Coherent | Earnings Review: The Sleeper Print (Free Release)

I think the market is wrong (?) The forgotten child of the optics family may actually have a comeback.

Opinions are my own and do not represent past, present, and/or future employers. All content is based on public information and independent research. This newsletter is not financial advice, and readers should always do their own research before investing in any security. I am invested in the semiconductor industry. As of the date of this publication, I currently hold a long position in Coherent Corp. (COHR). Feel free to reach out at jasonschips@gmail.com.

I built a tool using Claude Code to automate DCF valuation.

As promised, I am making my earnings coverage on Coherent free one week after release. This is the kind of content paid subscribers get early access to after each earnings for the companies in my coverage.

Pre-Earnings Vibe Check

(This section was written prior to the earnings call to communicate the prevailing narratives and provide a contrast to post-earnings sentiment)

Lumentum reported last night. They had a crazy beat on the raw numbers, especially for gross margin, revenue guide, and operating margin guide. They confirmed what the optical supply chain has been signaling for months: the industry cannot make enough lasers. EML supply-demand gap widening, 1.6T adoption accelerating, 800G still growing underneath it.

Coherent is generally seen as an inferior version of Lumentum.

COHR has rallied on the optical revisions, but nowhere near as much as its peer. They are still tryna qualify CPO lasers, make lower-quality EML, and their OCS approach (liquid crystal) is gaining less traction than Lumentum’s MEMS. However, what they have that Lumentum doesn’t is massive scale, able to ship 5-10x the transceiver volume.

Three narratives to watch:

1) 6-Inch InP Yield Ramp — the margin inflection story. Coherent’s 6-inch InP wafer fab became fully operational this quarter. In theory, 6-inch lines offer materially superior yield and output vs traditional 3-inch.

Like think about it.

BIG CIRCLE PRINT MORE SQUARE

In practice, initial yields are lower as expected during early production. The question tonight is how fast the learning curve is progressing. If yields come in ahead of plan, Coherent moves toward EML self-sufficiency, meaning it buys less lasers from Lumentum which has been the bain of their existence recently. This is the single most important variable for Coherent’s margin trajectory over the next 12 months.

2) Supply Chain Positioning — the demand-overflow-capture story. Coherent is vertically integrated across critical optical components (isolators, Faraday rotators) and is internalizing EML and CW laser production. It is U.S.-based, which matters as hyperscalers diversify supply chains away from Chinese transceiver vendors like Innolight. The industry is extremely constrained and Lumentum falls further behind demand every quarter. Where is all that excess demand gonna go?

Coherent plans to double internal InP capacity within the next 12 months, driven by 6-inch wafer lines in Texas and Sweden — a far more aggressive expansion than Lumentum’s 40% target that still has a 25-30% supply shortfall. This is a company building itself into the excess demand absorption machine for an industry that can’t make enough lasers.

3) CPO/OCS Disadvantage. Coherent hasn’t rallied as much as Lumentum because it lacks the same CPO and OCS credentials. On OCS, Coherent’s liquid crystal approach offers better reliability and scalability than MEMS but suffers from significantly higher insertion loss, and adoption trails Lumentum’s MEMS switches by at least two quarters. On CPO, Coherent has not yet qualified its CW lasers with any customer, let alone demonstrated the yields needed for commercial mass production. So very expectedly, COHR is the unloved child that trades at a discount to LITE. However, any progress here is currently unpriced. If Coherent can close either gap, ohhhhh boy. Get strapped in.

