Computex 2026 Review (ft. Lumentum & the CPO Endgame)

Jason's Chip Trip. Computex from an investor's POV. Lumentum to the moon.

Sorry if my posting frequency is down this week. I went on a chip trip to Taiwan.

This is the view from the top of the Taipei 101. It’s really a beautiful city.

Anyways Computex basically takes place inside of this building and there’s a whole bunch of booths and it is an absolute meat fest (very packed).

There was a ton of alpha to be found by looking at the racks and talking to the various interesting people at the booths.

We will first highlight various interesting exhibits from investors POV. We will then talk about CPO. The main takeaway I’ve had is the end-state of scale-up CPO (and it is incredibly important!)

Contents

Immersion Cooling

Fuel Cells

Hiwin (Robotics Supplier)

DRAM

Kyber Racks

Astera Labs

Nvidia RTX Spark (Laptops)

MediaTek MicroLED

Scale-Out CPO

Scale-Up CPO, Takeaways for Stonks, and Lumentum EPS

SemiAnalysis Giveaway: The first person to subscribe using the paywall on this post will be selected to receive one free month of SemiAnalysis (sent to your email).

By accessing this content, you acknowledge and agree to our terms and conditions. This research is not financial advice.

Immersion Cooling

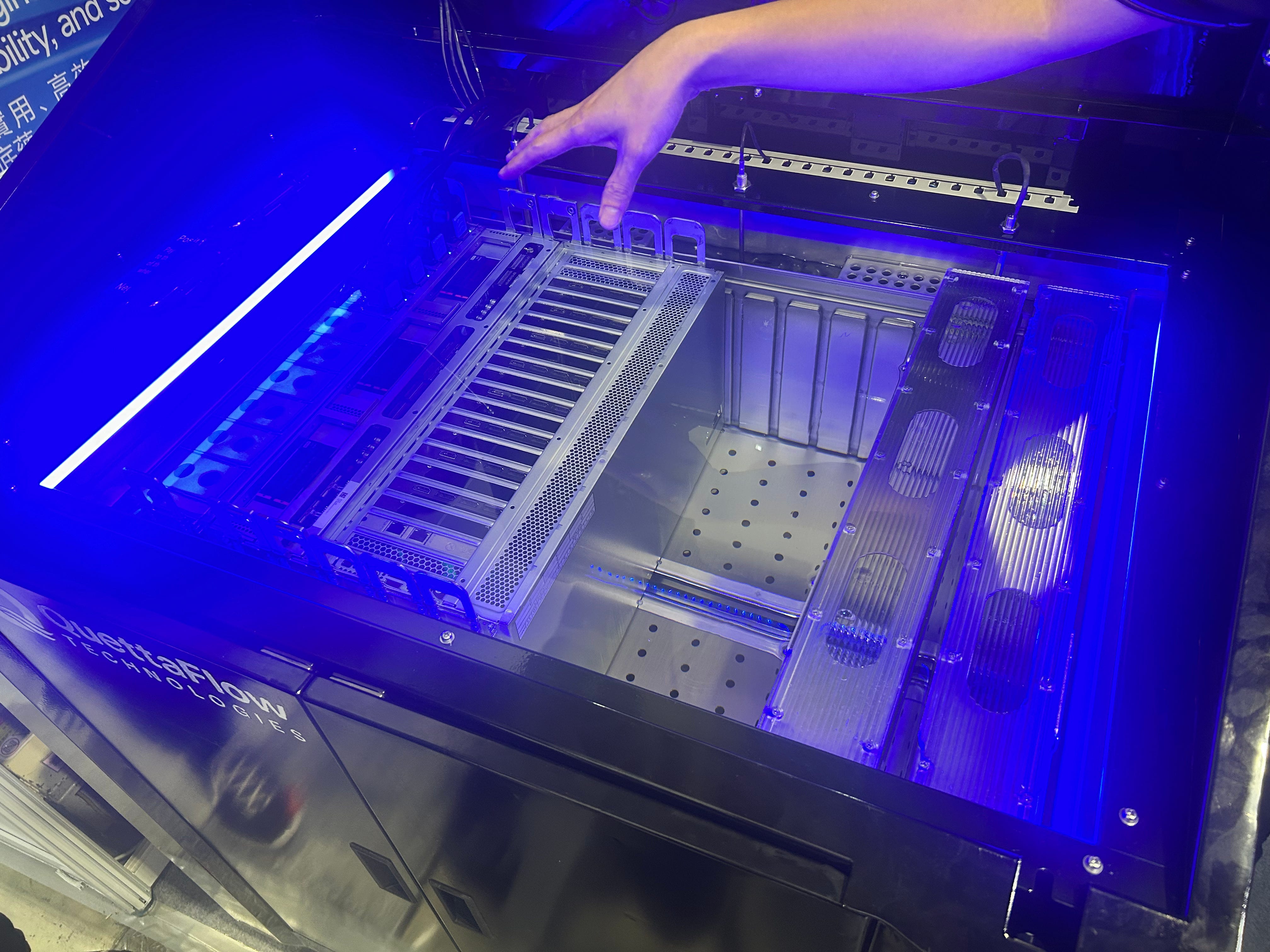

There is this company called QuettaFlow that literally submerges GPUs in liquid to cool them.

Isn’t that so sick?

Unfortunately, you can’t put an NVL72 rack in this liquid, as you may imagine. This is only for small chunks of compute, so basically enterprise on-prem.

The liquid isn’t water (duh). It is a non-conductive fluid that is a by-product of oil. You can plug stuff into the rack while it’s submerged. I actually touched it. It is very oily and greasy.

The benefits are that it is much cheaper (40-50%), much more compact (no IT room or raised floor), and saves a ton of electricity.

They’re private, of course, but fascinated to see where this tech can go.

Fuel Cells

Funny story.

We were at the Vertiv booth and asked the guy there about this 800VDC power module and what it does.

It is a combined transformer and rectifier that turns AC medium voltage from the grid into 800 VDC.

This is very big and expensive. I think they said like $3M ASP.

So we asked the guy, “What if you just had 800 VDC natively? Then you wouldn’t need this box, right?”

He said “Well, where would you get that?”

