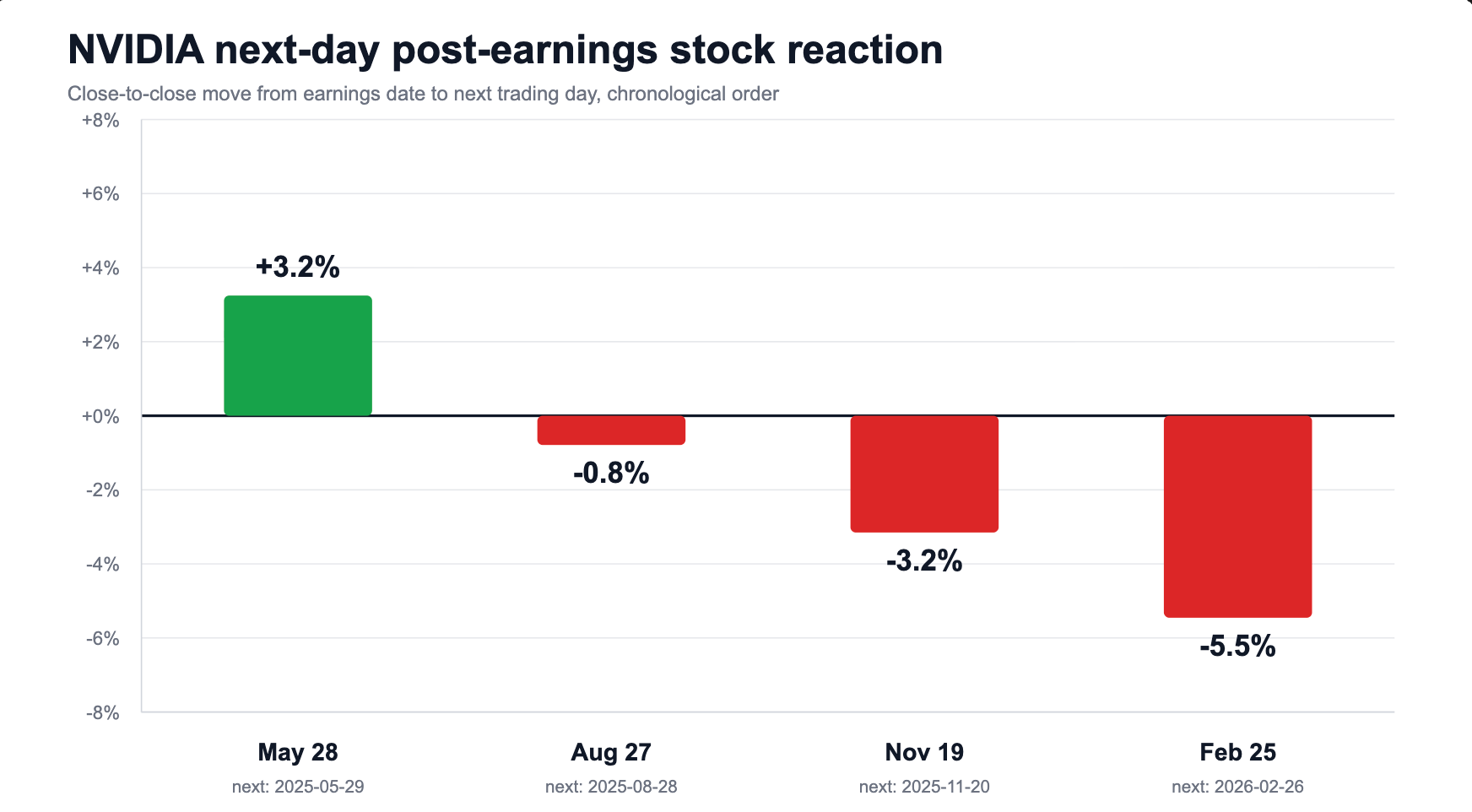

Another quarter, another NVIDIA earnings. Recently NVIDIA Day has been a lot less hyped and people are generally getting less and less excited about this event over time. Haven’t really heard the usual buzz on X today. Based on this visual, can you guess why?