The Print

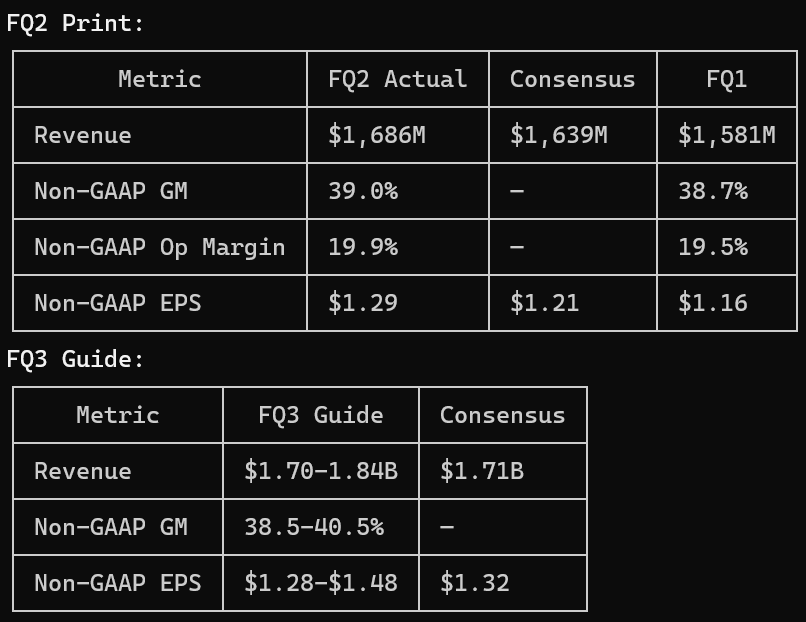

I was kind of shocked at how little info Coherent provides on their initial press release.

Behold my Claude Code terminal table (again):

The past quarter’s actual was fine. Revenue beat by 3%, EPS beat by 7%, gross margin expanded 24 bps sequentially. All lines above expectations. Not a blowout, but solid execution across the board.

The guide is where the market got disappointed. Revenue midpoint of $1.77B is only 3.5% above consensus and probably far below buyside whisper numbers. EPS midpoint of $1.38 is 4.5% above. Compare that to Lumentum guiding 18% above consensus on revenue and 24% above on EPS.

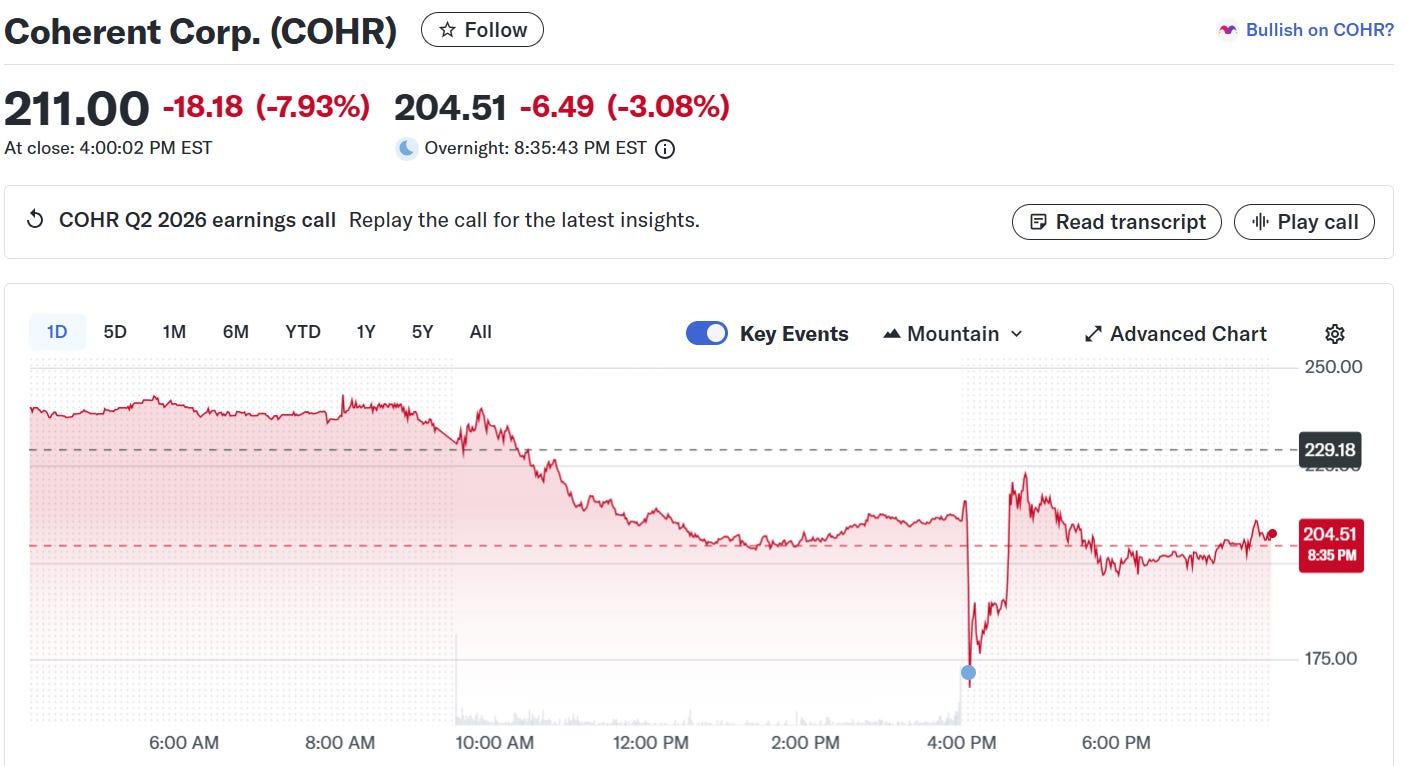

And they had some crazy whipsaw price action.