LOL

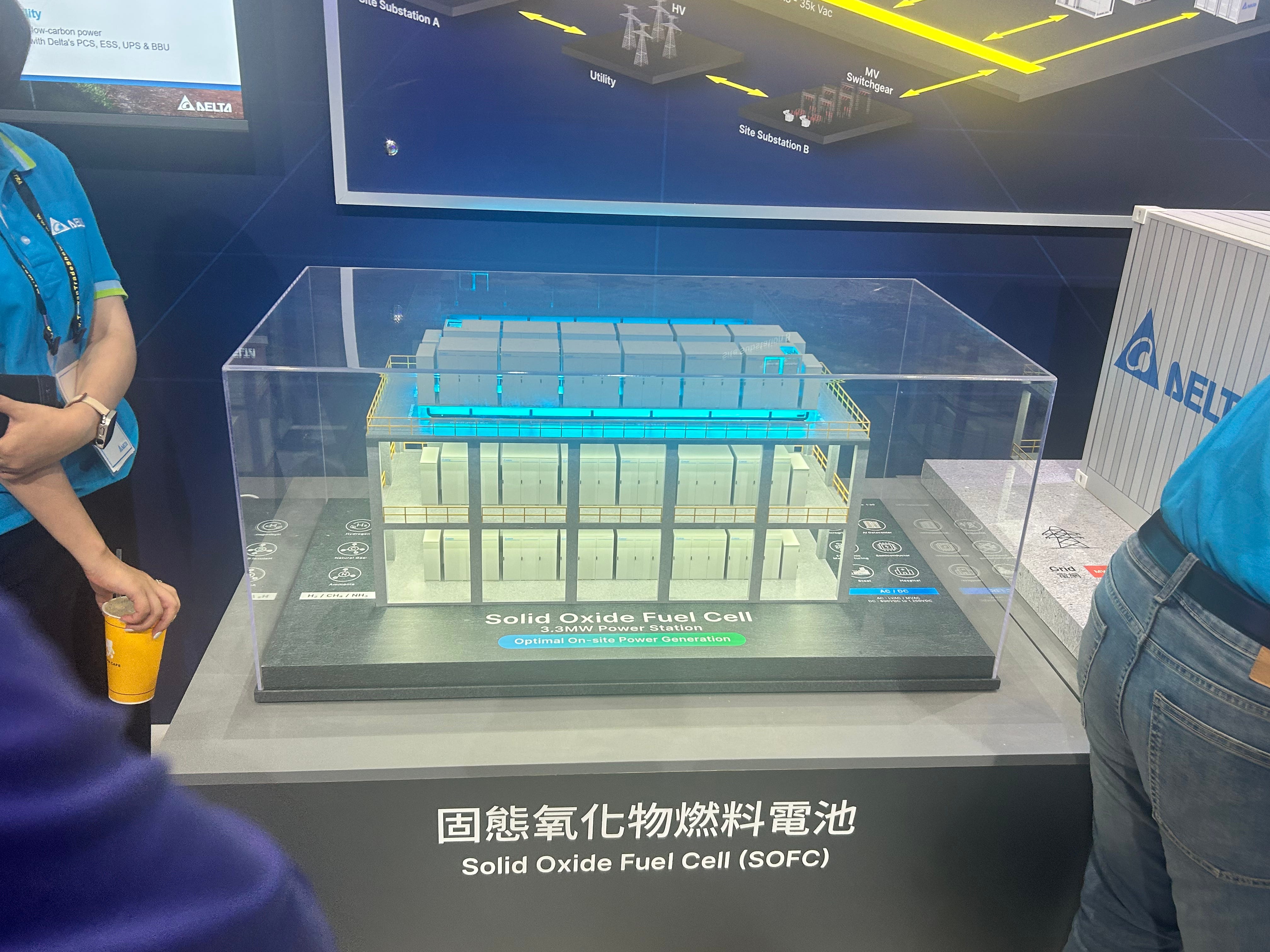

Then we visited a booth for a company called Delta Electronics. They are competitor to Vertiv and Schneider. Basically, liquid cooling and stuff.

But did you know that they also have an SOFC solution?

Unlike Bloom, which uses ceramic plates, Delta licenses Ceres’ IP, which actually uses steel. Obviously specs are inferior to Bloom currently, so it’s more of an overflow capacity play.

They are currently shipping small volumes (30 to 50 MW) and installing them in Taiwan. They’re not fully independently scaled commercially, also, as the purpose of these fuel cells is more to provide a full portfolio of power solutions complementing their Vertiv-like products.

Ticker is 2308 on the Taiwan exchange.

Hiwin (Robotics Supplier)

Hiwin is a Taiwanese screw maker that supplies into robotics. They make actuators (components that help robots move). Did you know that actuators actually make up most of a robot’s BOM?

Interestingly, most of their sales are actually to North America, to companies like Tesla. This is important because a lot of this stuff comes from China, so American companies would find suppliers like this very attractive as a geopolitically safe option.

In the middle is their best component, which is a linear actuator. They are better (higher ASP, less commoditized) than the rotary ones on the sides.

I looked into them a bit further. Turns out that 50% of their sales are actually to the semis market. So yeah, here’s a company that has exposure to both robotics and semis. If you are interested, the ticker is 2049 on the Taiwan exchange. However, as you might imagine, screws are quite commoditized. They only have about 10% market share. LOL. And they trade at 40x multiple on sell-side estimates. I honestly would have expected a way lower multiple for a business like this.

DRAM

How to invest in semis 101:

Look at the PCB.

Identify what has the most surface area.

Buy.

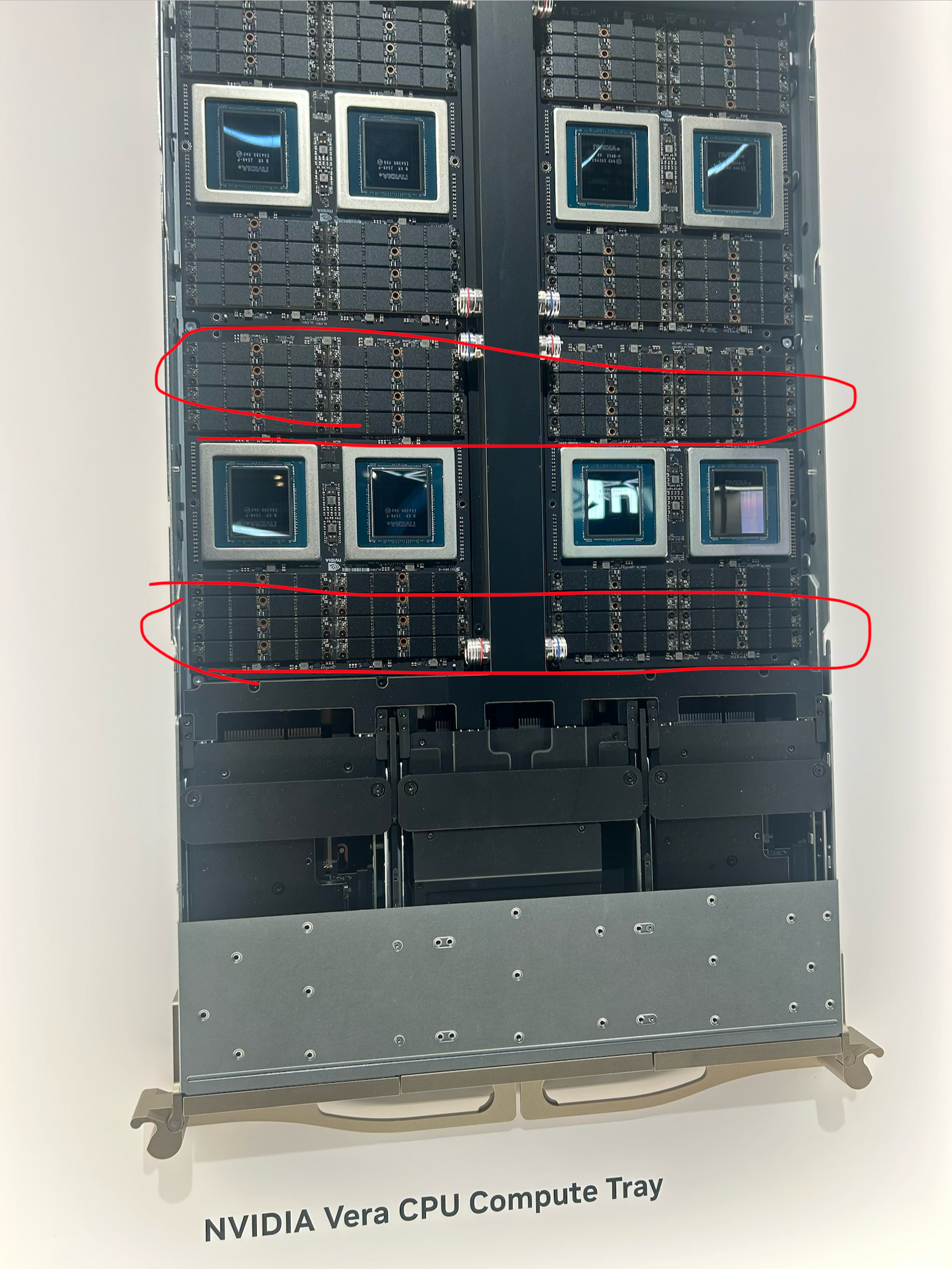

One recurring theme that I noticed is how literally every single tray that you see at Computex has a shit ton of DRAM. It sounds obvious, but you really need to see it for yourself to intuitively grasp how much DRAM is in everything.

