Economics of the Singularity | ALL STOCKS ARE UNDERVALUED

Tokenmaxxing is about to agentmog the Shiller CAPE-cels

Why do we invest in semiconductors? Well, obviously, AI. By owning semiconductor stocks, we own an upstream component in the supply chain for tokens and can therefore capture some of the value generated by AI.

However, if our end goal is to invest in AI and semiconductors are only a means to that end, I believe it’s ignorant not to look further downstream. This is exactly why I wrote my $100 trillion dollar Anthropic article.

Model labs are an even sharper expression of one’s belief in AI, because they generate the tokens themselves. Plus they capture both the upside from token value creation and from Moore’s law-driven cost reductions. I think they are the greatest business models (both in and out of AI) of all time.

But this is already well known. People are selling their kidneys for Anthropic stock. I am only saying that model going to be even more valuable than people predicted. But people are definitely already VERY excited. And when there’s that much excitement, alpha is harder to find.

But funny enough, by going just one step further downstream, to the thousands of regular businesses consuming the tokens Anthropic sells, all of that excitement ends. Here’s where you can be a true contrarian. Meaning possibly much more asymmetry.

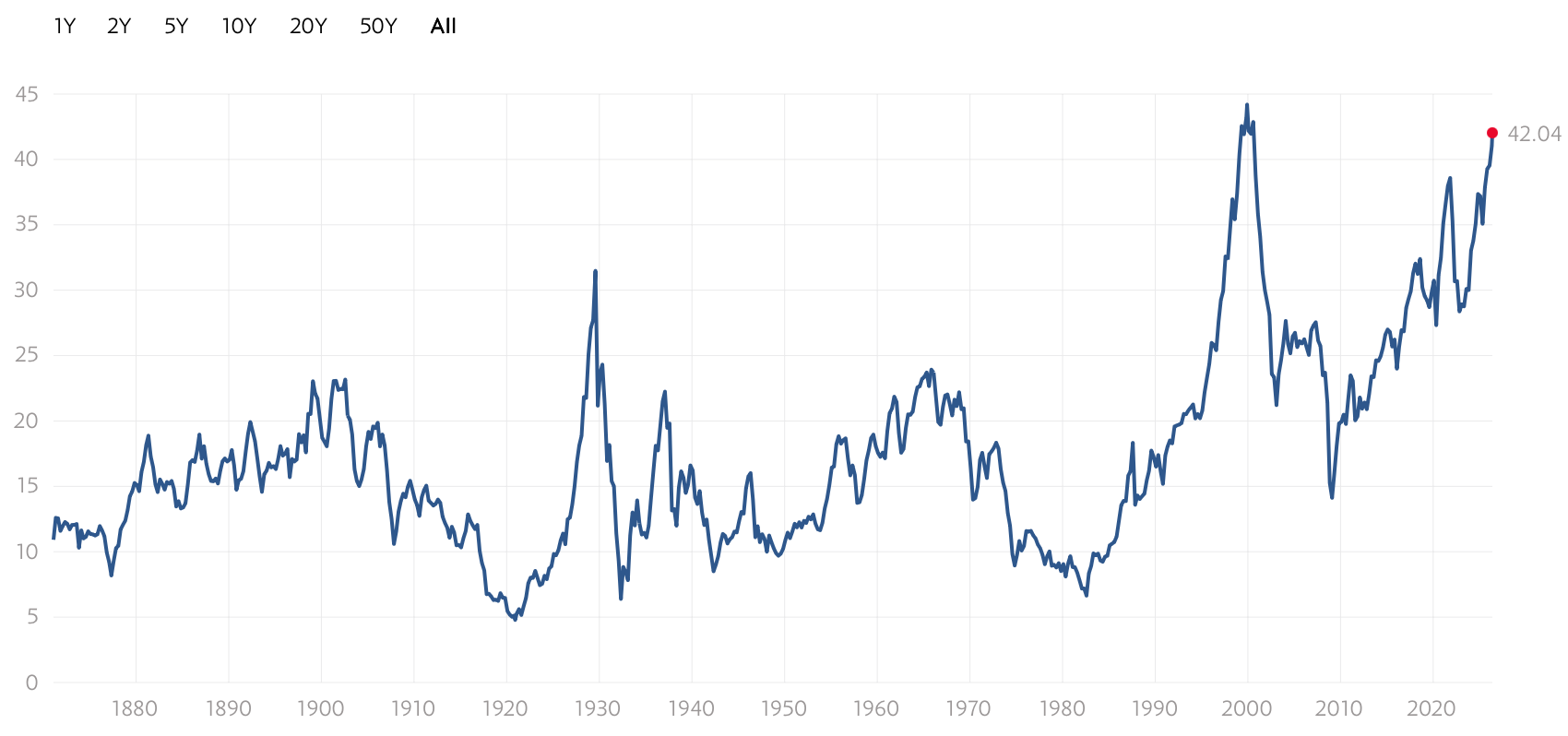

This is the Shiller Cyclically Adjusted P/E Ratio, or CAPE.

Today CAPE is at 42x. We are in unprecedented territory that has only ever been reached at the height of the dot-com bubble. We’re even higher than in 2021, which involved a speculative frenzy and preceded a brutal year-long bear market.

Every single time the Shiller CAPE was elevated, a crash followed. It is the world’s most reliable bubble indicator. Even if we don’t crash, these high valuations can be back-solved into a terrible forward CAGR.

It creates the perfect excuse to ignore stocks on the index level, and therefore the perfect mechanism for markets to underprice the singularity.

Tokenmaxxing is about to agentmog the Shiller CAPE-cels.

By accessing this content, you acknowledge and agree to our terms and conditions. This research is not financial advice.

