Aixtron | Earnings Review: Incoming Tsunami of Revisions (Free Release)

Laser factories are buying lots of laser machines!!!

Opinions are my own and do not represent past, present, and/or future employers. All content is based on public information and independent research. This newsletter is not financial advice, and readers should always do their own research before investing in any security. I am invested in the semiconductor industry. As of the date of this publication, I may hold long or short positions in the securities discussed in this article.

Earnings Preview

Aixtron | Earnings Preview: Full Year 2026 Guide Incoming

Opinions are my own and do not represent past, present, and/or future employers. All content is based on public information and independent research. This newsletter is not financial advice, and readers should always do their own research before investing in any security. I am invested in the semiconductor industry. As of the date of this publication, I…

The Print

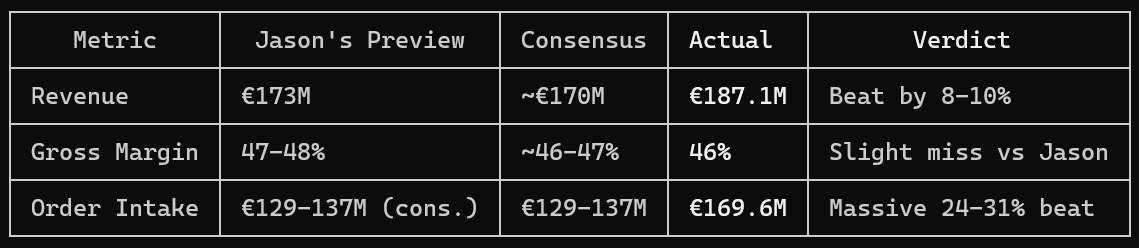

Actual Q4 results were very, very strong. Revenue came in way above consensus, even with weaker GMs. I don’t think this matters too much though.

The real leading indicator is backlog, and here we got exactly what we wanted. Orders €170M vs cons €130-137M (+25%). Seems like Lumentum and friends needed extra capacity, just like I predicted…

Now for the 2026 full year guide. Revenue missed by 10-20M, but it is perfectly in line with my model lmao.

Nothing much to report on in terms of the margins.

Also, FCF swung to +€182M from -€72M YoY. R&D also much lower than expected. I am not in the “cash is king” crowd, but you gotta appreciate this FCF generation.

Price Action

Today we continue our journey to a €50+ stock.

For my fellow fundamental analysts, a little lesson on technical analysis and price action.

NEVER TRADE AN EARNINGS CALL ON THE INITIAL PA.

Nobody can evaluate if a quarter was bad or good with only the PR and no call in seconds after it drops. There are no humans trading then. It’s all Jane Street bots and algorithms parsing natural language n shit.

Especially for a small cap low float stock like Aixtron, these algos can move the price very significantly. Your best bet is to ignore the price completely for the time in between the print and the call.