For example, this is the Vera CPU compute tray.

Those SOCAMM modules are stacked too, so it’s actually even more surface area than it appears to be.

Being bullish on CPU proliferation for agents is almost just as much bullish on DRAM. As it would drastically increase the total base of compute (accelerated or not) to which memory is attached.

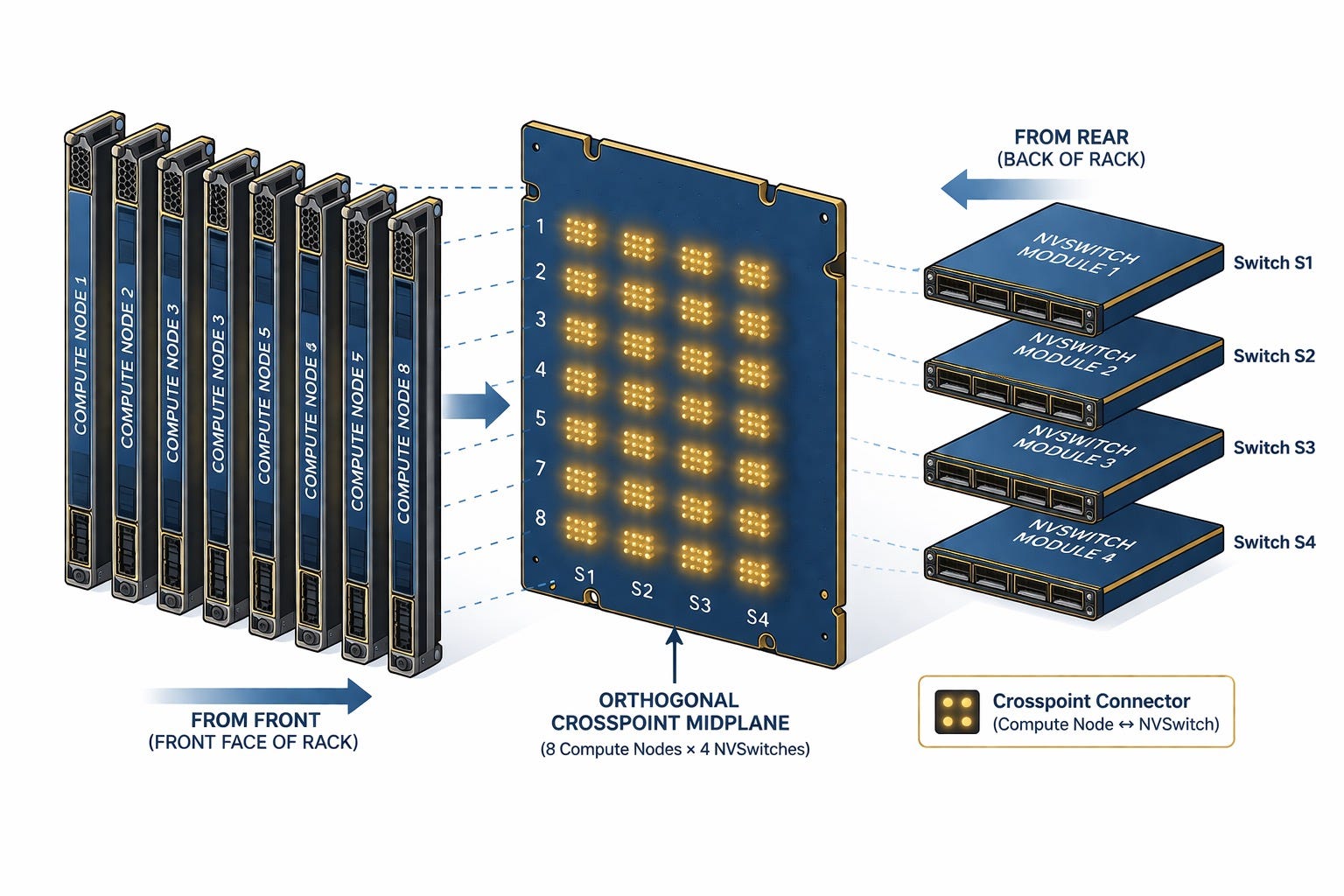

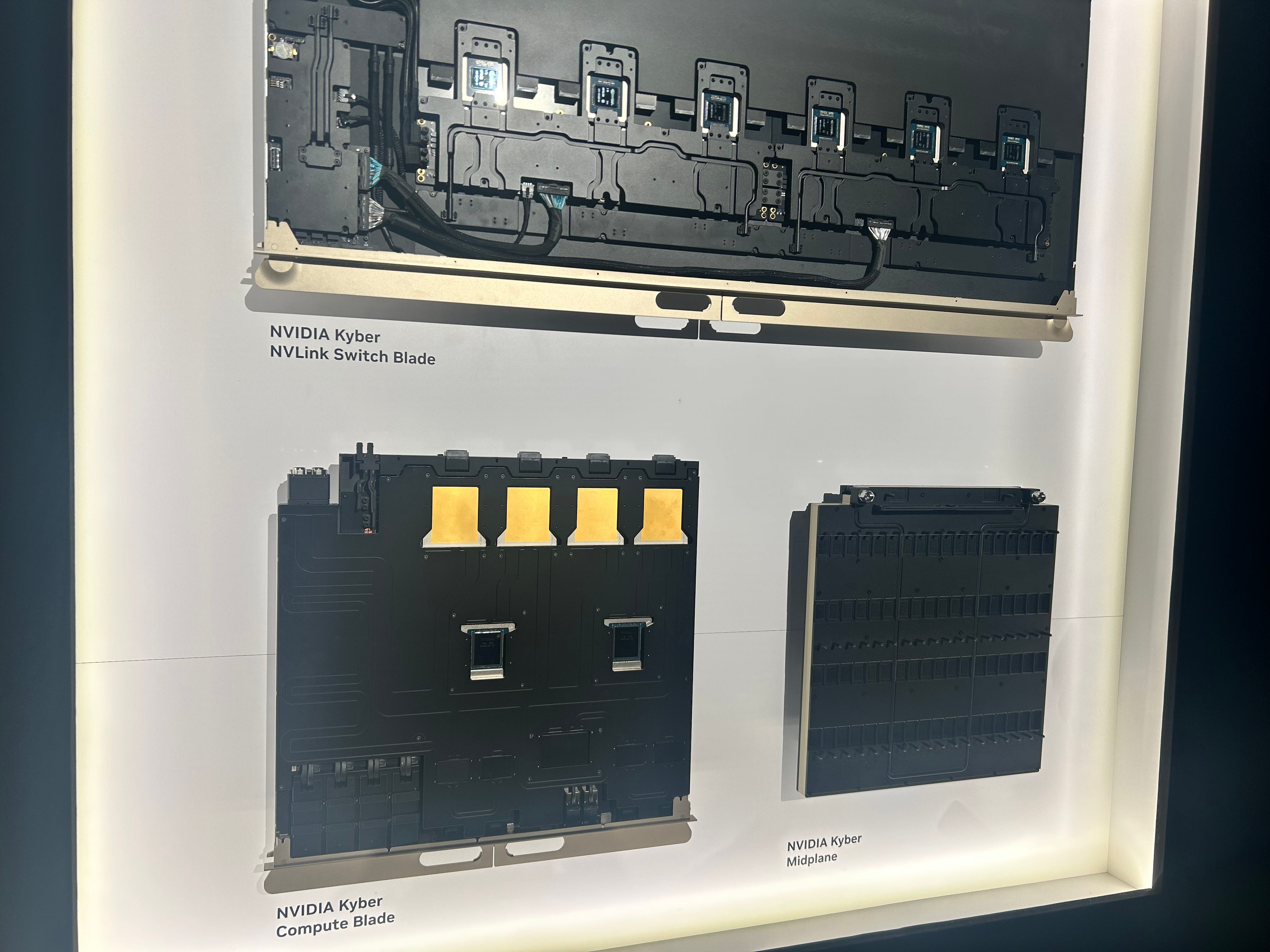

Kyber Racks

Kyber racks are so cool.

