Coherent | Earnings Review: The Sleeper Print

I think the market is wrong (?) The forgotten child of the optics family may actually have a comeback.

Opinions are my own and do not represent past, present, and/or future employers. All content is based on public information and independent research. This newsletter is not financial advice, and readers should always do their own research before investing in any security. I am invested in the semiconductor industry. As of the date of this publication, I currently hold a long position in Coherent Corp. (COHR). Feel free to reach out at jasonschips@gmail.com.

I built a tool using Claude Code to automate DCF valuation.

Pre-Earnings Vibe Check

(This section was written prior to the earnings call to communicate the prevailing narratives and provide a contrast to post-earnings sentiment)

Lumentum reported last night. They had a crazy beat on the raw numbers, especially for gross margin, revenue guide, and operating margin guide. They confirmed what the optical supply chain has been signaling for months: the industry cannot make enough lasers. EML supply-demand gap widening, 1.6T adoption accelerating, 800G still growing underneath it.

Coherent is generally seen as an inferior version of Lumentum.

COHR has rallied on the optical revisions, but nowhere near as much as its peer. They are still tryna qualify CPO lasers, make lower-quality EML, and their OCS approach (liquid crystal) is gaining less traction than Lumentum’s MEMS. However, what they have that Lumentum doesn’t is massive scale, able to ship 5-10x the transceiver volume.

Three narratives to watch:

1) 6-Inch InP Yield Ramp — the margin inflection story. Coherent’s 6-inch InP wafer fab became fully operational this quarter. In theory, 6-inch lines offer materially superior yield and output vs traditional 3-inch.

Like think about it.

BIG CIRCLE PRINT MORE SQUARE

In practice, initial yields are lower as expected during early production. The question tonight is how fast the learning curve is progressing. If yields come in ahead of plan, Coherent moves toward EML self-sufficiency, meaning it buys less lasers from Lumentum which has been the bain of their existence recently. This is the single most important variable for Coherent’s margin trajectory over the next 12 months.

2) Supply Chain Positioning — the demand-overflow-capture story. Coherent is vertically integrated across critical optical components (isolators, Faraday rotators) and is internalizing EML and CW laser production. It is U.S.-based, which matters as hyperscalers diversify supply chains away from Chinese transceiver vendors like Innolight. The industry is extremely constrained and Lumentum falls further behind demand every quarter. Where is all that excess demand gonna go?

Coherent plans to double internal InP capacity within the next 12 months, driven by 6-inch wafer lines in Texas and Sweden — a far more aggressive expansion than Lumentum’s 40% target that still has a 25-30% supply shortfall. This is a company building itself into the excess demand absorption machine for an industry that can’t make enough lasers.

3) CPO/OCS Disadvantage. Coherent hasn’t rallied as much as Lumentum because it lacks the same CPO and OCS credentials. On OCS, Coherent’s liquid crystal approach offers better reliability and scalability than MEMS but suffers from significantly higher insertion loss, and adoption trails Lumentum’s MEMS switches by at least two quarters. On CPO, Coherent has not yet qualified its CW lasers with any customer, let alone demonstrated the yields needed for commercial mass production. So very expectedly, COHR is the unloved child that trades at a discount to LITE. However, any progress here is currently unpriced. If Coherent can close either gap, ohhhhh boy. Get strapped in.

The Print

I was kind of shocked at how little info Coherent provides on their initial press release.

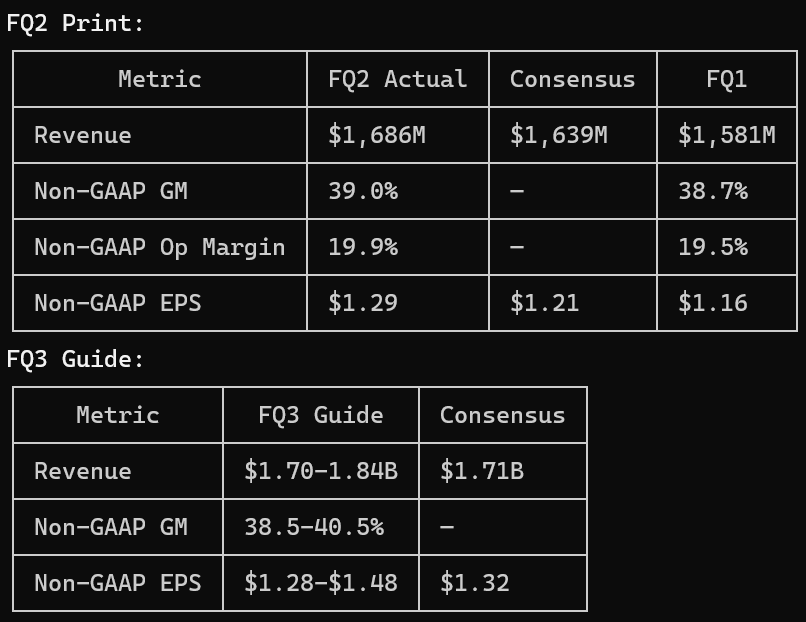

Behold my Claude Code terminal table (again):

The past quarter’s actual was fine. Revenue beat by 3%, EPS beat by 7%, gross margin expanded 24 bps sequentially. All lines above expectations. Not a blowout, but solid execution across the board.