The Call

Optoelectronics

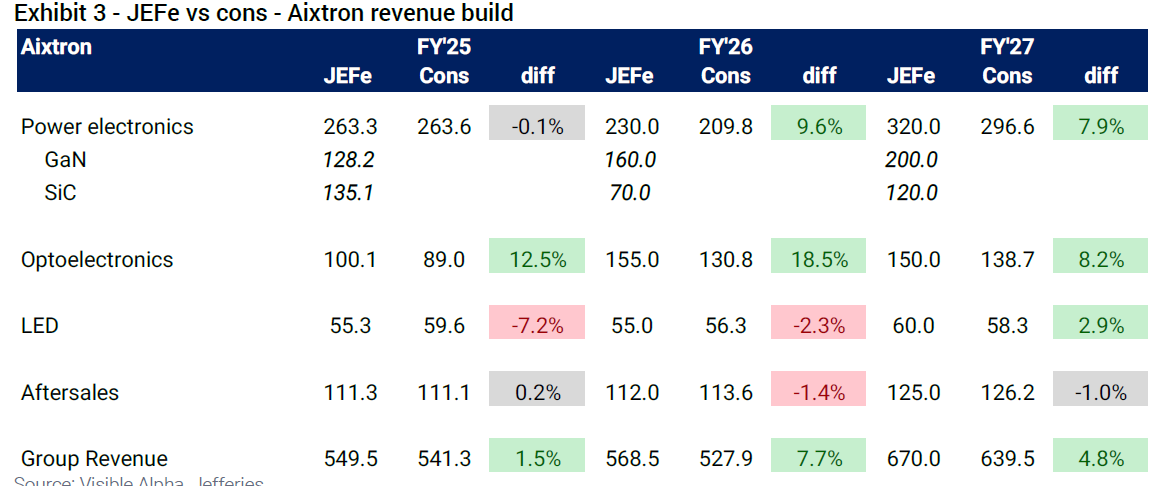

Before we actually talk about opto, let me level set you on what the sell-side thought about the scale of the opto opportunity, even after a bunch of them upgraded to buy.

JPMorgan:

Jeffries:

BofA (2022-2027):