GPUs go in vertically from the front. NVSwitch modules go in horizontally from the back. They meet in the middle via orthogonal midplane. Super compact! Save space!

This means you can fit 144 GPUs in one rack. It’s very beautiful and elegant. There are no cables, either.

However, the volumes at which they can actually be shipped for Rubin Ultra are constrained by the supply chain. Kyber racks require high-grade (M9) CCL (copper-clad laminate), because the per-lane rates are increasing, the layer counts per tray are increasing, and the cableless design pushes these signals through the midplanes and orthogonal backplanes, putting even more pressure on the CCL for M9 CCL. Traditional glass fiber won’t cut it. You need quartz fiber, which is much harder to manufacture and whose supply chain is much less mature.

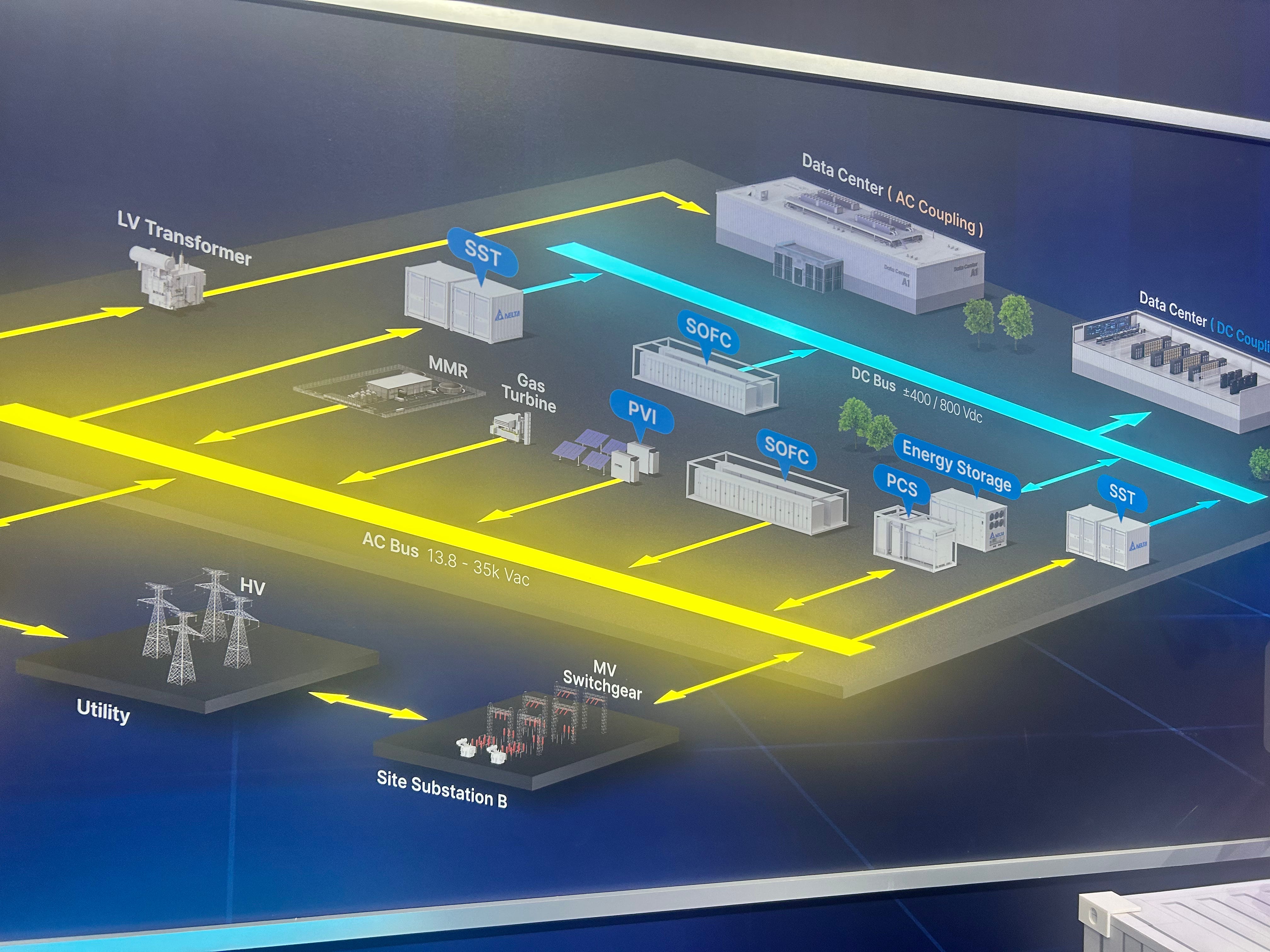

If it does ramp, this has significant implications for future data center design. If data centers become much more compact, 800 VDC might be able to span the whole shell without needing to go through lossy transformer and rectifier steps (800 VDC cannot travel long distances). This is incredibly bullish for Bloom, as they output 800 VDC natively. Meaning that the TCO of a fuel cell becomes materially more competitive if smaller form factor racks and data centers get wider adoption. This deserves an entire article of its own.

