Lumentum | Earnings Review: All of the LITEs (Free Release)

Can the multibagger continue to multibag? Exploring OCS, EML, and updating CPO model

Opinions are my own and do not represent past, present, and/or future employers. All content is based on public information and independent research. This newsletter is not financial advice, and readers should always do their own research before investing in any security. I am invested in the semiconductor industry. As of the date of this publication, I currently hold a long position in Lumentum Holdings (LITE). Feel free to reach out at jasonschips@gmail.com.

I built a tool using Claude Code to automate DCF valuation.

As promised, I am making my earnings coverage on Lumentum free one week after release. This is the kind of content paid subscribers get early access to after each earnings for the companies in my coverage. They are still ripping for all the reasons I discuss in this article. Tbh this is more like a part 3 to my coverage than an earnings note.

See my past coverage on Lumentum:

Pre-Earnings Vibe Check

(This section was written prior to the earnings call to communicate the prevailing narratives and provide a contrast to post-earnings sentiment)

Lumentum is up 5x over the past year. When I published Part 1 of The Lumentum Series in December, lite was $320. When I published Part 2 in January lite was $350. Today it’s $440. If you are scared of heights, this is not for you. (I passed on Bloom Energy because I was scared of heights which was not a good idea in hindsight.)

This is absolutely a beat-and-raise-or-die setup.

At the same time optics have been… performing quite interestingly. There have been multiple days where the Nasdaq is down 2%, SMH down 4%, and both LITE and COHR are green. These are names with infinity beta trading like consumer staples.

There are three narratives I’m watching tonight. Let’s walk through each.

First is the EML laser shortage and pricing power. This is the near-term earnings driver, the thing that actually shows up in the P&L right now.

In Part 2 of my series, I laid out the case for a major shortage in 200G EMLs. The logic is straightforward: 1.6T requires 200G EMLs with a ~2x ASP premium over a 100G EML but occupies roughly the same footprint on the wafer. Meanwhile, industry-wide InP capacity is maxed out. Lumentum was already running at 100% utilization last quarter, shedding customers because the supply/demand imbalance was so brutal, and is in the middle of a 40% capacity expansion including a migration from 3-inch to 4-inch InP wafers. Nvidia wants them to 30x capacity by 2030. Let that sink in for a second. A customer is telling their supplier to increase production by thirty times.

Channel checks indicated Innolight was raising prices $100 per module on 1.6T transceivers to Nvidia because of EML tightness. That’s the downstream effect of laser scarcity flowing through to module pricing. On the upstream side, management has been signaling “double-digit” price hikes on EML chips for 2026.

The second is of course CPO. This is what provides the really long duration growth.

Since I published The Lumentum Series | Part 2: Co-Packaged Omnipotence, the CPO story has actually gotten more bullish. Nvidia has apparently gotten more aggressive with their CPO plans, pushing harder on scale-up CPO. In a Rubin rack, scale-up CPO content is now several times the scale-out CPO content, which means the number of optical engines for Lumentum is higher than I initially modeled.

AYZ had some really good (and bullish) research on Nvidia’s accelerating scale-up CPO roadmap you should go check out.

Third is OCS. Lumentum is the only external company globally capable of mass-producing MEMS-based optical circuit switches for Google’s TPU architecture. It’s critical to Google’s TPU + OCS + 3D Torus hybrid that gives them a scaling advantage over everyone else - Ironwood (TPUv7) interconnects 9,216 chips via OCS into a 1.77 PB memory pool, dwarfing Nvidia’s GB300 at 20.7 TB per rack.

Rosenblatt noted that management targets $100M per quarter in OCS revenue by 4Q26 (the June quarter). TAM estimates are generally around $10-15b by 2030, so it’s a huge market, albeit smaller than CPO.

Currently, this is still a Google-only story. LITE was used heavily as a Google TPU proxy back in Nov when the whole short OpenAI complex long Google trade happened. Arguably more exposure to TPU than Google itself. The open question I don’t have a great answer to yet: is OCS expanding beyond Google? Meta and Microsoft are exploring OCS architectures. If a second hyperscaler commits to OCS, this goes from a single-customer product to a platform.