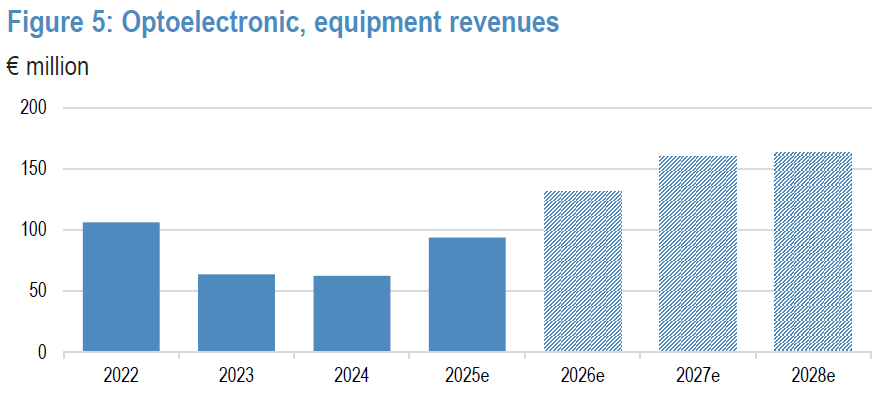

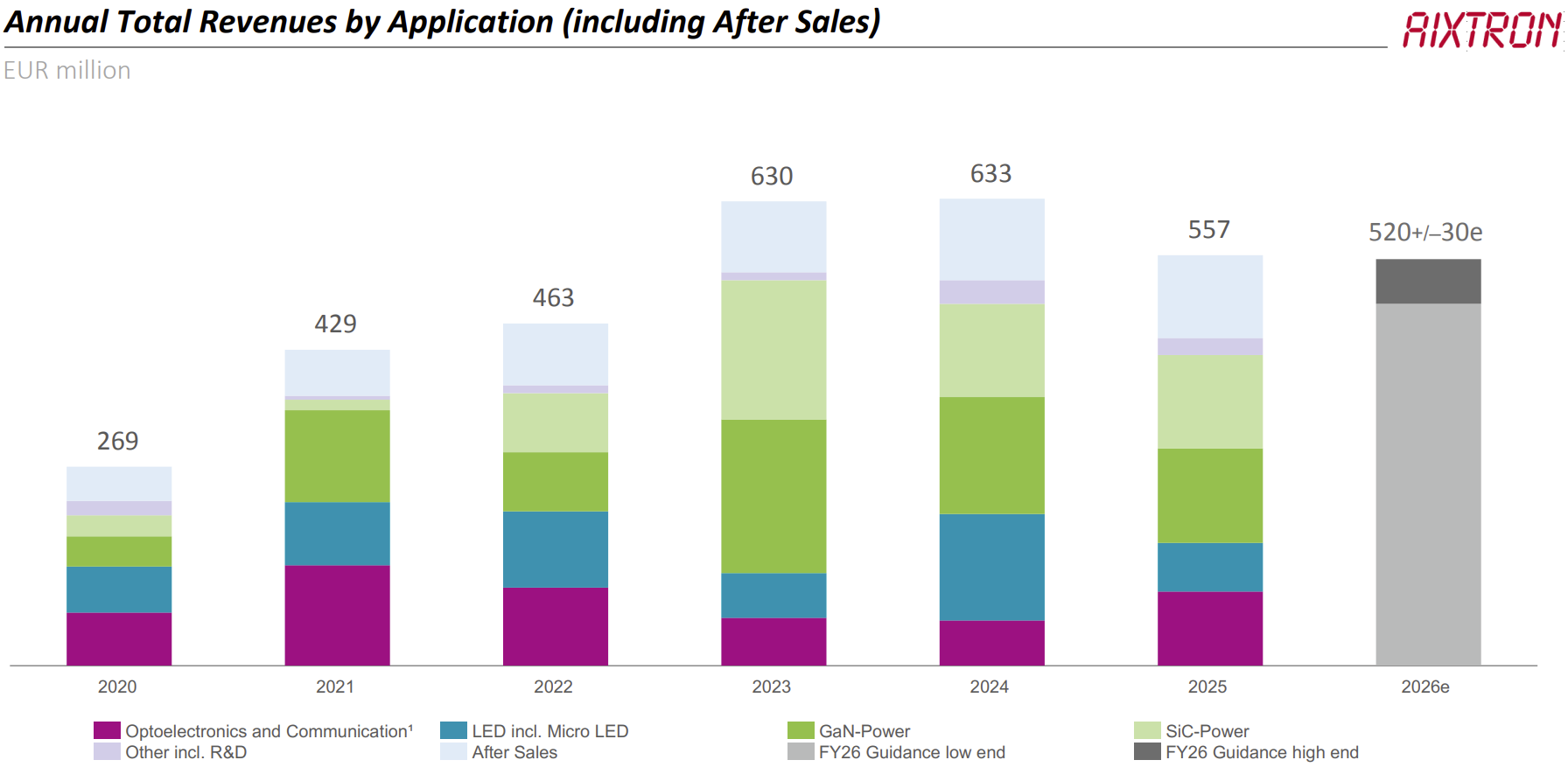

Aixtron’s 2025 equipment revenue (excl. aftermarket) came in at 445M, and Opto was 23% of it.

That means opto was 102M. Not bad, considering consensus estimated 89M. The Q4 beat was basically only driven by opto strength.