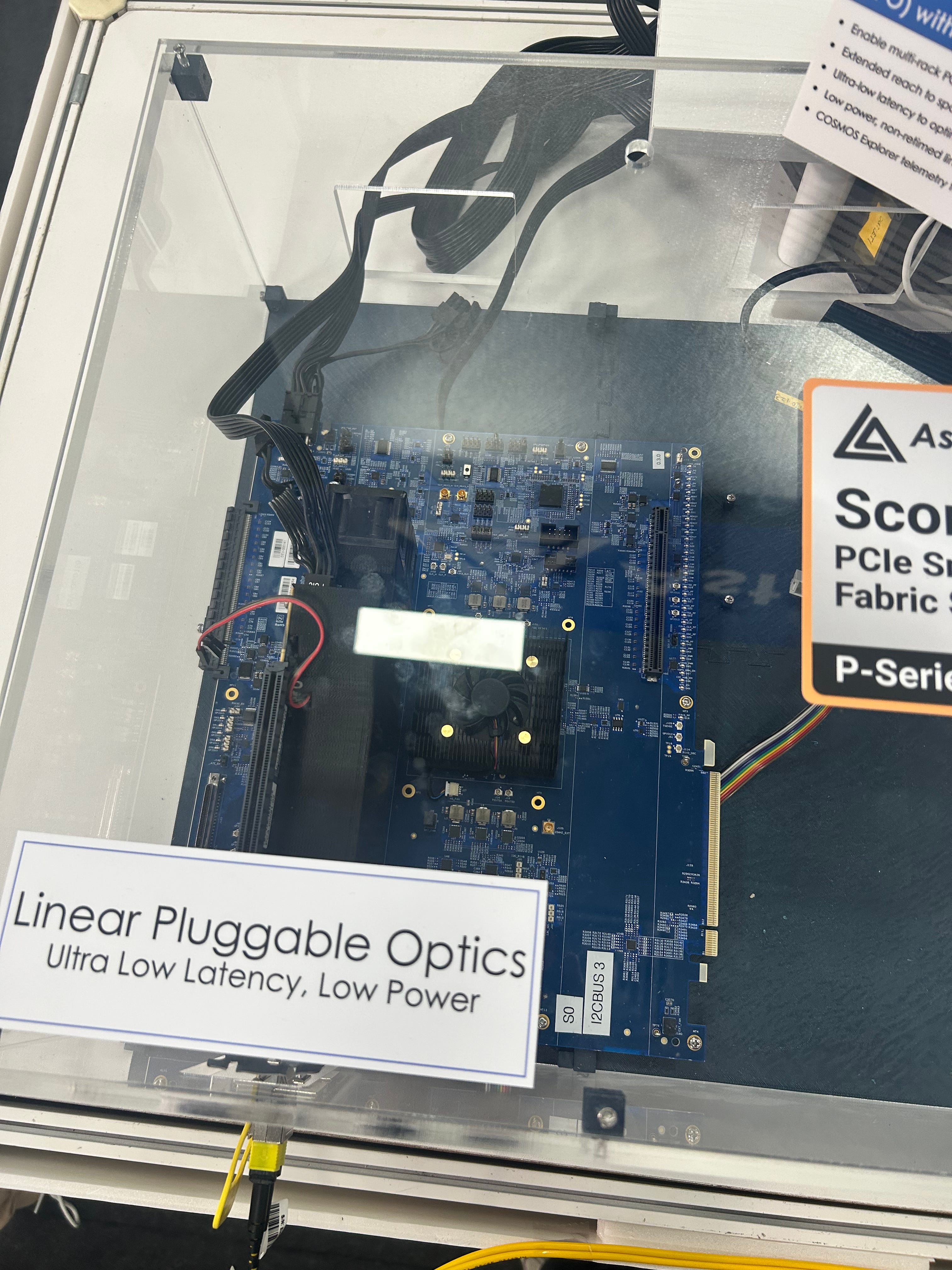

Astera Labs

Asteria Labs makes connectivity chips, like retimers (which are chips that clean up signals and retimes it to the clock) for copper communication (CXL and PCIe).

Astera Labs is a huge Trainium supplier. The 2025 10K says that one customer was 70% of revenues. I wonder who that is!

(This is also why Astera is Gavin Baker’s biggest position. Gavin is a believer that Trainium is an even better ASIC than TPUs.)

Think of Trainium as the Amazon basics of XPUs.

They are literally air-cooled and also use PCIe for scale-up like regular computers. Sometimes I am flabbergasted that compute which doesn’t use NVLink… works.

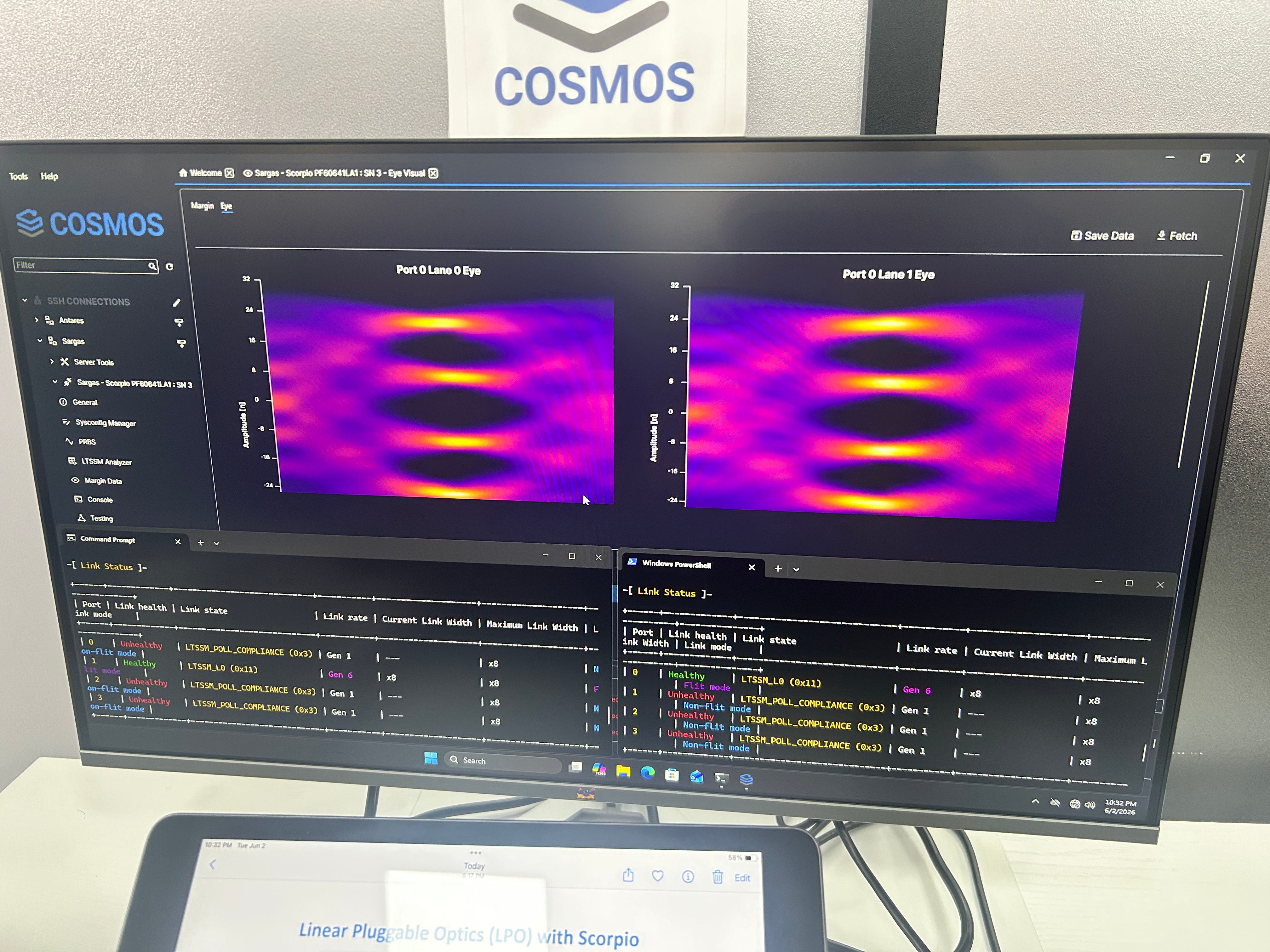

But did you know that Astera Labs actually has an LPO solution?

(An LPO is just a transceiver without a DSP. Think of it like the transceiver is to LPOs as an AEC is to passive copper.)

They don’t actually make the LPO module itself. They sell the LPO switch ASIC and the software that modulates the SerDes signal.

This can be used for PCIe scale-up!

An LPO has the same latency as passive copper DACs because there is no retiming. Compare that with an AEC, which has active data processing components. It is pretty much strictly better, as the LPO can reach up to 50m while the DAC fails within a few.

Here is an eye diagram (PAM4, you can tell because there are three eyes).

I have no opinion on this stock besides that it is a good tracker for Trainium capex.

Nvidia RTX Spark (Laptops)

Nvidia’s new agentic laptops. The only thing I have to say here is that isn’t it so weird that they are turned off and facing away from the crowd? I wanted to try them, but they don’t even work. This is just fueling more criticism of their ARM + Windows design.