Check out FundaAI’s research on OCS and LITE’s role in the Google TPU ecosystem. These are not sponsored btw I just like pointing out good research by the community.

All of the LITEs continue to shine bright heading into tonight. There are obvious risks at these levels but the setup across all three business lines is about as good as it gets for a company this early in its inflection cycle.

The Print

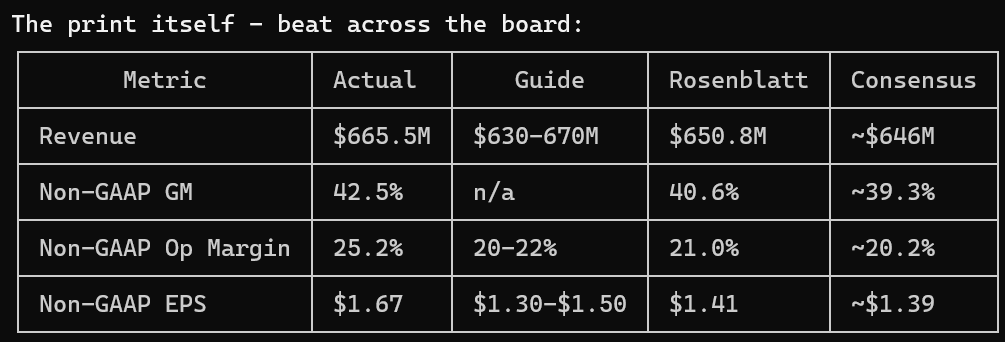

They crushed it. Behold my Claude Code terminal table:

Revenue hit the high end. Not a huge beat on the top line, but that’s not where the story is. The story is profitability. Gross margin at 42.5% cleared consensus by 250 bps. Operating margin at 25.2% blew past the top end of their own 20-22% guide by 320 bps. EPS at $1.67 was 20% above consensus.

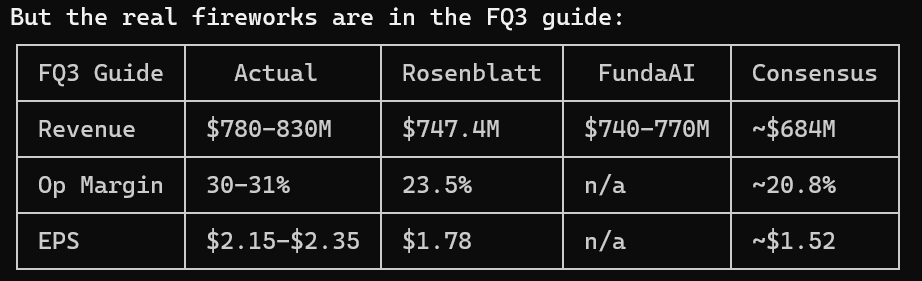

But the guide is where it gets stupid.

The FQ3 revenue midpoint of $805M is 18% above consensus. And op margin is guiding to 30-31%, another 500+ bps of sequential expansion. At the midpoint of the EPS guide ($2.25), that’s a 35% sequential increase. On 85%+ Y/Y revenue growth. The operating leverage in this model is just obscene.

In addition, OCS backlog is now “well beyond $400 million.” That’s the first time they’ve quantified OCS demand this explicitly, and it gives us a hard floor on committed revenue. Second, they received a “multi-hundred-million-dollar order” for CPO, deliverable in H1 calendar 2027. That’s Nvidia CPO becoming a real P&L event with a specific timeline and a specific order size.

Price action was very weird. Spike on the print, then fade into the call, and now back up into the overnight session. I am ignoring this. Market is strange, I’m not gonna call the reaction until the next 2 trading sessions finish.