Contents

Microtokenomics

Why The “Intelligence Crisis” Won’t Happen

Timing and Revisions

The Trade

Microtokenomics

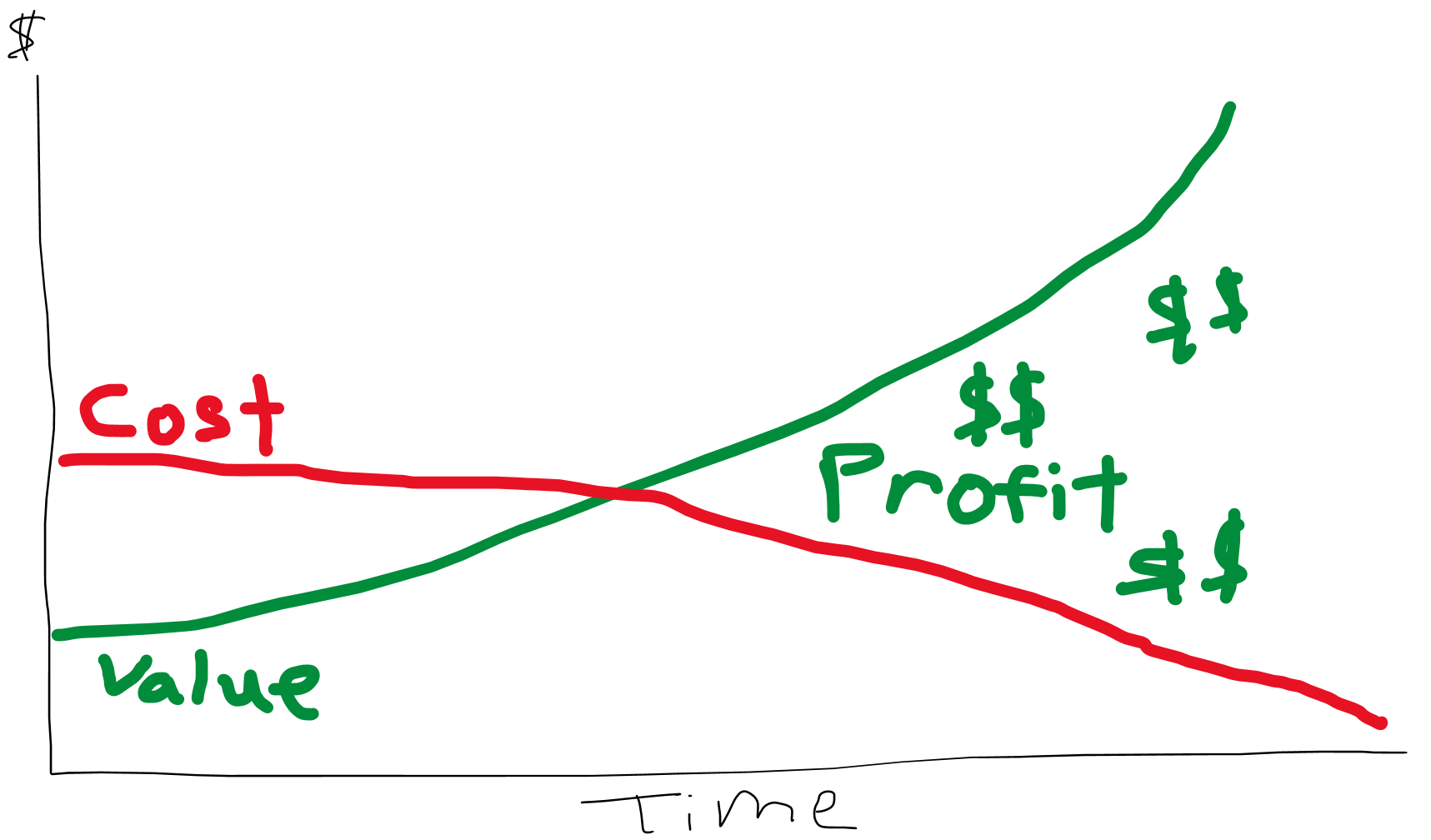

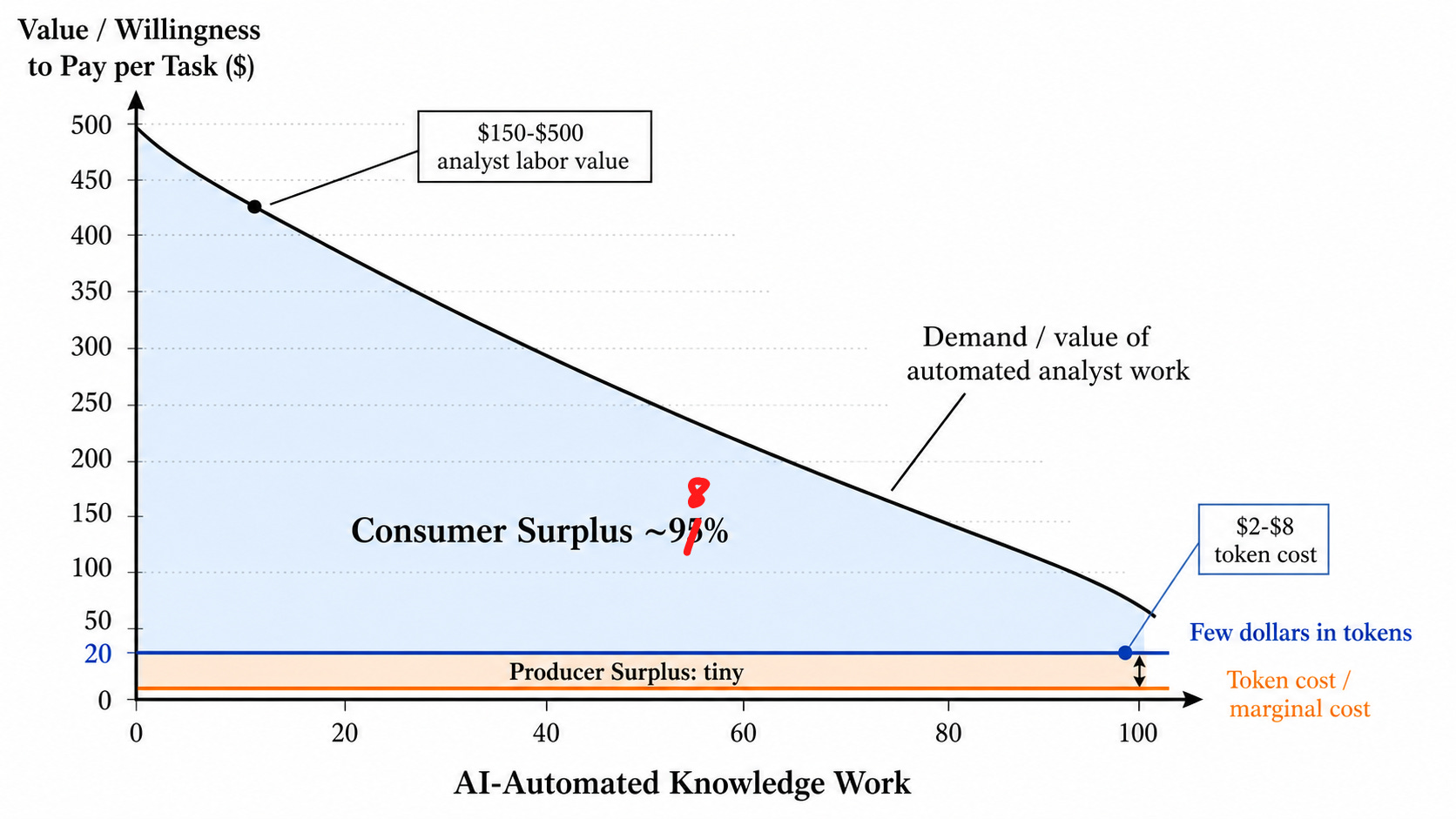

In every business or market, there is value creation and value capture. It’s a fancy way of saying consumer surplus and producer surplus, where value creation is the sum of all surplus and value capture is simply producers’ portion of it.

In AI, we can think of value creation as the value of the work that AI agents do for end consumers (how much benefit I get from tokenmaxxing) and value capture as the price charged by the model labs for inference (which also flows down to Nvidia, TSMC, the memory makers, ASML, etc.).

The higher the value capture compared to value creation, the more valuable that AI labs and semiconductors should be relative to the rest of the economy, and vice versa.