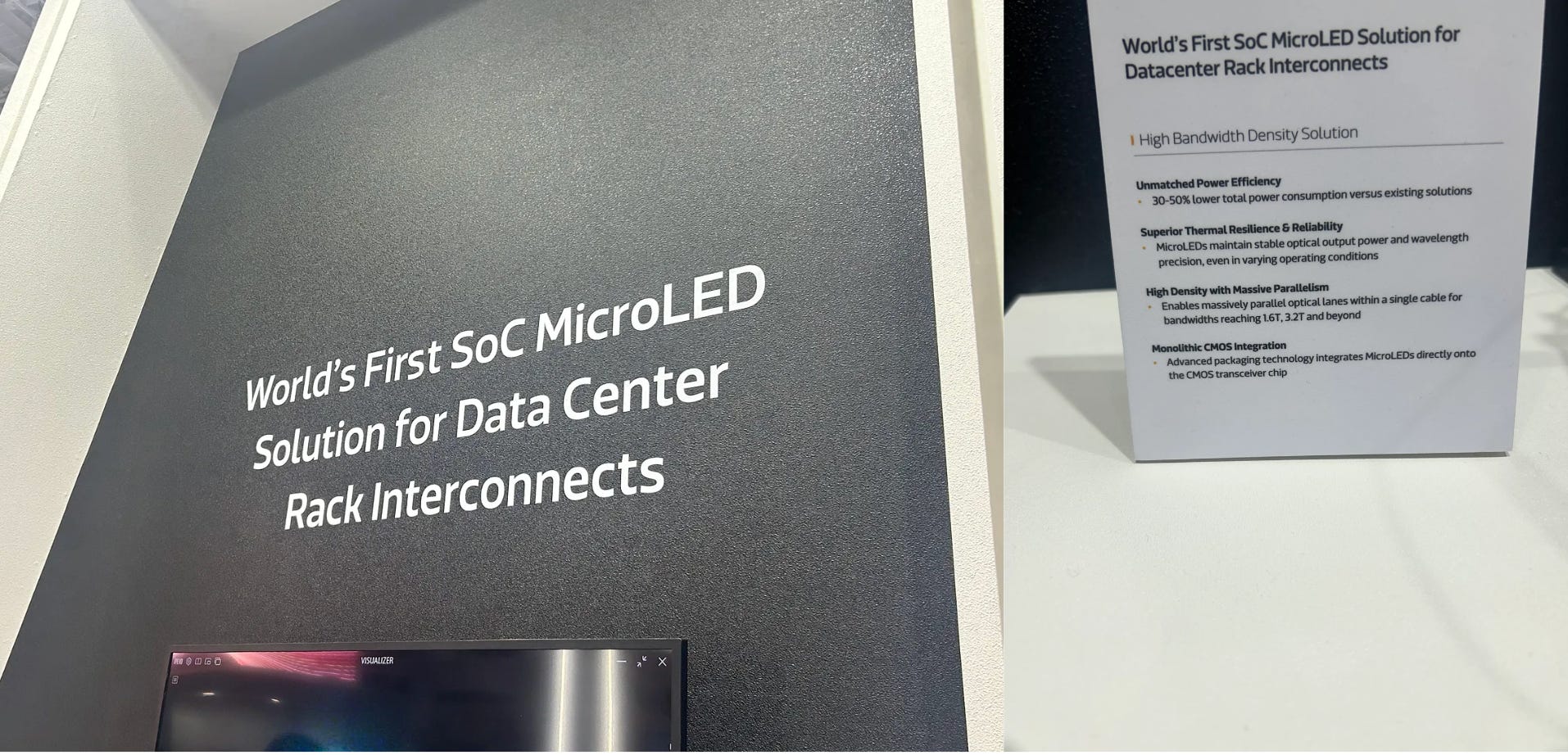

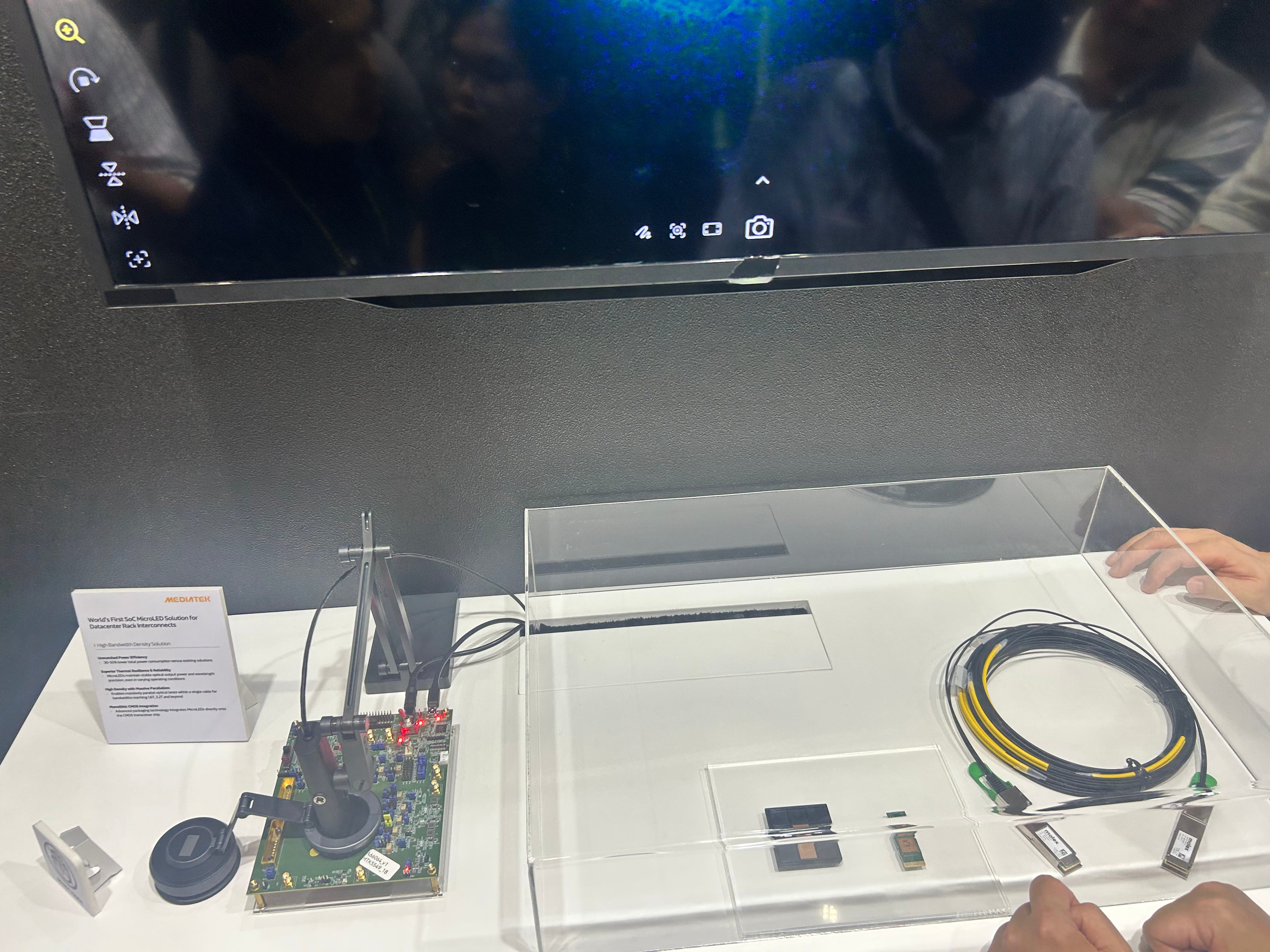

MediaTek MicroLED

For some reason, MediaTek is obsessed with microLED for scale-up CPO. When I was at their booth, a ton of space was dedicated to this (very widely hated) solution while their custom ASICs weren't present at all.

Interesting.

Micro-LEDs are an alternative to lasers. A lot of photonics engineers don’t like them because laser light is basically very concentrated (coherent, highly directional) and it is also a single wavelength (linewidth anyone?) while LED light is very diffuse.

Like literally think about the LEDs in your house versus a laser that you can shine.

As a result, it is much harder for the receiver to pick up the signal, and thus you have much higher insertion loss and bit error rate. This is a pretty fundamental difference between the two technologies that is sort of glossed over in these booths.

But they do have a lot of claimed advantages. They are much more power efficient, have superior thermal resilience and reliability, and can be integrated directly onto the CMOS transceiver chip.

Micro-LEDs are very short-reach. I was at the Molex booth, which is an ODM for micro-LEDs, and they said that it only reaches up to several meters, meaning that this is a potential scale-up CPO candidate.