The Call

Key Positive Themes

1. OCS Goes Kinda Hard

Management originally targeted a $10M quarterly OCS run rate for next quarter. They hit it this quarter. Manufacturing readiness is proceeding ahead of plan, and the backlog of “well beyond $400M” that we saw in the print now has a timeline attached: most of that $400M+ ships in H1 2027. They also disclosed that the CY26 exit rate will be “quite a bit higher” than the previously projected $100M quarterly run rate.

But the real revelation was customer diversification. The market (including me) had been treating OCS as a Google-only product. It’s not. Lumentum is now shipping OCS to three customers, with multiple customers comprising the backlog, and those customers are increasing their demands. The question I asked in the pre-earnings section - “is OCS expanding beyond Google?” - got a definitive yes. FundaAI hinted that Meta and Microsoft were exploring OCS architectures. Turns out they weren’t just exploring.

Management also outlined four distinct OCS applications across every customer: spine replacement, scale-across, optical scale-up, and network redundancy.

2. CPO: Scale-Up TAM Unlocked

The near-term trajectory is now quantified: ~$50M quarterly CPO run rate by CY26 Q4, with the “multi-hundred-million-dollar order” from the print kicking in during H1 2027. By late calendar 2027, management expects the first scale-up CPO shipments to begin replacing copper. This is the timeline the market needed to hear.

What current CPO revenue consists of is mostly scale-out. The scale-up opportunity is brand new. This is a large chunk of TAM that literally did not exist in anyone’s model before Nvidia got more aggressive with its CPO plans. I also under-modeled scale-up and will address this later.

Management also made clear they feel even better about their competitive position in CPO lasers than they do in EML. Their ultra-high-power CW technology was originally proven out in subsea applications over many years, giving them a reliability track record that competitors can’t replicate quickly.

3. EML Share Remains Significant at 1.6T

The sell-side likes to complain about this one a lot and TBH the concerns are valid.

Will SiPho be the majority of 1.6T transceiver shipments eventually? Yes, management confirmed this. But the absolute numbers are so large that even with SiPho taking the majority of percentage share, there will still be substantial EML growth in absolute terms. EML is dominant in WDM (wavelength division multiplexing) applications, while SiPho is taking share in fiber applications. The two architectures are coexisting, not competing for the same socket.

On top of this, Lumentum is introducing 200G differential EMLs, a new product variant that offers power efficiency advantages for customers and represents another ASP tailwind. By year-end, management expects 200G EMLs to represent 25% of their datacom chip mix, up from ~10% today. And they noted their 1.6T transceiver market share is higher than their 800G share, with a stronger growth trend.

Key Negative Themes

1. The Capacity Bottleneck

I think the market wanted to hear far more than what it got on capacity.

Management delivered on half of the previously guided 40% supply expansion this quarter - and they front-loaded it, which is why it was already in the FQ2 numbers rather than FQ3. They’ll do “a little better” than 40% overall, but haven’t quantified by how much. They have “line of sight” into a significant block of new capacity with better fab utilization. The remaining ~20% of the expansion will come online over the course of the calendar year.

Here’s the problem: even as they add capacity, the supply-demand imbalance is increasing, not narrowing. Management said the gap is “about the same, incrementally up” versus last quarter. Which is good because there is crazy demand, but as we learned from Intel’s last earnings, demand doesn’t turn into revenue unless you have the supply. For a stock priced for perfection, “line of sight” into future capacity isn’t enough. The market wants to know Lumentum both has insane demand AND will close that 25-30% supply-demand gap, and there’s no clear timeline for that.

The most interesting new disclosure was contract manufacturing. Lumentum is exploring outsourcing and has hired someone specifically to focus on it. Who could they be outsourcing to…?

For Coherent, it’s a massive opportunity. Like the AMD to Lumentum’s Intel, every EML and CW laser that Lumentum can’t ship is excess demand that Coherent will gladly absorb, particularly as their 6-inch InP wafer fab ramps yields. You can see this reflected in Coherent being up almost as much as Lumentum in the after-hours session. This is why I own both.

2. No EML Pricing Squeeze

Some rumors heading into the print suggested Lumentum might announce aggressive EML price hikes - the kind of squeeze that would show up as a dramatic gross margin inflection. That didn’t happen.