To analyze how big the value capture is compared to the value creation, we can look at microtokenomics. There’s not actually a thing called microtokenomics lmao this is just what I call looking at the value per token generated on a per-task basis.

SemiAnalysis did some amazing work on this. This is possibly one of the most impactful SemiAnalysis articles I’ve ever read.

Here is the most important quote from the article. This states very plainly an idea that I’ve believed for a while but struggled to articulate.

“End users are enjoying a productivity bonanza - tasks that used to take tens of person-hours costing thousands of dollars can now be accomplished in minutes with a just a few dollars’ worth of tokens. This huge surge in revenue and margins is because the value of tokens being created is dramatically improving businesses. For example, SemiAnalysis has reached as high as $10.95 million dollar annual spend rate on Anthropic Claude tokens, but the value we derive allows us to outcompete all our competitors and gain market share.”

Later in the article, SemiAnalysis goes on to demonstrate traditional knowledge work tasks that would have taken several hours of traditional analyst labor, costing from $150 to $500, being able to be automated with a token cost of $2 to $8. They included tasks like:

pulling 5 years of financials and emailing the results with Excel tables attached

searching past conferences for optical networking and OCS trends

The ROI on tokens spent in these examples is over 50x.

So yeah, the ROI question is solved.

This has allowed Model Labs to expand their gross margins from the 30s and 40s all the way up to 70s and soon moving into the 80s as they take advantage of their pricing power. At the current point in time, if the ROI on tokens spent is over 50x the cost of the tokens, producer surplus is about 2% of the pie, while consumer surplus is 98%.