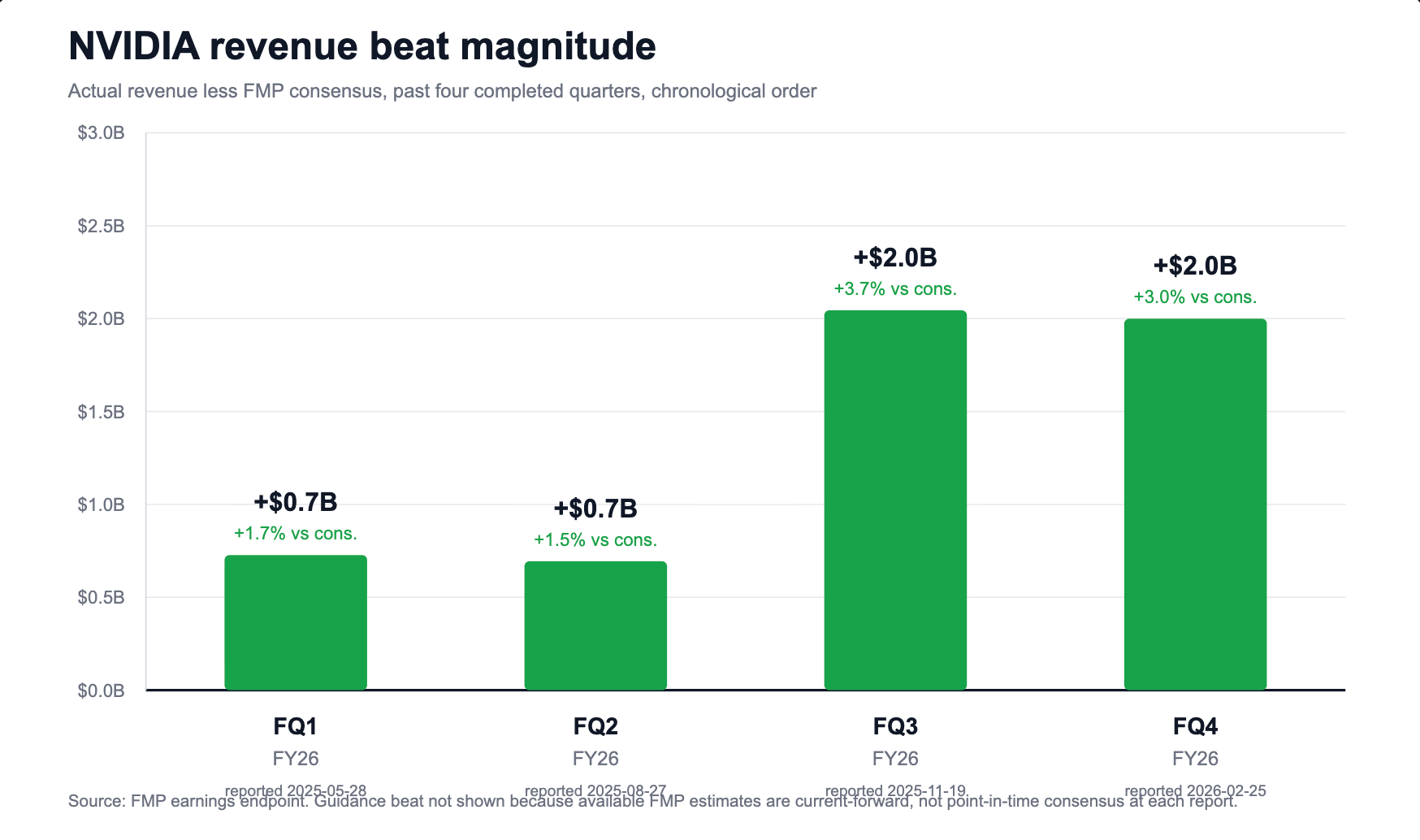

This is despite an increasing magnitude of their beats over time, and probably is frustrating Jensen right now.

We will see if today breaks the pattern!