However, on the call…

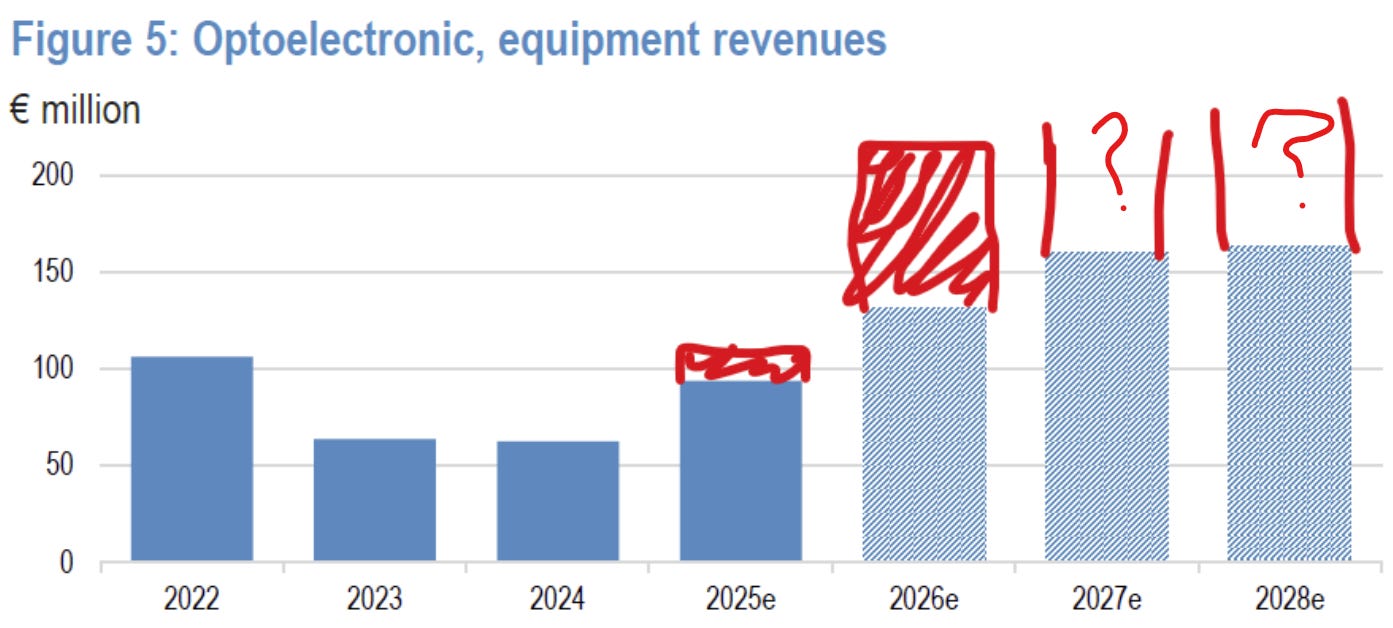

“Looking at demand dynamics, we expect the optoelectronics business to more than double year-over-year from 2025 into 2026. With this, it makes up for a large part of the revenue that declined in silicon carbide that I illustrated earlier.”

MORE THAN DOUBLE

MORE THAN DOUBLE

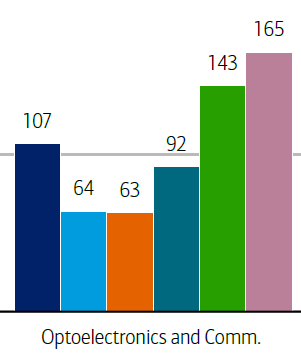

That’s over 200M in opto revenue next year. For context, this is what >200M looks like vs current consensus :)

Opto now represents 40% of Aixtron’s order backlog.

The cycle is also just getting started. The inflection was Q4 2025. Orders were low through Q1-Q3, then surged in Q4. Management confirmed €150M in Q1 order run rate and said they are “fully on track,” which means opto orders are continuing to flow as we speak.

On duration:

“This does not happen within 1 year. Now, to which extent and how large this will extend in 2027 and 2028, I think that’s the billion-dollar question I cannot quantify for you. Yeah? I am very convinced that we are not talking about 1 year, but at least about 2, and I would guess rather a 3 to 4-year time horizon.”

But he couldn’t quantify 2027 relative to 2026 — which makes sense. You can’t see the road if you’re sitting at the back of the bus.

Okay now let’s discuss moat.

“First, cloud services with a market share, we estimate well north of 90%.”

That’s a funny way of saying unbreakable monopoly.

Laser qualification is the stickiest of all Aixtron’s segments, and it’s not close. On the call, we learned that modern high-speed laser wafers see the tool three, four, five, or even six times during the manufacturing process. Epi layer, other processing steps, back into the tool, another epi layer, and so on. If something changes in the deposition and that change is repeated five or six times, the error compounds to the power of five or six. This is why qualifications take years, and why the G10-AsP — launched back in 2021/2022 — is only now achieving commercial momentum. Once a customer qualifies on your tool, they are not switching.

I want to address a question posed by an analyst I disagree with.

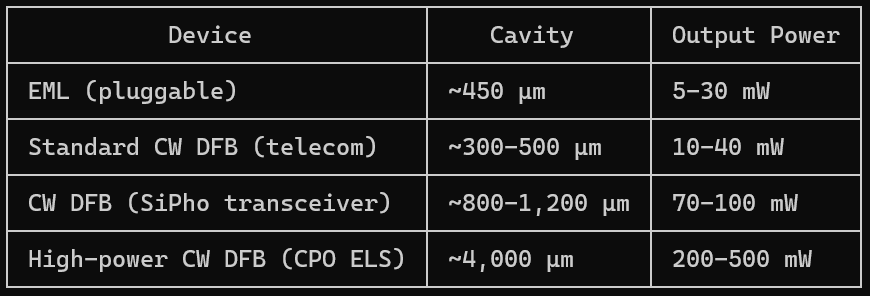

“From what I understand, the yields are something like 50%, and that the continuous wave lasers used in CPOs are about a tenth of the die size of EML lasers. I just wanted to hear your thoughts on how you think about the yield improvements, especially if the die sizes go down.”