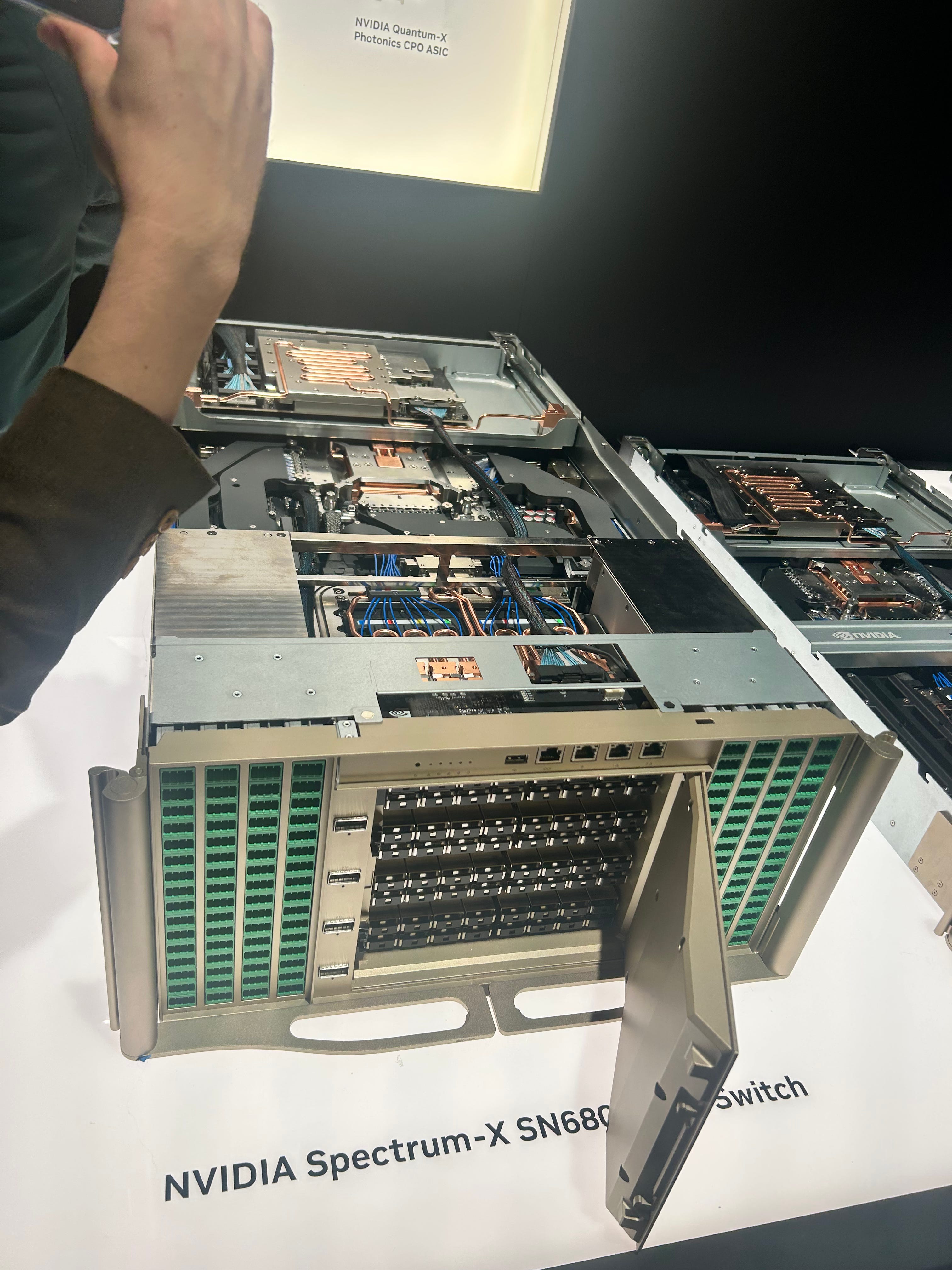

Scale-Out CPO

There are two types of scale-out CPO switches: InfiniBand (Quantum-X) and Ethernet (Spectrum-X).

Let’s start with the InfiniBand one.

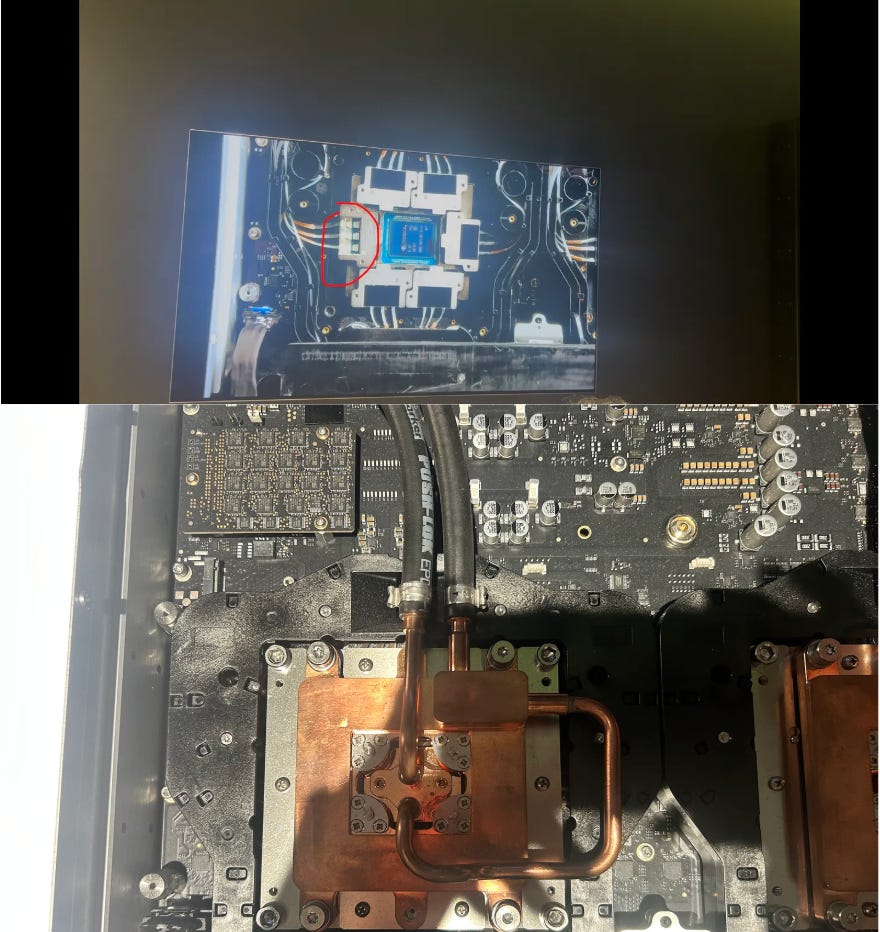

There are 18 ELS (external laser) modules (down on the bottom of top pic) and 4 switch ASICs with 18 optical engines surrounding each (see below, optical engines circled in red).