That orange sliver is the entire AI token supply chain that we are all invested in, everything from the Model Labs to the fabless chip designers to the foundries to the memory makers to the equipment vendors to the optical networking providers and to the power generators. All of that is 2% of the pie. The 98% gets spread out across every other firm in the economy. For every trillion dollars added to Anthropic’s market cap, $50 trillion or more should be added to the market cap of the S&P 500.

People see the ROI question mostly as a question for the AI infra value chain, but but it’s actually far more important for the economy. Negative ROI on AI means that every dollar spent reduces aggregate earnings for the S&P 500, while positive ROI means that every dollar spent adds to Aggregate Earnings.

In our case ROI is extremely positive. Every dollar of revenue for a model lab is an order of magnitude more value created for the economy (in the form of aggregate earnings). In addition, this aggregate earnings boost definitionally grows at the same exponential clip as the model lab revenues as AI penetrates deeper and deeper, meaning that earnings growth for the S&P 500 should accelerate beyond what historical norms suggest.

This is why the Shiller CAPE is flawed. Of course, stocks, which are supposed to price in future earnings, look funny based on past earnings if the future earnings are all of a sudden growing way faster than before!

Why The “Intelligence Crisis” Won’t Happen

This famous and very well-written article by Citrini single-handedly made consensus bearish on AI-impact-on-stocks.

Today, after seeing more empirical data, I am vastly more bullish, and the reason is a sort of a Jevons paradox but for labor.

Nathan put it well in his podcast, the AI Daily Brief.

“And what was interesting in all of this is that both the promise and the fear of AI, the promise of AI that would reduce how long it took to do your work so you could go enjoy more leisure time, and the fear of AI that would negate your value as a worker.

We’re both very far away from the lived reality of the most advanced users.

In fact, instead of finishing your work day at 3:00 PM, the more common challenge was people having to force themselves to go to bed at 3:00 AM, tearing themselves away from the next thing they could accomplish, which was always just sitting there waiting for them.”

What we see empirically is that when people use AI, they work way more rather than way less.

More quantitative evidence for this can be found in proxy metrics for the formation of small businesses. In the post-agent era, the number of domain names being registered and small business applications filed has sharply inflected.

The economic theory behind this effect is perhaps more important than the data itself.

Citrini’s original scenario went something like this: AI can do the same things that humans can do. It starts in coding, which is why software engineers get replaced first. These displaced workers stop spending, which weakens the economy and forces more businesses to cut workers and replace them with AI, further reinforcing the cycle. This continues until the drop in spending destroys the credit markets and causes a financial crisis.

The core premise of this scenario is that there is a fixed amount of work to do. The first software engineers get replaced and stay unemployed as AI has taken a portion of that fixed pie of work. This is why the empirical evidence that AI has created more work to be done than ever before is important because it shows us that the pie is not fixed. AI reduces the cost of providing many services in the economy. For example, coding, writing, and creating infographics. Many goods and services that were previously too expensive and uneconomical to produce (such as starting a software business which used to take millions of dollars of engineering talent and multiple rounds of VC financing, now only requiring a $200/month subscription to Claude) now become viable. These new goods and services present themselves in the economy as business ideas that are only possible in the age of AI. These businesses then hire more people and that then increases employment.

The end result is essentially a Jevons paradox but for labor. By making work cheaper we vastly expand the universe of economically useful work to be performed and cause the need for human labor to go up and not down.

Those first software engineers don’t get replaced because they can now do far more within the organization, or they find a new job because new businesses are created that are hiring, or they start their own businesses. The vicious cycle never begins.

There’s also another argument that humans are partially a complement to agents, rather than agents fully being a human substitute, which is argued by Dan Shipper in his essay “After Automation.”

You can read it here.

I am much less confident in this theory as we have yet to see the empirical evidence for this with much more powerful models. If this is indeed the case, AI can be treated much more like past automation technologies like spreadsheets, factories, or farming equipment which are a complement to labor (and are the examples used for the “the Luddites are wrong again” argument) rather than the theoretical substitute that is more consensus.