The guide is where the market got disappointed. Revenue midpoint of $1.77B is only 3.5% above consensus and probably far below buyside whisper numbers. EPS midpoint of $1.38 is 4.5% above. Compare that to Lumentum guiding 18% above consensus on revenue and 24% above on EPS.

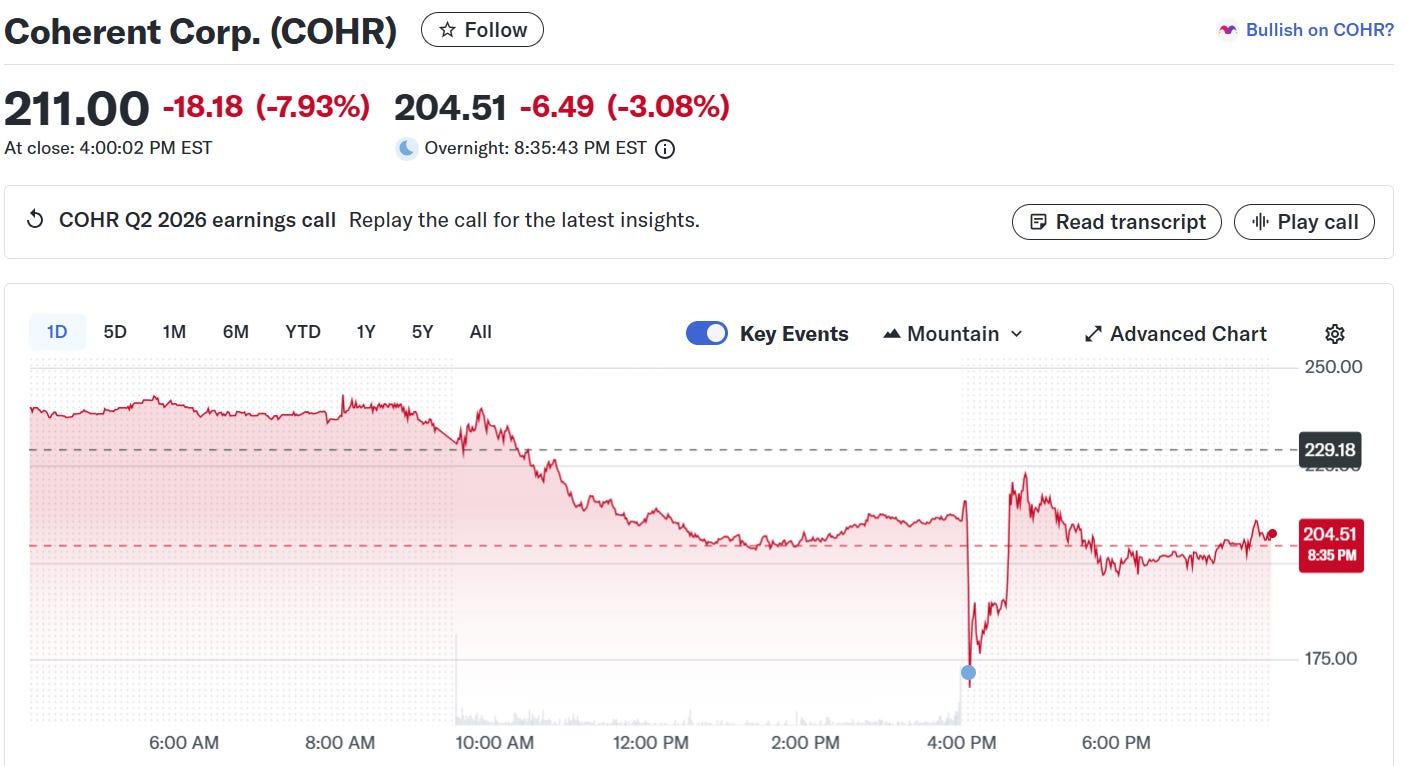

And they had some crazy whipsaw price action.

I must confess I traded this terribly and lost a lot of money. I panicked on the initial print and sold part of my position when it was down 20% at $172.

Then the call started and right when the right keywords hit my ears, I bought back… at $219. Yes you read that right.

Never trade an earnings call. No one has had time to digest information or make revisions. I ended up donating money to Jane Street robots. Take this as a lesson, dear reader. (but not as financial advice)

The Call

Now I just want to say. Once I locked in and started really digging into this transcript, I actually found it a fascinating quarter. I was a bear on the initial print, but the call flipped me from bear to bull very steadily throughout the 60 minutes. I think this is the kind of result that is prone to be misinterpreted for days after. There are several subtle details management pointed out on the call that act as “forcing functions” that lead me to believe they will post much larger beats 2 quarters from now. As you will see in my conclusion, this is a sleeper print.