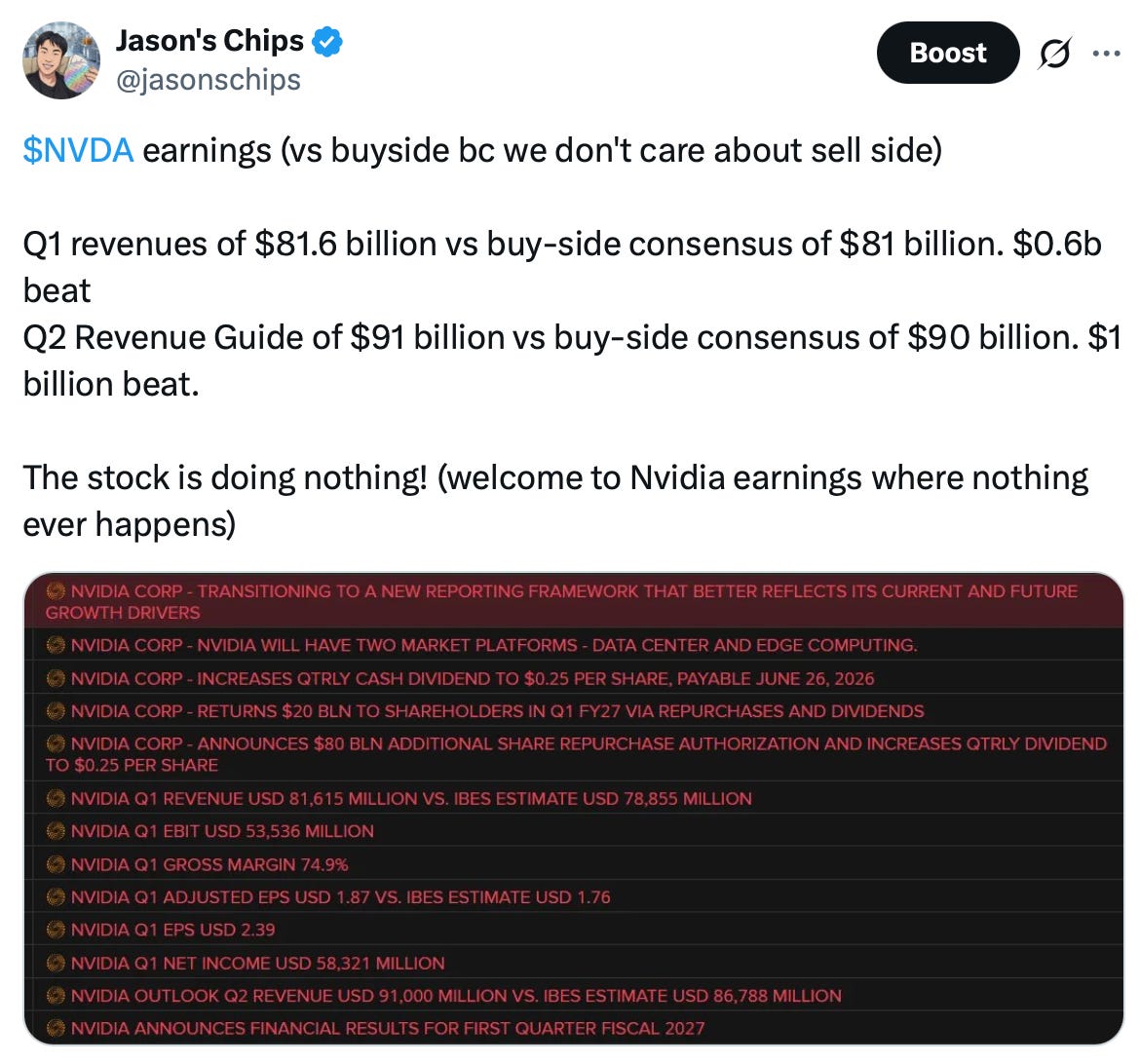

Here’s today’s Buy Side Consensus and Street Consensus courtesy of Jukan on X.