What we got instead was more measured: prices are “holding or even increasing.” Management has done “a couple of step-ups” and noted they “have pricing leeway” available. Long-term agreements have helped lock in pricing at elevated levels - there are no price-downs in the current environment. Where incremental pricing shows up is when customers demand volumes beyond what their LTAs cover, and those incremental orders come at higher prices. These price increases are flowing through to the March quarter guide, but management described the overall revenue impact as “relatively modest.”

This is good, but it’s not a blowout. The 42.5% gross margin beat was driven more by mix shift (200G EML at ~2x ASP, higher Systems revenue) and cost efficiency than by dramatic price increases on existing products.

Narrative Check

EML pricing power: Weakened. The pricing squeeze some expected did not materialize. This is fine, but the narrative that EML pricing would be a standalone upside driver took a hit.

OCS: Strengthened. This was the biggest positive revision on the call. The $10M run rate arrived a quarter early. The backlog has a concrete shipping timeline. The customer base expanded from one to three. And the CY26 exit rate is now above the previously guided $100M/quarter. OCS go brrr.

Not meaning to state the obvious, this earnings is highly constructive for intrinsic value and I see the after-market reaction as justified.

The Most Valuable Information on the Call and Model Update

This earnings call provided clarity on a key lingering question that I and many other analysts have had about CPO - one that fundamentally changes how to model the business. After the call, I have revised my CPO estimates and become many times more confident in the structure of the CPO business. Though my assumptions still depend on the industry adoption rate and unit shipments, the business model and my ASP assumptions have now been fairly crystallized. I believe I am the first analyst to incorporate the following framework for modeling Lumentum’s CPO revenue and I expect others will adopt a similar approach as the business scales.

Subscribe to read the most valuable takeaway from the call and my updated CPO model. Full breakdown and model update below the paywall:

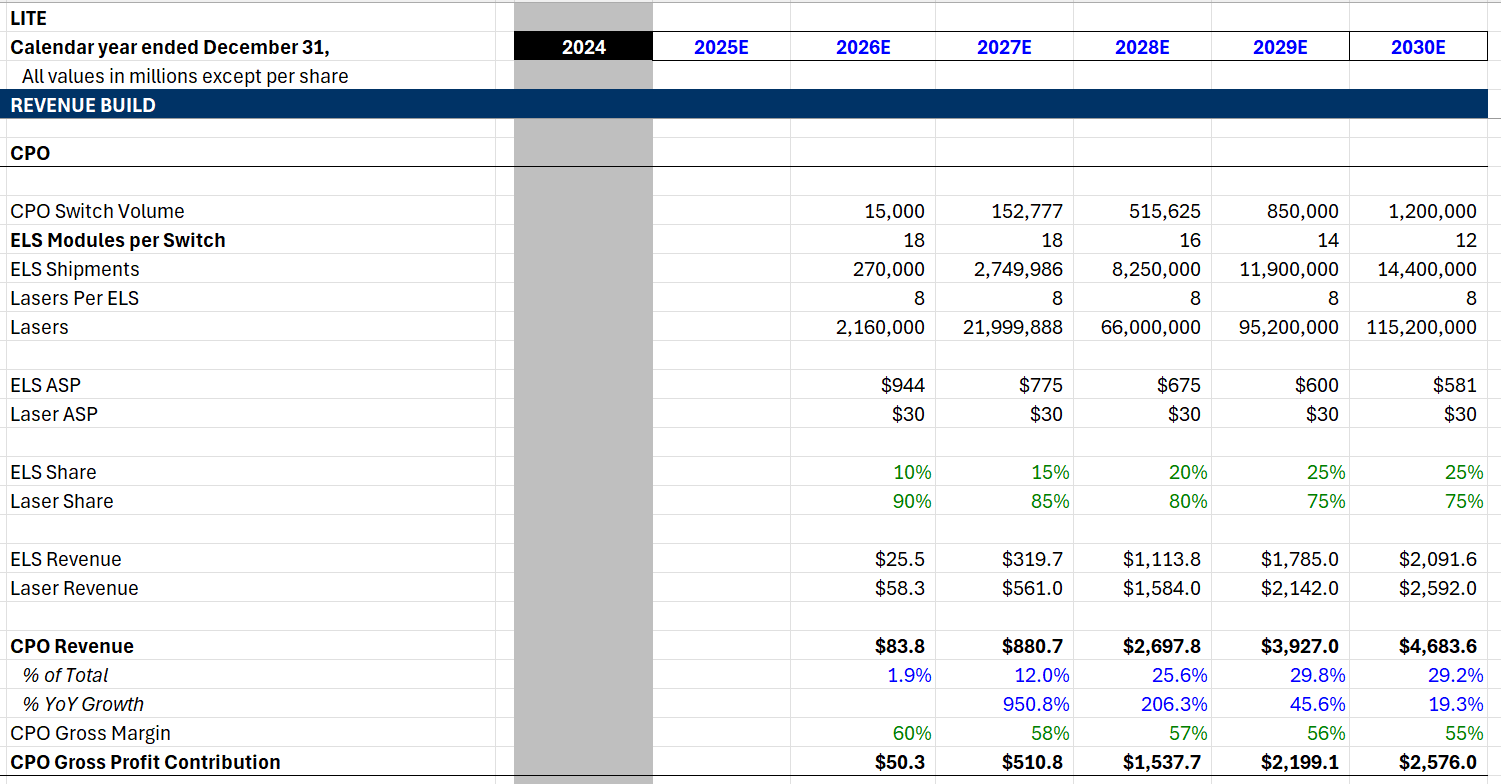

In my original Lumentum Series Part 2, I modeled CPO revenue using ELS module shipments at ~$1,888 ASP per module. I had always debated with myself whether Lumentum actually sells the complete ELS module or just the UHP laser chips that go inside it. I always concluded it had to be the module - we can see it on their product page. So what gives?

On the call, they clarified something important: Right now, they are only shipping the laser chips. But they are planning to expand into selling full ELS modules for the margin and ASP benefits. Management explicitly stated that ELS content represents ~2.5x the value of just the lasers alone.

I also previously made the mistake of under-modeling scale-up shipments from my estimates. With recent reports suggesting Nvidia will push scale-up CPO aggressively, some in the industry place scale-up CPO content at several multiples of scale-out content per Rubin rack shipped. This means my original unit shipment estimates were off by roughly half an order of magnitude. We may see 8.2 million ELS modules shipped in 2028 based on these estimates. With numbers that large, using my old ELS ASP assumptions makes absolutely zero sense. I’m talking $10M+ in CPO revenue by 2028 and still growing at triple digits. And no, even though I am long Lumentum, I don’t believe its the next Broadcom.

Here’s how the ASP math actually works. Multiple industry participants have confirmed laser chips at approximately $30 each. With 8 lasers per ELS module, that’s ~$240 of laser content per module. At 2.5x, the full ELS module comes in at ~$600 at mature mass-production pricing. I assume initial pricing starts higher, around $775 in 2027, decaying slowly each year as volumes scale - standard learning curve dynamics. I’m much more confident in these ASPs than I was before.

The framework I’ve built is to model Lumentum’s CPO revenue as two streams: laser chip revenue and ELS module revenue. We want as much of this revenue to be ELS as possible, since their content is higher. Since they are currently shipping mostly lasers but plan to expand into ELS, I model the starting ratio at 90% lasers / 10% ELS, gradually shifting to 75% lasers / 25% ELS by 2030. You add both streams together to get total CPO revenue.

This framework produces nearly identical revenue estimates to my original model that assumed 100% ELS modules at higher ASPs with lower shipments. Funny how the math works out. But I’m far more confident in these numbers now because the underlying assumptions - $30 per laser chip, 2.5x for the module, mix shifting over time - are each individually anchored by management commentary or industry confirmation, rather than relying on a single large ASP assumption.