This suggests less capacity is needed for CPO because you can fit more dies on each wafer. This is completely wrong and I’ll explain why.

The more power a laser uses, the larger its cavity must be. Though EMLs are complex structures, they use very little power, at only 5-30mW. The fat CW lasers needed in CPO are ultra-high-power, at 400mW, and therefore have a cavity size almost 10x larger. This is all confirmed in Lumentum’s CLEO 2022 paper.

Finally, on capacity:

“Honestly, it’s not relevant for the overall business or profitabilities. I would say capacity can always be scaled up in one way or another, yeah. Which way we choose to take, yeah, we will decide when we are there. I think it’s nothing that affects the P&L in one way or another. It’s not a constraint, it’s not a limit to us, it’s not a profitability limiter or inhibitor or whatever it is, it’s just operations.”

Why?

The Planetary reactor platform is modular, meaning the same parts, the same supply chain, and the same shop floor assembly used for SiC tools can be redirected to build opto tools. As Grawert put it, “the SiC customers were nice enough to step to the side.”

Lol. Thanks for stepping to the side, SiC customers.

SiC

The obvious drag on the business that is “putting a big hole in revenues” actually has a bullish nuance. This is all about 2027 and beyond, I’m literally modeling 40M of SiC revenue this year.

The overcapacity is cyclical, not structural. A year ago, SiC utilization was around 30%. Grawert laid out the recovery mechanism clearly: substrate prices have dropped significantly, which brings down the cost of SiC power devices, which makes them more competitive versus silicon IGBTs, which drives more design-ins and design wins, which increases unit demand, which gradually fills existing capacity, which eventually triggers new tool orders.

Then there’s actually structural growth. Two forces converge: the industry-wide transition from 6-inch to 8-inch wafers (starting with Western customers, now also in China, full shift expected 2027-2028) and the adoption of super junction SiC MOSFETs.

Super junction devices require multiple thin epi layers instead of a single thick one — the wafer goes through the tool three or four times using a multi-epi, multi-implant process. No tool upgrade needed, but epi time per wafer increases meaningfully, directly driving higher tool demand per unit of output. Grawert said Western players will “strongly embrace” this because it gets more dice per wafer and drives down cost per chip. When SiC comes back, it comes back with both a wafer size upgrade (necessitating an upgrade cycle) and an architecture change demanding more epi intensity.