I must confess I traded this terribly and lost a lot of money. I panicked on the initial print and sold part of my position when it was down 20% at $172.

Then the call started and right when the right keywords hit my ears, I bought back… at $219. Yes you read that right.

Never trade an earnings call. No one has had time to digest information or make revisions. I ended up donating money to Jane Street robots. Take this as a lesson, dear reader. (but not as financial advice)

The Call

Now I just want to say. Once I locked in and started really digging into this transcript, I actually found it a fascinating quarter. I was a bear on the initial print, but the call flipped me from bear to bull very steadily throughout the 60 minutes. I think this is the kind of result that is prone to be misinterpreted for days after. There are several subtle details management pointed out on the call that act as “forcing functions” that lead me to believe they will post much larger beats 2 quarters from now. As you will see in my conclusion, this is a sleeper print.

Key Positive Themes

1. CPO Qualification

Last quarter, Coherent explicitly mentioned they were only sampling its 400mW CW laser for CPO applications. This quarter, they secured what Anderson called a “massive purchase order” from a market-leading AI data center customer for a CPO solution based on that CW laser. They did it! They qualified! Sure they didn’t quantify what massive really means like Lumentum did, but it’s good enough. A win is a win. They were never gonna go from sampling to splitting the CPO pie 50/50 with 800lb gorilla LITE. This was much earlier than I thought and I pulled in my CPO estimates for them by one year. No model today but I’ll have my COHR initiation out soon.

The purchase order is for a solution manufactured on Coherent’s 6-inch InP line in Sherman, Texas — and Anderson stated that U.S.-based 6-inch manufacturing was a key factor in the customer’s decision. Initial revenue is expected toward the end of CY26, with a more significant contribution in CY27 and beyond. Coherent also has CPO engagements across multiple other customers.

On scale-up CPO specifically, Anderson’s language was stronger than Lumentum’s. He described the scale-up CPO opportunity as “orders of magnitude larger” than scale-out and said it would “dwarf” scale-out. He also pushed back on the idea that scale-up is years away: “I wouldn’t call it years out, I think it’s sooner than that based on the plans that we’re seeing from our customers.” Honestly the language is better for Lumentum than Coherent lol.

2. SiPho Positioning vs. Lumentum

When asked about EML vs SiPho mix at 1.6T, Anderson stated: “We have both products, ramping both products, so depends on the application. There is not a big financial difference in either one.” Coherent is genuinely agnostic between architectures because it has competitive offerings in both.

This is a structural advantage over Lumentum. LITE’s core business is selling EML chips to third-party transceiver makers. LITE confirmed on their own call that SiPho will eventually be the majority of 1.6T transceiver units. As the industry shifts toward SiPho due to its structural cost advantage, Lumentum loses transceiver content; Coherent doesn’t. Coherent simply builds whichever version the customer orders. Combined with 1.6T ASPs coming in higher than 800G and gross margins being accretive at the new data rate, the transceiver mix shift is a tailwind for Coherent regardless of which architecture wins.

3. 6-Inch Execution Ahead of Plan

The market is focused on the guide being low and asking “what is management not telling us?” I am listening to management and asking “what is the guide not telling us?” Two forcing functions give me confidence I’ll be right.

This part is kind of funny because I took an intro to philosophy class 2 semesters ago and for whatever reason I had the intrusive thought to apply it to a Coherent earnings call…

Anyways, welcome to Logic 101!

Forcing function #1: the capacity math is a proof, not an estimate.

We have 3 premises

Coherent has increased capacity by 80%. (they had plans to double capacity and are 80% of the way there)

Demand is insatiable. (4x book-to-bill, supply-demand imbalance not closing this year or next)

Wafer starts take 6 months to become transceiver shipments. (specifically mentioned on the call)

If capacity is up 80%, demand exceeds supply, and wafer starts mechanically convert to shipments in 6 months, it is not just sufficient for but necessary that beats widen two quarters from now. Think about it… :)

And this also explains the weakness of the guide today. The guide is constrained by yesterday’s capacity, not today’s.

Forcing function #2: 6-inch exclusivity is a revealed preference.