Timing and Revisions

The biggest risk to this trade is probably timing.

The AI build out happens before AI creates value. That is why it’s been so much easier to invest in AI infrastructure and make money than it has been to try to predict anything at the application layer or the end economic effects.

Dylan Patel has said in a podcast before that the hardest part of his job isn’t analyzing the semiconductor supply chain (supply-side) but is instead analyzing the demand side.

“I think the hardest area for us and for everyone is understanding tokenomics, economics of tokens. I think we have a really tremendously like good insight into how much it cost to run infrastructure, what the cost of tokens are, what the cost of models are, what the margins of these labs are. But the usage and adoption is what’s really difficult to model, you know, continuously, right?

We, we have these like we had like crazy in January, we had crazy estimates for February, Anthropic smashdown. How do we calibrate this model? What are the data sources for this February? We had crazy assumptions for March and then they smashed them and everyone sees the number of 10 billion and they’re like, what the fuck? How do they add 10 billion of revenue? Who is using all these tokens? Why are they using them? What are they building with them?

And then more importantly, with what they’re building with these tokens, how is that actually diffusing into the economy? And what value is that generating? Because it’s not really something that you can capture in any any GDP statistic, right?

All of the value of the tokens that I use get transformed into better information, which I then sell at a discount to what people used to sell information for relatively because and therefore that information is now making its way throughout the economy and and people are making better investment decisions or better competitive decisions.

But if they’re semi data company or data center company or hyperscaler. And now how, how much what, what is the value of this? And what is that? What is that done to the economy? It’s clearly by every subjective metric, amazing.

But where is the phantom GDP? What is the phantom GDP? How do we track the real economic because because the GDP metrics are not, you know, accurate.

If you were to say what is the GDP that Dylan Patel is making? It’s tiny compared to what the value that I think is being created. And so ultimately, what is the value being created by these tokens, not on a basis of, you know, just simple, you know, what is the knock on effect, right? What is the knock on effect of all the things that these things are doing? And I think that’s the real question and challenge that that’s hard to measure.

I think we’ve got a tremendous, you know, reading on the supply side of things. I think we’ve got a tremendous reading on even a lot of the demand side signals. But it’s it’s what is the value these tokens are generating that’s hard to quantify and measure.”

Thanks, Dylan, for the very long quote that says literally exactly what I wanted to say.

We know how much hyperscaler capex is going to be spent this year, but we can’t predict when that capex is going to turn into token revenues, let alone when those token revenues are going to contribute to productivity in the economy at large, let alone how much productivity it’s going to contribute and if that is big enough to actually move aggregate S&P 500 earnings or aggregate GDP. It’s really hard.

However, even though we can’t draw perfect causation, our job as investors is to take imperfect information and make an interpretation of it that allows us to make asymmetric bets. We can analyze the empirical data from today and come to our own conclusion on if we are too early to see the economic diffusion of AI.

And even though we are still super early in the S-curve adoption of agents, we are already seeing some anomalous data that suggests we are not too early for their macro effects.