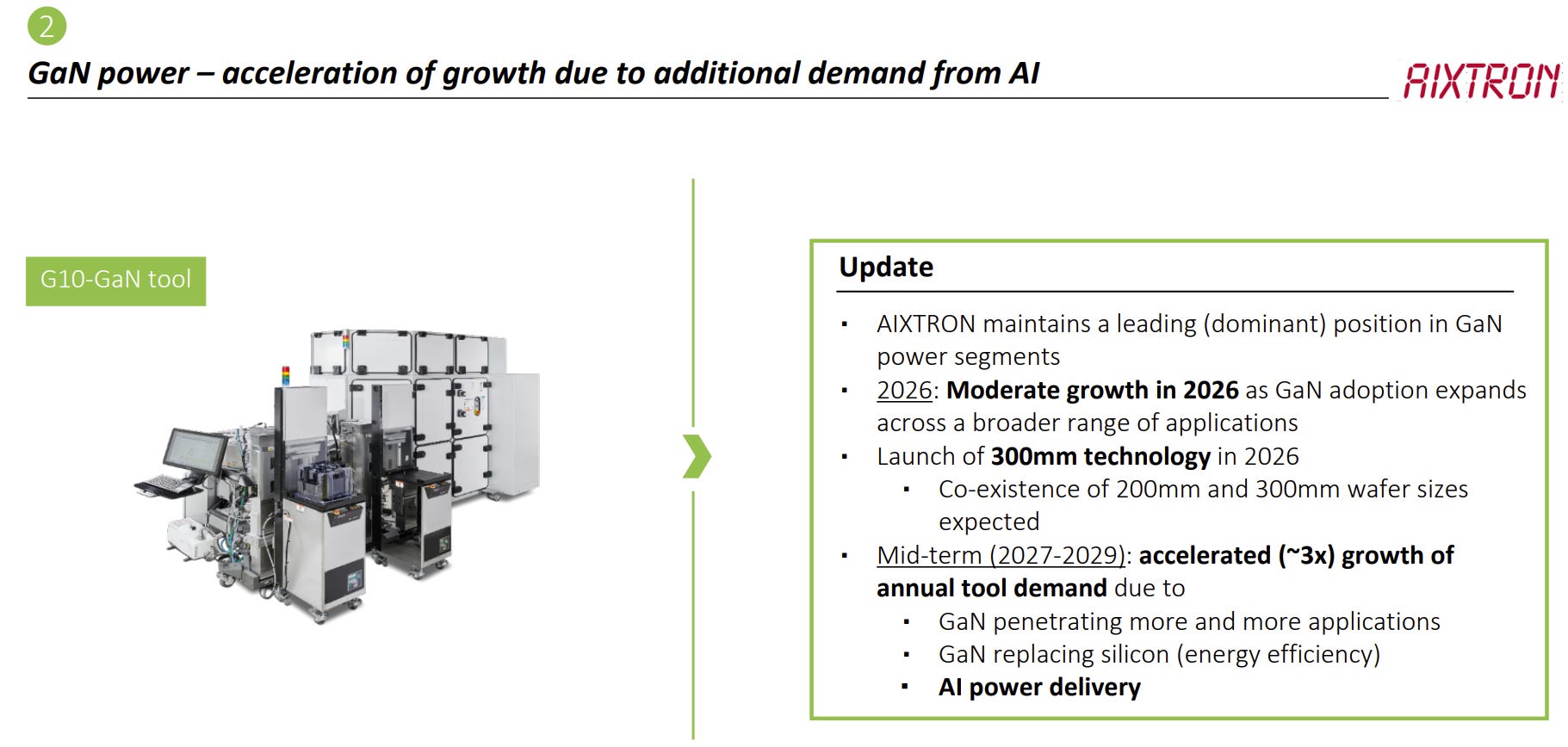

GaN

In my preview, I wrote that GaN is a much longer-dated story than opto — the 800VDC opportunity is real but the ordering window is Q3 2026 to Q1 2027, with revenue showing up mainly in 2027. The call confirmed this.

There is no 800VDC GaN in the backlog. Zero. And we don’t really know when it’s coming except for the fact that it is definitely coming. 100% for sure.

The reason for the uncertainty is that Aixtron is effectively blind to the downstream qualification. Their customers, IDMs and foundries, are qualifying GaN devices with their customers: the board makers, the power supply manufacturers, the rack designers. Aixtron sits at the top of the supply chain and gets the order when the entire chain below them has aligned, so they’re kind of blind to what’s going on.

But the TAM is pretty nice. Aixtron thinks the market can triple.

On 300mm GaN, there’s competition to watch. 300mm GaN’s purpose is to re-use regular old silicon fab capacity for GaN. Since standard silicon fabs process using single-wafer, Aixtron can’t use their planetary reactor design and must compete on single-wafer directly. That’s what Hyperion was for.

The call came a day after Veeco claimed several 300mm GaN orders. Grawert responded that Aixtron is “very well on track” with “multiple orders” of its own. The tool of record decision is expected Q3 or Q4 of 2026. Aixtron is in a great position but this is a risk we can’t ignore because it falls outside of Aixtron’s core moat.