Here we use modus tollens.

IF 6-inch yields were bad or not cost-effective, management WOULD hedge by adding some 3-inch capacity alongside it to mask the problem.

Therefore, IF management adds only 6in capacity, 6in yields MUST be good and cost effective.

I mean, you don’t bet 100% of your capacity expansion on a technology that doesn’t work.

An additional point: On cost structure, Anderson reiterated that 6-inch produces over 4x the chips at less than half the cost of 3-inch. They actually quantified the cost reduction of 6in vs last quarter where they were vague and just said it was better than 3in. By year-end, roughly half of internal capacity will be 6-inch.

Key Negative Themes

1. VCSEL Persistence at 200G

Anderson mentioned VCSEL-based 1.6T transceivers three times during the call, confirming a production ramp in H2 CY26. This is the same strategy the market criticized last quarter.

The concern is technical: VCSEL reliability degrades significantly at 200G per-lane speeds (thanks Irrational Analysis!). While VCSELs are cheaper to produce, pursuing them at 1.6T risks credibility with customers who prioritize reliability, which is the exact selling point Coherent emphasizes for its liquid crystal OCS and CPO products elsewhere on the call. The internal contradiction is notable. If 200G VCSELs underperform in the field, this becomes a margin and reputation headwind.

2. The OCS “Trust Me Bro”

OCS customer engagements expanded from 7 to over 10, backlog grew sequentially, and applications are broadening beyond scale-out into DCI and scale-up. The TAM is now “well above $2 billion” by end of decade, up from the prior $2B estimate. All directionally positive.

Buuuut that’s not what matters. When JPMorgan’s Samik Chatterjee asked directly to quantify the backlog and when OCS reaches $100M/quarter, Anderson provided no numbers. He said they would “probably give some more specific milestones as we progress through the year.” Compare this to Lumentum, which disclosed $400M+ OCS backlog, shipping timelines for H1 2027, a $10M run rate already achieved, and a CY26 exit rate above $100M/quarter. Coherent is asking the market to “trust me bro” while Lumentum provides a spreadsheet. For a liquid crystal technology that still needs to prove its competitiveness against MEMS on insertion loss, the lack of hard numbers makes me think that their OCS kinda sucks.

Conclusion

In my opinion, this is a sleeper quarter. All three pre-earnings themes strengthened.

6-inch InP yield ramp: strengthened. The yield story now has cost math behind it. Management confirmed 6-inch production costs roughly half of 3-inch, a quantification number we didn’t have before. And essentially all new capacity being added is 6-inch, not 3-inch. If 6-inch wasn’t working, they wouldn’t be exclusively building 6-inch lines. They are betting the entire capacity expansion on this technology. That tells you everything about where yields actually are.

Supply chain positioning / capacity ramp: strengthened. Wafer starts are at 80% of the doubling target, ahead of schedule. But wafer starts take ~6 months to become transceiver shipments. The FQ3 guide — the one the market sold off on — reflects capacity started in September/October, when 6-inch was barely getting going. The current quarter’s aggressive ramp won’t show up in revenue until June and beyond. This is the alpha: the guide is constrained by yesterday’s capacity, not today’s. As 6-inch wafers flow through the P&L over the coming quarters, the gap between what the market expects and what Coherent can actually ship should widen. Expect larger beats in H2.

CPO/OCS: net strengthened. We went 1 for 2 on this one. CPO went from sampling to a massive purchase order in one quarter — the single biggest change Q/Q and earlier than I expected. I’ve pulled in my CPO estimates by one year. Lumentum’s market cap is approaching Coherent’s, and arguably half or more of LITE’s valuation is CPO. If Coherent captures even a fraction of CPO share, the re-rating potential is significant. OCS was a loss — two consecutive quarters of refusing to quantify backlog or revenue milestones, no demonstration of liquid crystal competitiveness vs MEMS. But a CPO win and an OCS loss is an acceptable outcome. At Coherent’s valuation, the majority of the equity value still comes from transceivers, not from OCS. You only need to win one, and they won the one that matters more.

Credibility issues remain: VCSEL persistence at 200G despite market criticism, OCS vagueness, and continued dependence on external EMLs from Lumentum. But this quarter qualified the thing that is most material to their valuation — transceivers on 6-inch InP — and proved the capacity is 80% of the way to doubling. The beats are coming. The market just can’t see them yet because the wafers haven’t shipped.

Is it still early to get in on this

Great analysis! The dcfmodel.ai website is also pretty neat man.