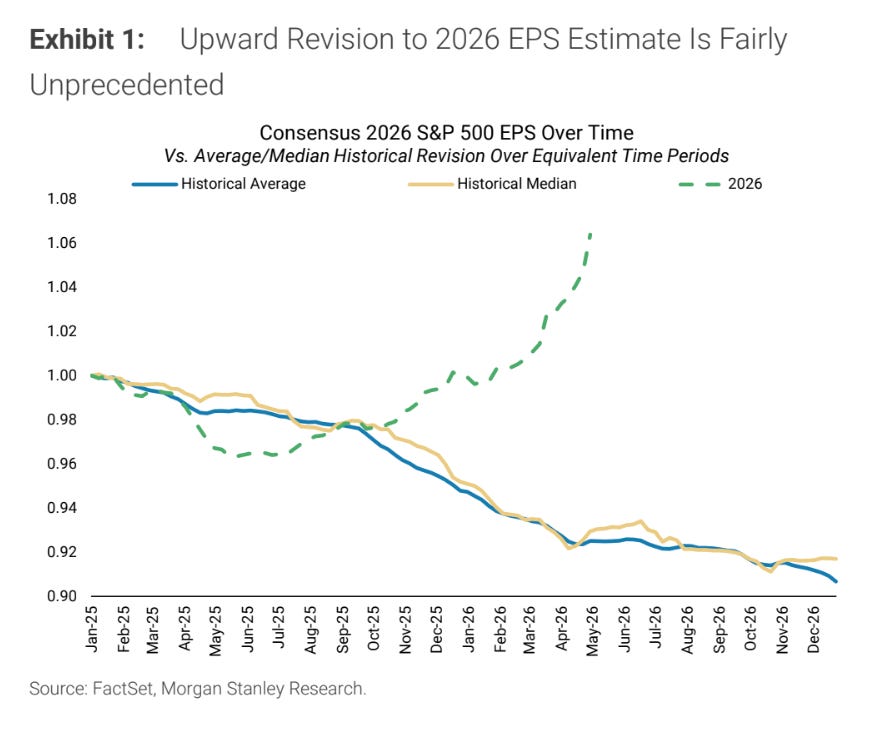

First, 2026 EPS revisions are completely outpacing the historical norm. Funny enough the kink in the chart is quite literally right when Claude Code got widely adopted in January and February of 2026.

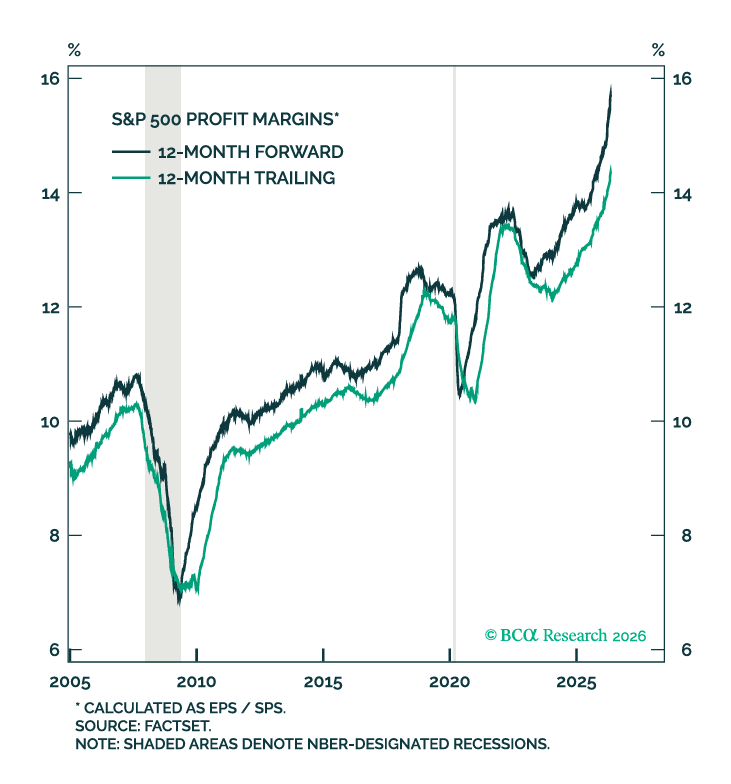

Second, S&P 500 margins are also increasing much faster than history would suggest, showing that the same revenues can be achieved on a much smaller cost structure, a structurally healthy sign for economy-wide ROIC.

While it is impossible to link these effects to agentic AI and it is easy for it to become another example of the classical correlation and not causation logical error, this is enough evidence for me to conclude that there is likely an effect of AI here and “likely” is good enough for a trade.

The Trade

I called out a trade in my subscriber chat not too long ago (May 8th). You know which one this is lol.

It’s performed quite well since.

It is…