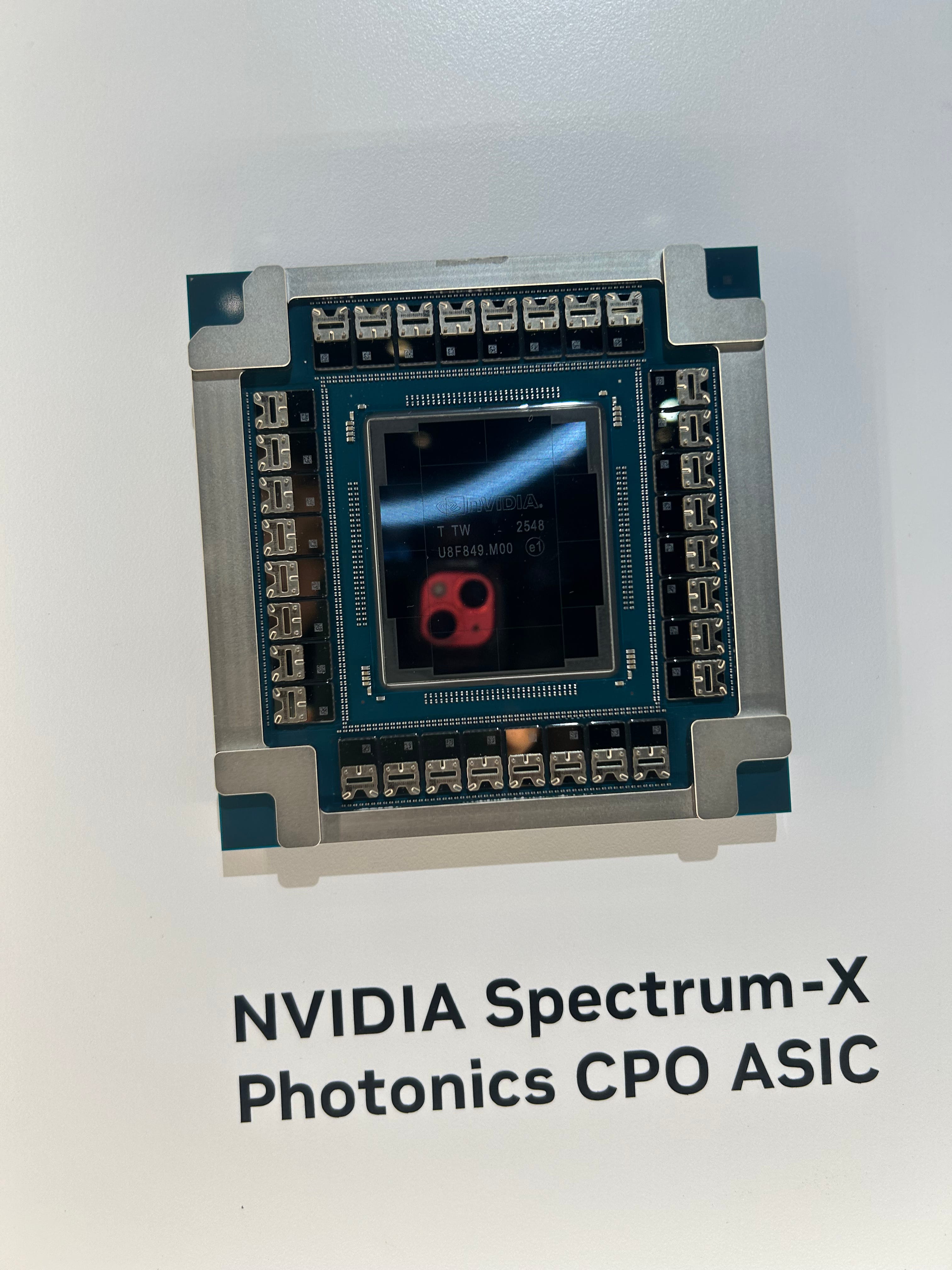

Now for Spectrum-X. There are 16 ELS… but only one ASIC!

That one ASIC has 32 optical engines around it. So less than 1/2 optical engines total, and 2:1 OE to ELS ratio rather than 4:1.

The ELS are also liquid-cooled, unlike quantum X where the ELS are air-cooled.

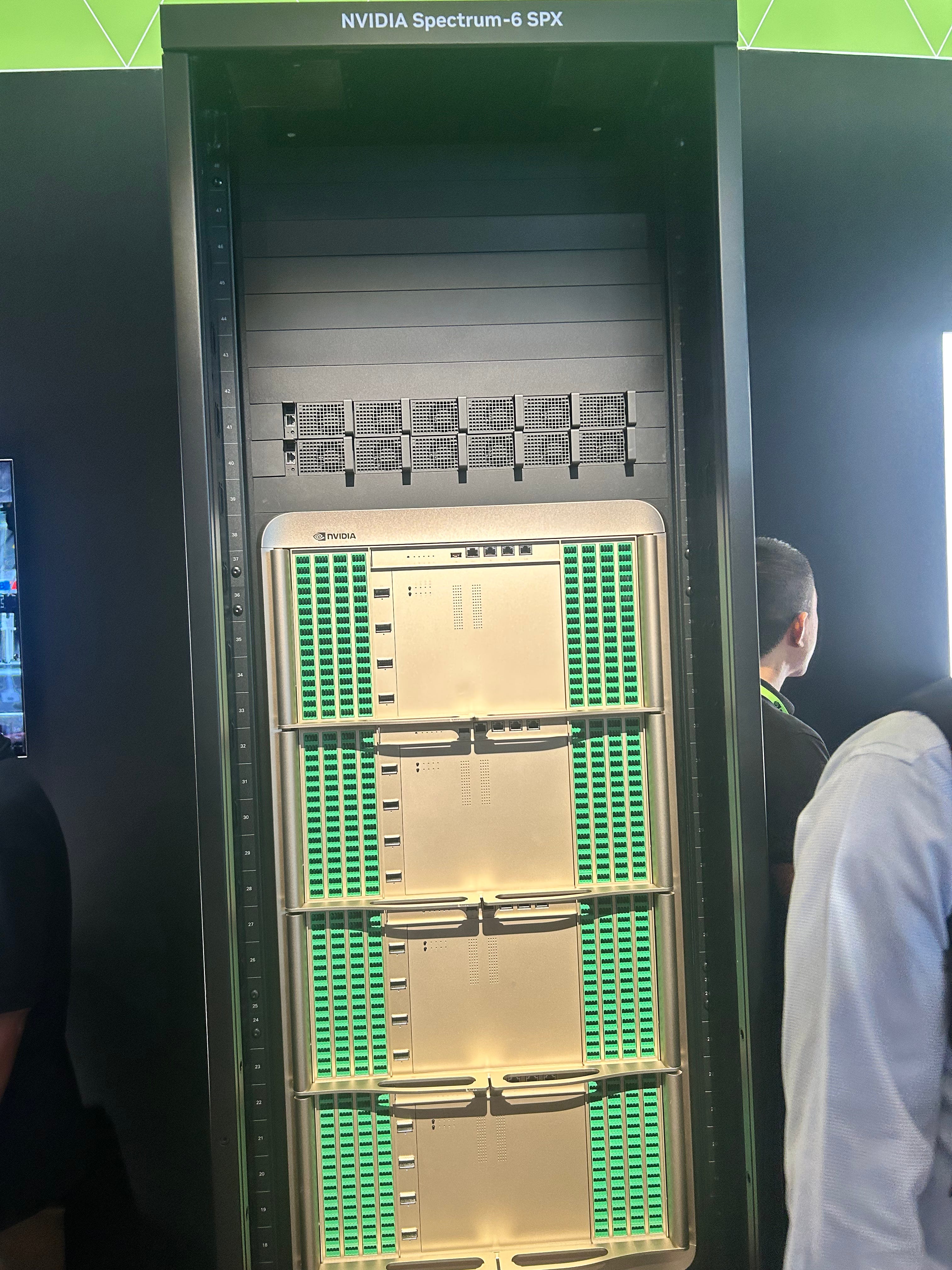

Here is the higher radix one. Basically 4 switches put together.

And the Spectrum-6 rack, which is four high radix switches put together (16 normal switches). This supports eight NVL 72 racks.

Scale-Up CPO, Takeaways for Stonks, Lumentum EPS

Below the paywall, we will discuss how my models (CPO ELS/OE builds) have changed after looking at Nvidia’s reference designs, the crazy mock scale-up CPO rack I saw (and the face-slapping implications for the scale-up CPO endgame I realized), and takeaways for optical stonks.

I will be providing the answer to the question I posed in this tweet.

We will be talking a lot about ratios and numbers and assumptions because small changes to these can either blow out or tank out-year revenues for optical companies.

And I will update my Lumentum model & EPS estimates.