Same pattern as always: they guide for $78 billion, which means that they will probably beat by $2-3 billion due to historical conservatism, Sell Side models just above their guide because of Sell Side conservatism, and the stock probably dumps and takes down the whole AI infra ecosystem along with it unless they meaningfully exceed even buy-side consensus.

In terms of their rev guide, buy-side expects $90 billion. That’s a lot.

Gross margin expectation is 75% as always, and I bet it’s going to come out at 75% as always.

The Print

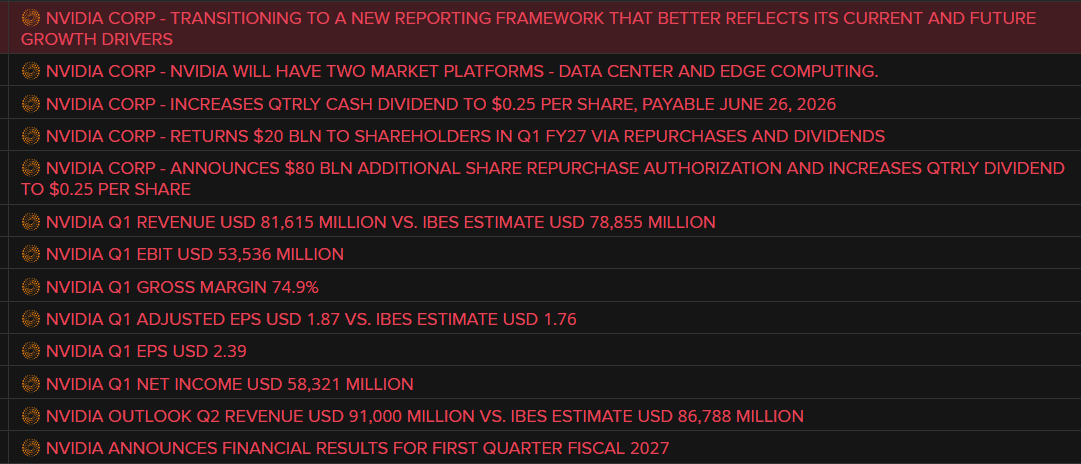

My initial reaction was WOW. $1 billion above buy-side on the guide and almost $1 billion above buy-side on the current quarter revenue. But then I realized it was only a $1 billion beat. Which means… nothing really happened.

The price action is really funny. We went down 3%, then flat, then up 2%, and now we’re flat again.

Two other pieces of information that were reported in the print (and we don’t have to wait until the call for closing parentheses) are:

Nvidia said that they have not generated any revenue under their H200 program and do not know if any imports will be allowed into China (by China) at all.

They said that Rubin is not delayed to counter all the Twitter rumors lol.

IMO, the real signal can only come from the call today. There’s a reason that nothing really interesting happens with the numbers ever, because Nvidia’s numbers are mostly a lagging indicator of AI hardware procurement. They’re also easy to estimate because Nvidia is so big. The market would rather look forward.

There have been tons of rumors on Rubin being delayed by a quarter or two. There are a few speculations on why this is.

Competition especially, AMD has pressured Nvidia to start upping the specs of Rubin. For example:

Power from 1800 W to 2300 W

Memory bandwidth from 13 Tb/s to 22 Tb/s

Increasing the HBM4 requirements to over 11 Gbps per pin

The increased HBM4 requirements meant that the Big Three, the Big Memory Three, had to redesign their samples and resubmit.

There was also a claim that Nvidia had unresolved SerDes chip interface problems and was “dialing down specs” as a response.

And also heat-spreader redesign?

Anyways, Nvidia is probably going to get a lot of pressure from the sell-side analysts to explain what’s going on here, so we should learn a lot today.

I have never seen a post-earnings chart as perfectly flat as this one today. It’s so perfect and so flat, it’s funny. Probably won’t be the case after the call, though!

The Call

Contents

New Reporting

Compute vs. Networking

Neoclouds

Growth Rate vs Hyperscaler Capex

Frontier Labs share

CPUs

Other

Supply Commitments

Capital Returns

Groq LPX

VR Ramp