Nvidia | Earnings Review: No Hair on The Print

And the structural reason why Nvidia’s multiple will always trade range-bound

Opinions are my own and do not represent past, present, and/or future employers. All content is based on public information and independent research. This newsletter is not financial advice, and readers should always do their own research before investing in any security. I am invested in the semiconductor industry. As of the date of this publication, I may hold long or short positions in the securities discussed in this article.

Outline

Pre-Earnings Vibe Check

The Print

Price Action

The Call

No Hair On The Print

Absolute Dominance Over The Supply Chain

Very Positive Useful Life Commentary

Jensen Reasons In a Way That is Very Different from the Finance People

There is No Way to Prove the Skeptics Wrong

Pre-Earnings Vibe Check

(This section was written prior to the earnings call to communicate the prevailing narratives and provide a contrast to post-earnings sentiment)

This preview will be very brief since I covered most of what’s happened this past quarter in State of Nvidia.

I’ve already covered the idiosyncrasies of this company. What I do want to get into briefly, however, is the macro picture. I think they are in such a strong competitive position any further improvements in Nvidia vs competitors won’t matter. The real valuation mover is Nvidia vs AI Bubble. It’s like finishing the PvP of a game while being stuck on PvE.

Nvidia trades at 15x 2027E EPS not because of the TPU, but because the market is afraid of a downcycle starting in 2028. Every other technology wave resulted in an overbuild, why is this different? Any way Nvidia can address this deep-seated concern will do a lot more than beating guide by $3b yet again.

What will calm these concerns and finally unshackle the stock? Long term growth visibility. How can they provide this? I don’t know. It’s not like the smaller supply chain players with their LTAs, Nvidia is literally the whole market. They are burdened with answering the AI bubble question.

The most compelling argument about a near-term overbuild is the fact that everything is in a shortage. Hyperscalers would spend more, but they simply can’t because there is not enough memory, power, and foundry capacity.

Other than that, I think you have the more traditional questions.

Amendments to the $500b “Jensen Math” backlog through YE2026 they had in October.

Rumors of SK hynix HBM4 issues delaying Rubin by a few quarters (vs mid-2026). True or false? Rubin Ultra shipping mid-2027?

Commentary on if the everything-constraint is affecting growth.

Networking growing faster than compute as a leading indicator of demand.

Is gross margin holding up during the blackwell ramp?

What ever in the world is going on with China.

Anything product related is probably saved for GTC.

Earnings Estimates

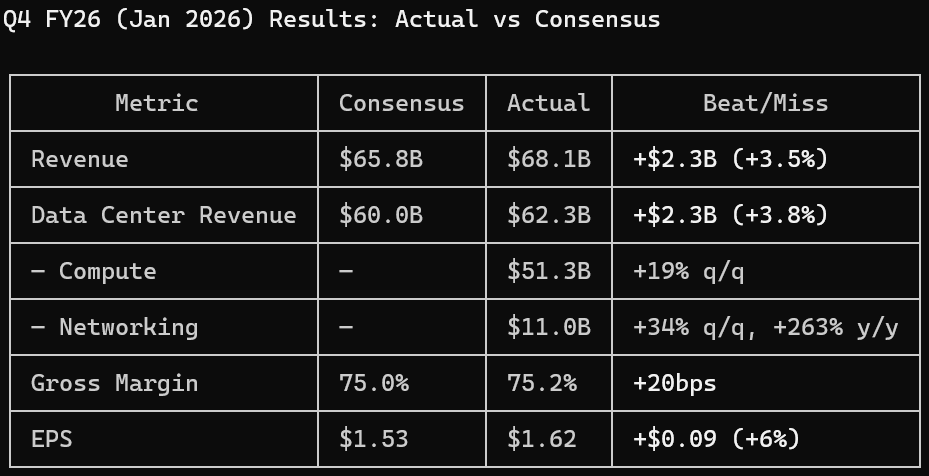

Current quarter guidance: $65b revenue, 75% gross margin.

Current quarter consensus: $65.8b revenue, 75% gross margin, $1.53 EPS, $60b datacenter revenue.

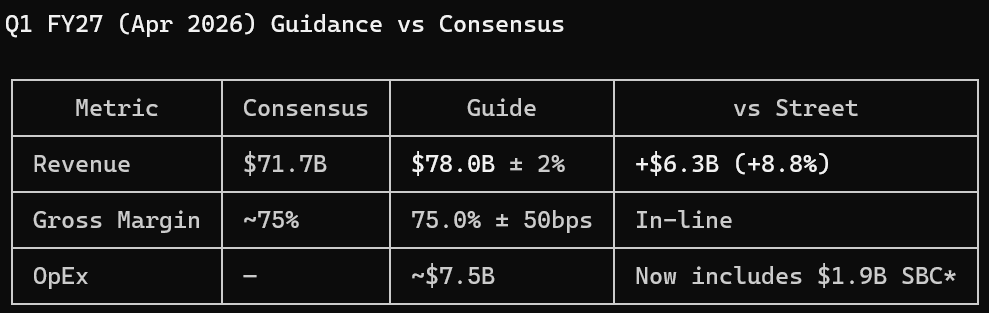

Next quarter consensus: $71-75b revenue. $71.7b official consensus. Buyside bogey probably $75b or slightly higher.

The Print

I expected nothing less from Jensen than this absolute blowout. But tbh, this is mostly first order stuff that probably gets forgotten by the market within a few trading days. Still, it’s helpful to go over it to set our baseline.

The guide is really the number that matters the most. People know it’s a beat so at this point we be scrutinizing the size of the beat.

Whisper numbers around $75-76b. $78b is an enormous 8.8% above consensus.

Importantly, this was larger than last quarter’s guidance beat of $65b vs $61.8b, or 5.2%.

Last quarter there was some hair on the 73.7% gross margin, but this time, we got a clean 75%. No hairs whatsoever on this print.

$95.3b in supply commitments for inventory and capacity is interesting. Let’s see what that means. Memory capacity…………? :)

Networking outgrew compute as well, with 34% vs 19% sequential growth, again serving as a leading indicator for further growth.

Price Action

To those new to Nvidia, this makes no sense. We could have asked for nothing more from this quarter. What would actually make the stock go up?

However, we saw the same last quarter. Each earnings becomes a pump-and-dump, because there is a structural reason why Nvidia trades range-bound unlike the other AI infra suppliers that I will dive into behind the paywall.